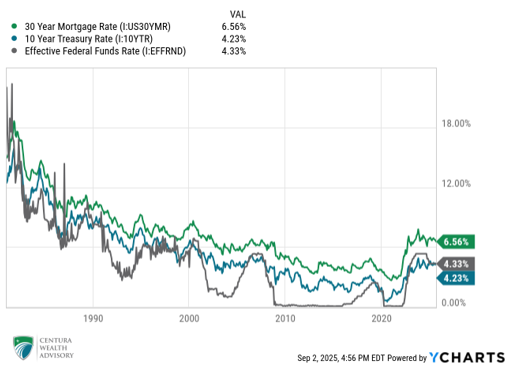

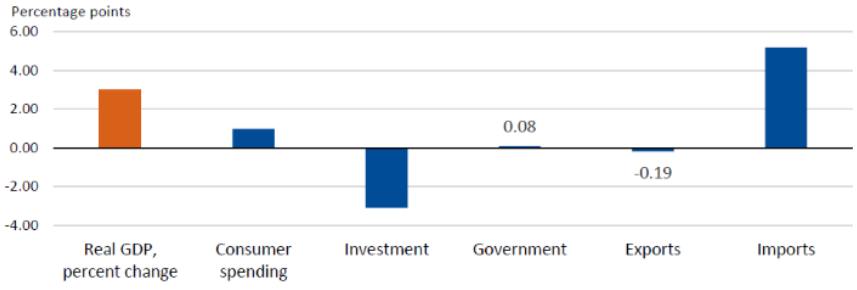

Macro Indicators: Inflation remains a key macroeconomic risk, with March headline CPI and PCE showing prices rising 3.3% and 3.5% on a YoY basis, respectively, due to increased energy prices related to the Iran conflict. The advance estimate for 1Q 2026 GDP printed at 2.0%, driven by AI investment spending, after 4Q 2025’s near-flat growth. The labor market continues to plod along, with unemployment claims continuing to tick down and the unemployment rate at 4.3% as of March.

Trump 2.0: Tariffs remain on the docket, contingent on Congressional approval in mid-July. Geopolitical tensions remain heightened in the Middle East despite the April 8 ceasefire. The fiscal year 2027 federal budget was released in April, proposing a 42% increase in defense and a subsequent 10% decrease in non-defense spending.

Fed & Monetary Policy: At the April FOMC meeting, the Fed held interest rates steady with notable dissents, signaling an uncertain path forward for monetary policy. During his last FOMC press conference as Chair, Jerome Powell broke from tradition to announce he will stay on the Board after his Chair term ends, citing concerns over Fed independence. Kevin Warsh is expected to replace Powell in mid-May, barring confirmation from the Senate.

Capital Markets: Risk assets came back into favor over the month, with U.S. equities rallying to all-time highs, fueled by the tech sector and a strong 1Q earnings season. The dollar reverted to its pre-Iran conflict trend of weakening, helping push international equity markets higher. Credit spreads remain tight and U.S. Treasury yields drifted toward 4.4% on oil-driven inflation concerns. Brent crude oil prices ended the month around $114/bbl.

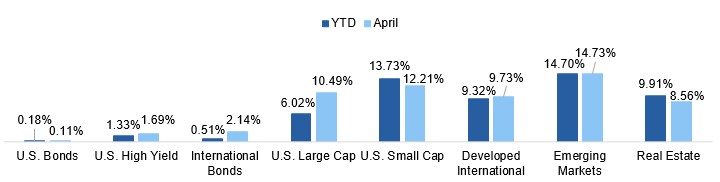

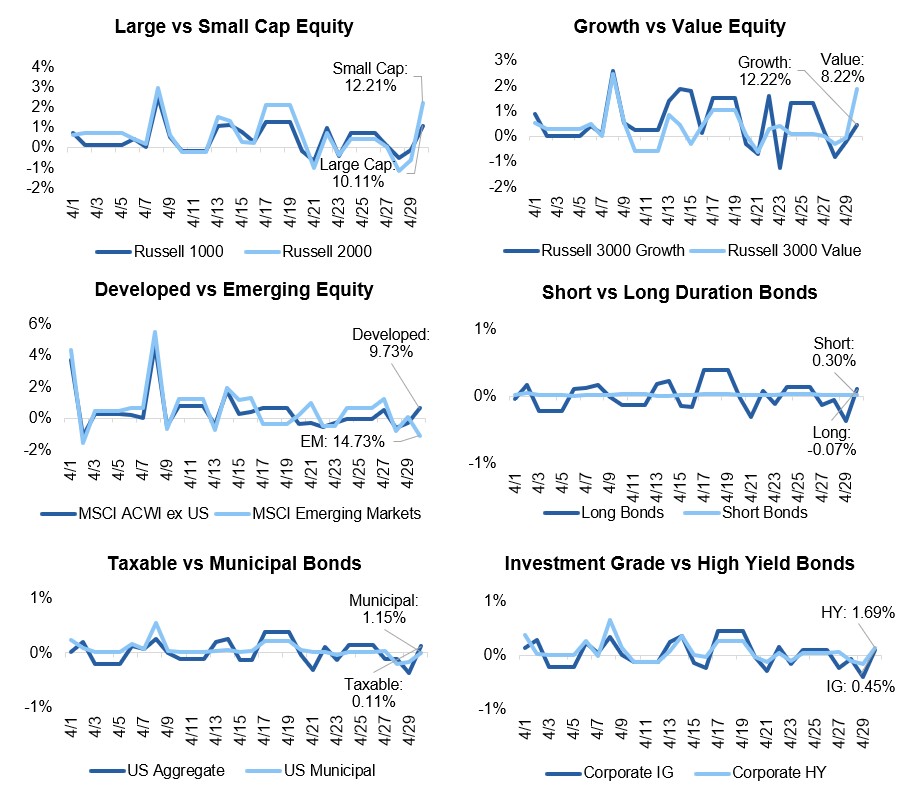

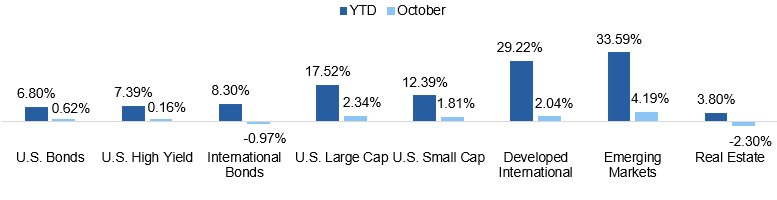

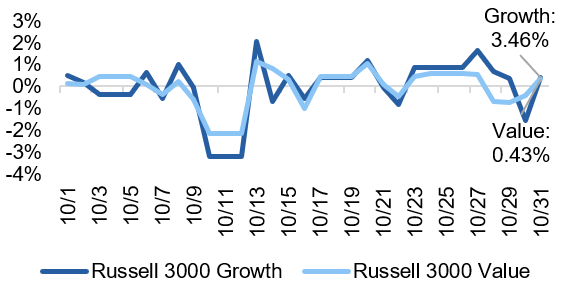

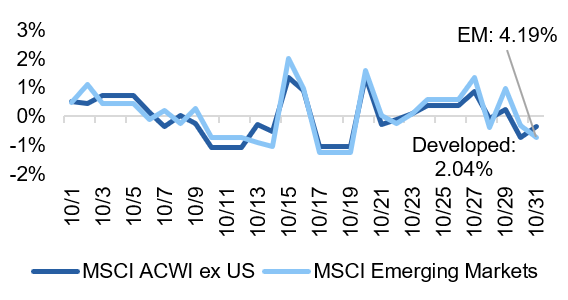

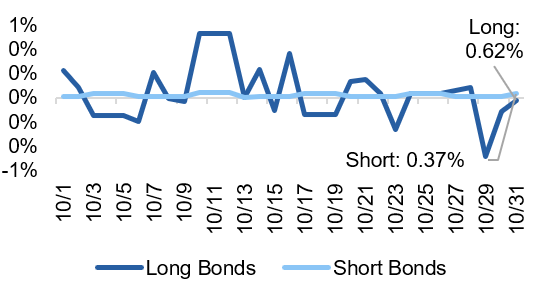

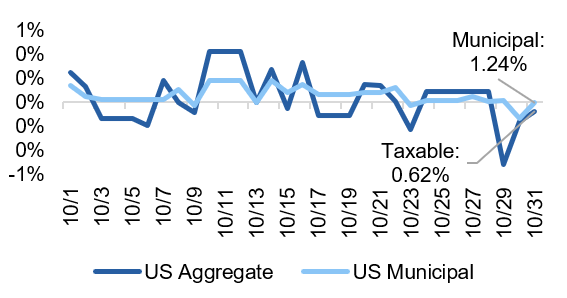

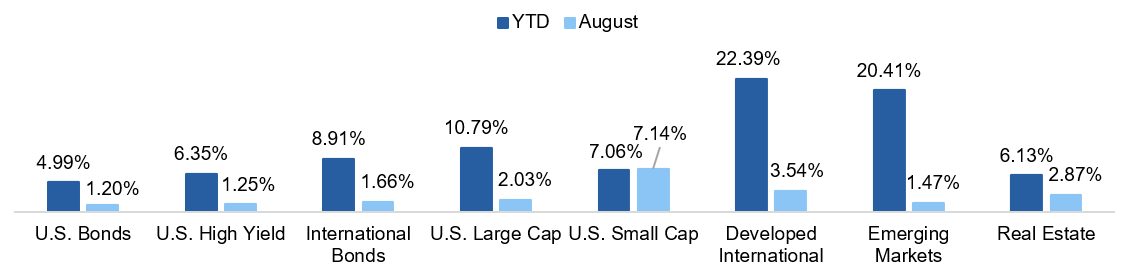

Asset Class Performance

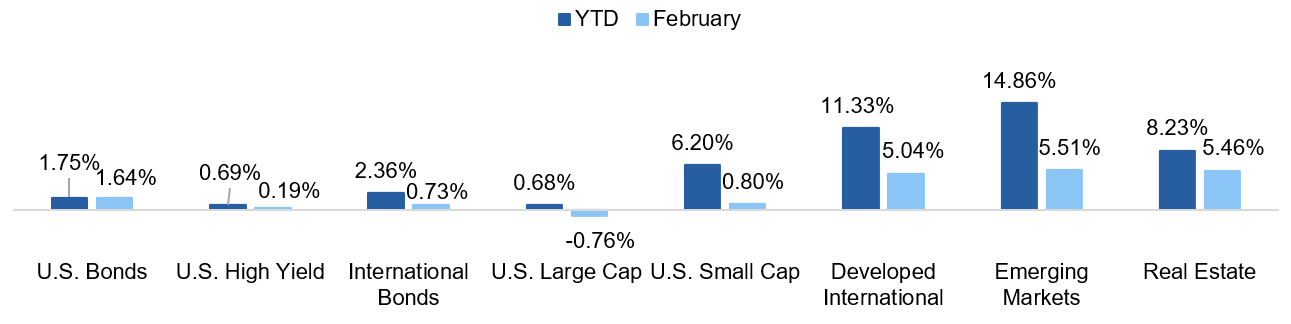

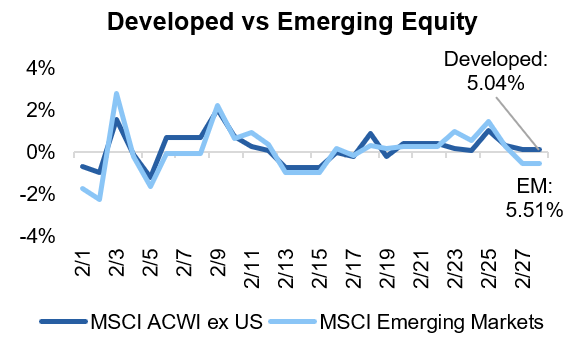

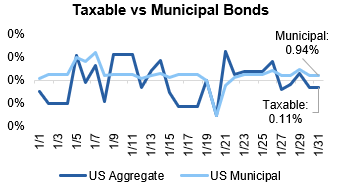

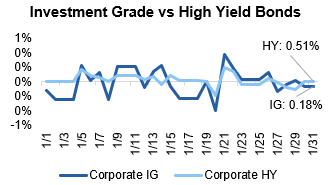

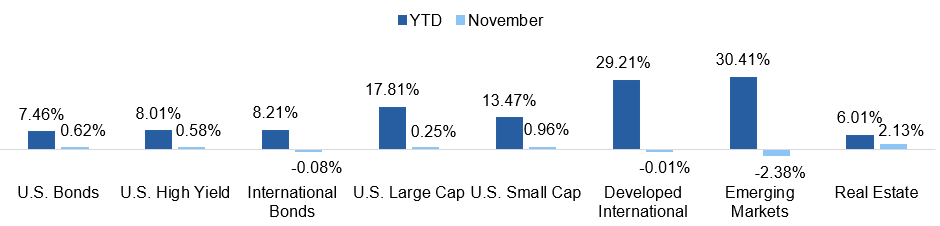

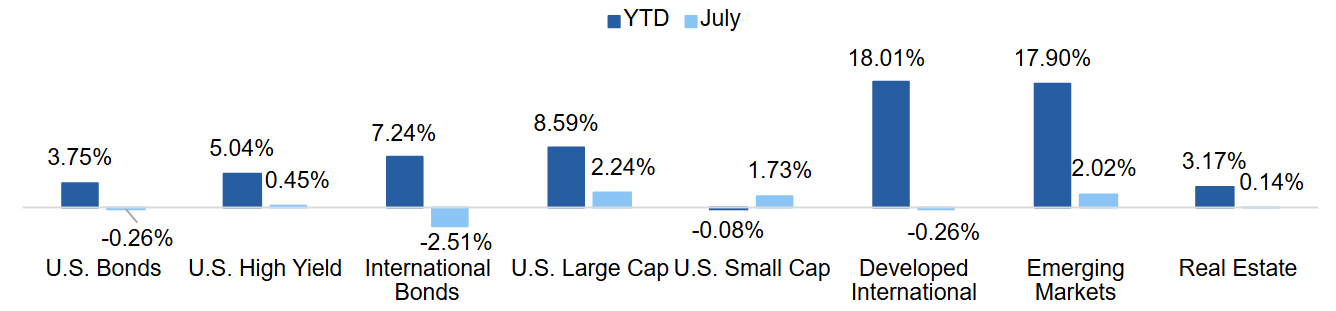

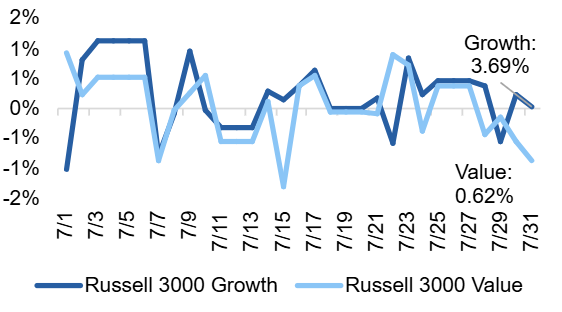

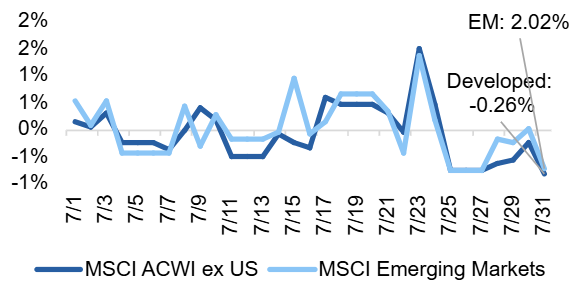

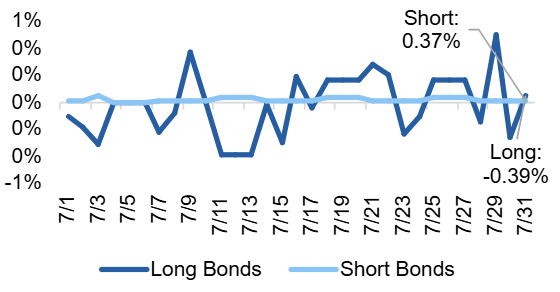

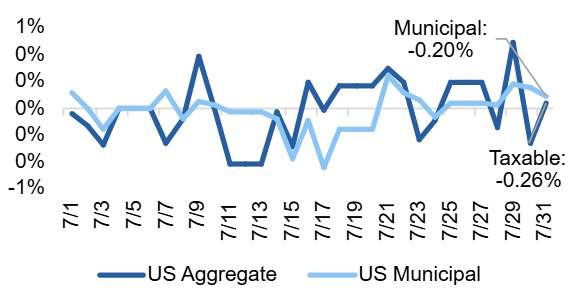

Markets turned positive in April as geopolitical concerns abated. After underperforming in prior months, U.S. equity markets ran at pace with international equity markets in April but continue to underperform on a YTD basis. High yield fixed income markets showed positive performance as spreads tightened over the month.

Source: Source: YCharts. Asset class performance is presented using total returns for an index proxy that best represents the respective broad asset class. U.S. Bonds (Bloomberg U.S. Aggregate Bond TR), U.S. High Yield (Bloomberg U.S. Corporate High Yield TR), International Bonds (Bloomberg Global Aggregate ex-USD TR), U.S. Large Cap (S&P 500 TR), U.S. Small Cap (Russell 2000 TR), Developed International (MSCI ACWI ex US TR), Emerging Markets (MSCI EM TR), and Real Estate (Dow Jones U.S. Real Estate TR).

Markets & Macroeconomics

New Highs in Stocks and at the Pump

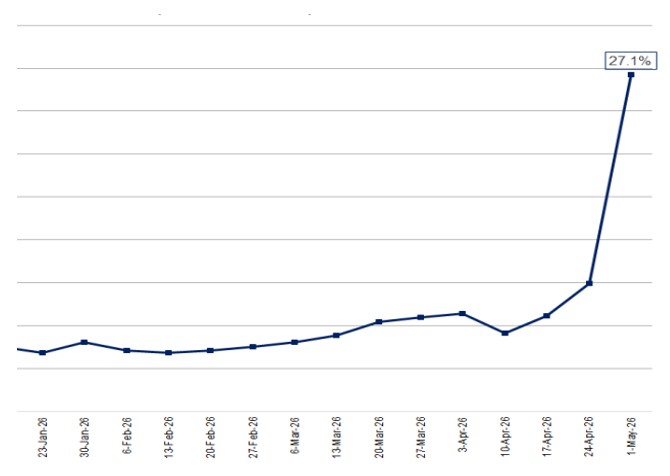

In April, global energy markets confronted one of the worst supply shocks on record. The conflict in the Middle East, which is now entering its third month, kept the Strait of Hormuz almost entirely closed, with the U.S. now blocking traffic in an effort to starve off Iran from continued toll-taking and further exports. The chokepoint handles roughly 20% of the world’s oil and LNG trades where approximately 20 million barrels typically transit the waterway daily. The issue is not isolated to Iran, as the conflict with Iran as well as spillover into neighboring countries forced Gulf producers to reduce total output by more than 14 millions barrels per day – totaling an approximately 440 million barrel expected supply loss thus far.

While Brent crude futures peaked at around $120 near the end of April, those derivative contracts did not tell the whole story of the supply squeeze taking place. In the spot market (for those taking physical delivery of oil), actual transaction prices came in around $25 per barrel higher, illustrated in Exhibit 1. The market is pointing to genuine stress in the physical oil market – for context, during the Russian invasion of Ukraine in February 2022, this premium never peaked above $10. And even though the U.S. is now a net energy exporter, they are not fully insulated from the effects of higher energy costs globally.

Gas prices at the pump rose above $4.10 by month-end from $2.80 at the start of the year. The longer oil is not flowing through the Strait, the tighter the pressure on domestic consumption and the greater risk that input costs flow through to corporate margins.

Despite continued conflict and repeated failed attempts at peace talks, markets have looked through the noise and pushed to new highs on the back of a strong start to the 1Q earnings season. While markets are looking through the conflict, one question remains: whether or not the Federal Reserve will as well. The April FOMC meeting saw three governors oppose the inclusion of easing language in the statement. Expectations for PCE inflation have risen; however, importantly, expectations of long-run inflation remain anchored. While the consumer and broader economy have remained resilient, the risk of higher energy costs feeding through to core inflation creates a much more complex task for the expected incoming Fed Chair Kevin Warsh. As of month-end, Warsh has been approved by the Senate Banking Committee and should face a full Senate confirmation vote in May. Markets have historically tested a new Fed Chair, and the current environment appears ripe for history to rhyme once more.

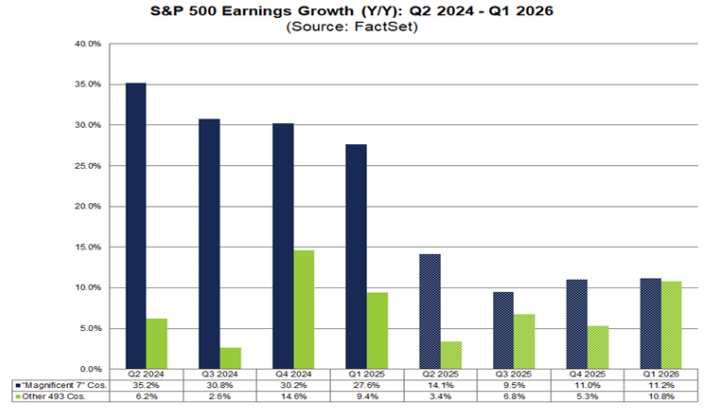

Exhibit 2: 1Q’26 S&P 500 Earnings Growth (YoY)

Source: Source: FactSet, Earnings Insights

The Bottom Line:April delivered a study in contradictions: equity markets climbed to new highs on the back of surging earnings growth, even as the worst oil supply shock since the Russian invasion of Ukraine sent gas prices soaring, reigniting inflation fears. The incoming Fed Chair is set to inherit a divided institution, an unresolved energy crisis, and a market with very little room for disappointment.

Looking Ahead

Navigating the Macroeconomic Fog

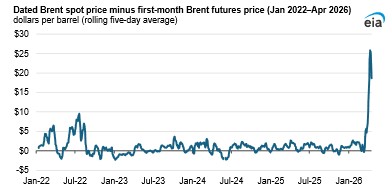

The two forces dominating the outlook heading into May are the same ones that defined April: an oil-driven inflation shock with no clear end date and a Federal Reserve entering a leadership transition at precisely the wrong moment. Together, these forces are creating a policy environment with fewer positive outcomes than markets may be currently pricing in. The Iran conflict that began February 28 has proven more durable than early consensus expected – going on 60+ days – with the Strait of Hormuz still effectively closed and oil prices around $114 to end the month, despite a ceasefire, illustrated in Exhibit 3. This means that the energy shock is no longer a tail risk, but rather a base case. For the U.S. economy, every $10 rise in Brent adds roughly 0.2 to 0.5 percentage points to inflation and shaves 0.1 points off output growth. This stagflationary math is already showing up in the data: core PCE accelerated to 3.2% in March, headline PCE touched 3.5%, and 1Q GDP growth came in at a modest 2.0%, below the 2.2% consensus. Beneath the headline data, the labor market continues to show sluggish growth and the IMF revised 2026 global inflation up to 4.4%. The Fed now faces a classic (and dreaded) dual mandate dilemma: fighting inflation could tip a slowing economy into contraction, but staying on hold could cause inflation expectations to become unanchored from the 2% target.

Exhibit 3:Brent Crude Oil YTD Spot Price ($/bbl)

Source: EIA

Adding to the current environment’s complexity is the Fed’s leadership backdrop. Incoming Chair nominee Kevin Warsh cleared the Senate Banking Committee 13-11 on April 29 and now awaits a full Senate vote. The simultaneous April 29 FOMC decision to hold rates at 3.50-3.75% drew four dissents, the most divided vote since October 1992. As of month-end, markets are pricing a roughly 25% probability of one 25-bps hike over the next 12 months. Investors should expect elevated uncertainty around the Fed’s reaction function and a wider rate-path distribution in the forward-looking environment, particularly as concerns related to Fed independence remain heightened.

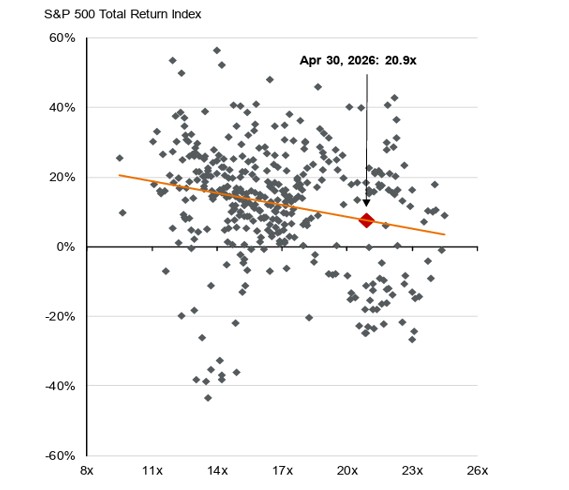

From a positioning standpoint, staying anchored to fundamentals remains crucial rather than trying to call the market top or dramatically reposition portfolios. Equities have recovered impressively from March lows, with the S&P 500 closing the month of April at a fresh all-time high of 7,193. However, this trend reversal means that valuations are once again stretched to historic levels. Historically, higher equity valuations tend to result in lower forward-looking returns, illustrated in Exhibit 4. While earnings growth projections look strong, the full pass-through of higher oil prices to corporate margins has likely not yet occurred. The fixed income market has seen yield curves steepen globally, with better risk-adjusted value in the belly of the U.S. curve and high-quality municipals than long duration sovereigns. Outside of these trends, quality, diversification, and duration discipline continue to be the right tools for the foggy environment ahead.

Exhibit 4: : S&P 500 Forward P/E & 1-Year Returns

Source: JPM Guide to the Markets

The Bottom Line:The Iran conflict and Fed leadership transition have created a policy environment with few obvious answers for how to allocate portfolios. While a recession or a market breakdown is not largely expected, we are watching the duration of the oil shock and global interest rate divergence closely. The next two to three quarters will require patience and discipline as these forces work through the economy, allowing the macro fog to (hopefully) lift.

Capital Markets Themes

What Worked, What Didn’t

•U.S. Equity Markets Soar Back: U.S. equity markets posted a positive month, with large cap equities soaring to all-time highs and the more attractively valued small cap sector posting over 12% total returns, driven by both sentiment and a strong earnings season.

•Spreads Tighten: Credit spreads tightened over the month, prompting close to 2% returns in high yield bonds, another illustration of the return of the “risk on” attitude across markets.

•International Outperformance Continues: International equities returned to their pre-conflict trend of outperformance, strengthened by a weakening dollar and a ceasefire in the Middle East that helped partially reopen the Strait of Hormuz, easing oil prices.

Source: YCharts. Data call-out figures represent total monthly returns.

On Alternatives

Following the Capital, Missing the Returns

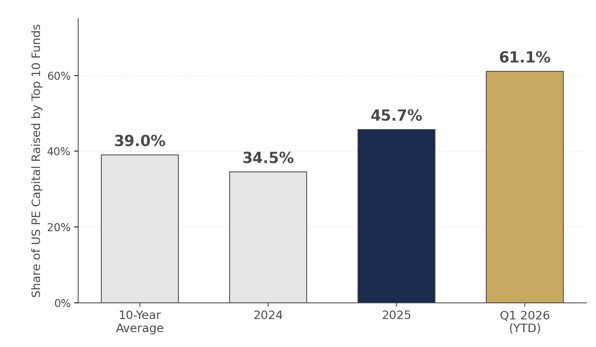

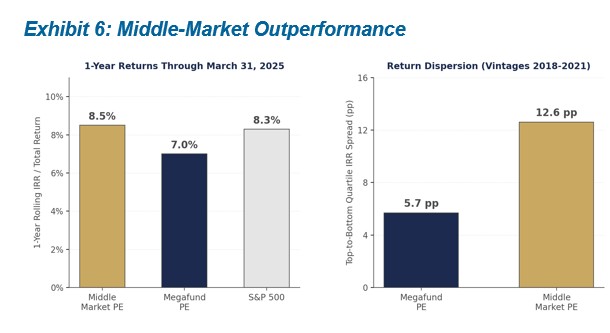

The 10 largest U.S. Private Equity (PE) funds raised in 2025 captured almost half (45.7%) of all PE capital, well above the 10-year average of 39%. Through mid-April 2026, the top 10 funds have captured 61.1% of capital ($60.2B of $98.5B), illustrated in Exhibit 5, though that share will likely moderate as more funds close throughout the year. With this much capital flowing into so-called megafunds, one would assume they would outperform the rest of the PE market, but the data tells a different story. One-year rolling IRR through March 31, 2025 was 8.5% for middle-market managers, narrowly outpacing the S&P 500 at 8.3%, while megafund managers came in at just 7.0%. PitchBook’s research shows the same at the manager level: emerging managers have outperformed established managers across the most recent vintages. Middle-market funds have demonstrated a consistent ability to outperform their larger counterparts over time, yet LP inflows continue to favor scale over performance.

Exhibit 5: Megafund Concentration Surge

Source: PitchBook

Exhibit 6: Middle-Market Outperformance

Source: PitchBook

Why have LP inflows favored megafunds? The answer lies in dispersion of returns. The performance gap between top- and bottom-quartile middle-market managers has run about 12.6% in recent vintages, more than double the 5.7-point spread seen among megafunds, illustrated in Exhibit 6. Middle-market managers offer more upside but realizing that upside requires better manager selection. For most LPs, consolidating with larger, established managers is the more practical path, even if it means giving up some of that upside.

Why are middle-market managers outperforming the megafunds and their nearly unlimited resources? The large-cap space is simply more efficient, leaving less room to drive alpha. In the lower- and middle-market, managers can access niches and deals that megafunds cannot reach due to their size, and their specialized teams can exploit those inefficient pockets. The large buyout space, by contrast, has come to resemble public equity exposure, just with added fees and illiquidity. With so much capital chasing a limited set of large deals, megafunds end up bidding against each other for the same assets, ultimately compressing investor returns.

The Bottom Line: The data shows that the more inefficient corners of the PE market add more value to investor portfolios, but this warrants an emphasis on rigorous manager selection on GPs with a proven ability to drive alpha. While mega PE funds have attracted more capital recently, we prefer to reserve our large-cap equity exposure for the public market, where we receive daily liquidity for a similar return profile.

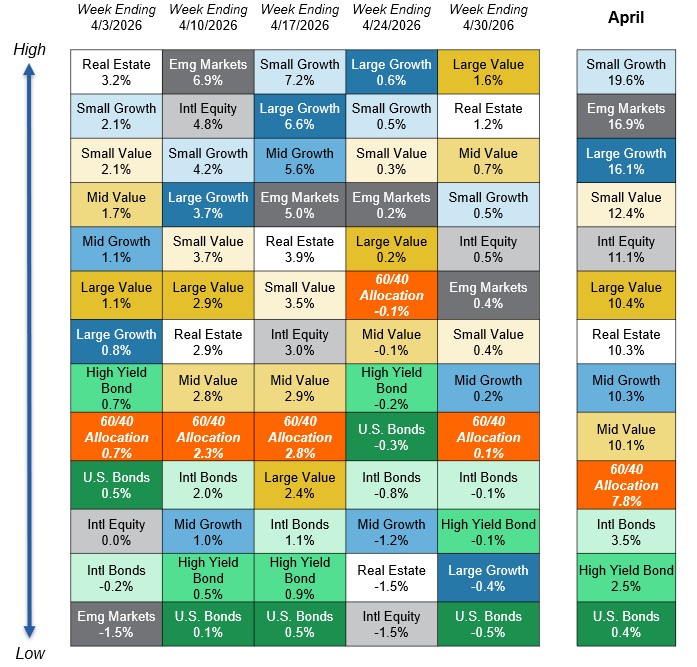

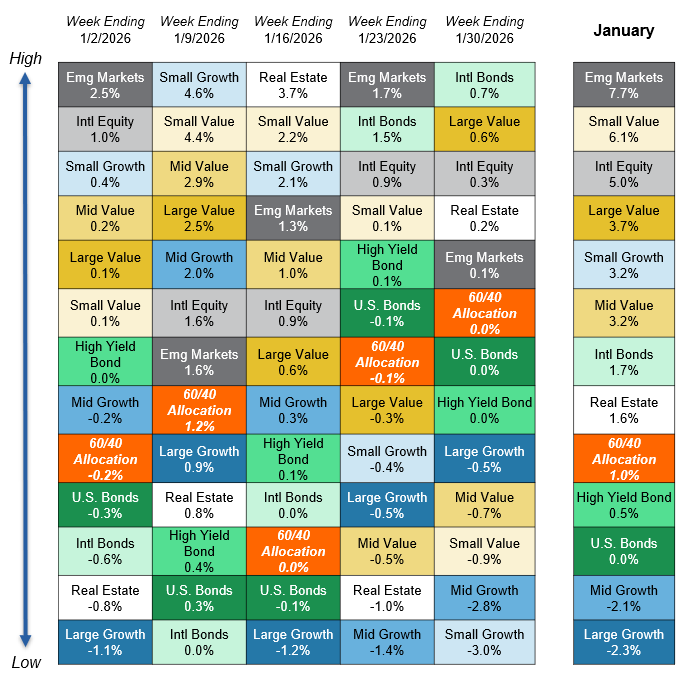

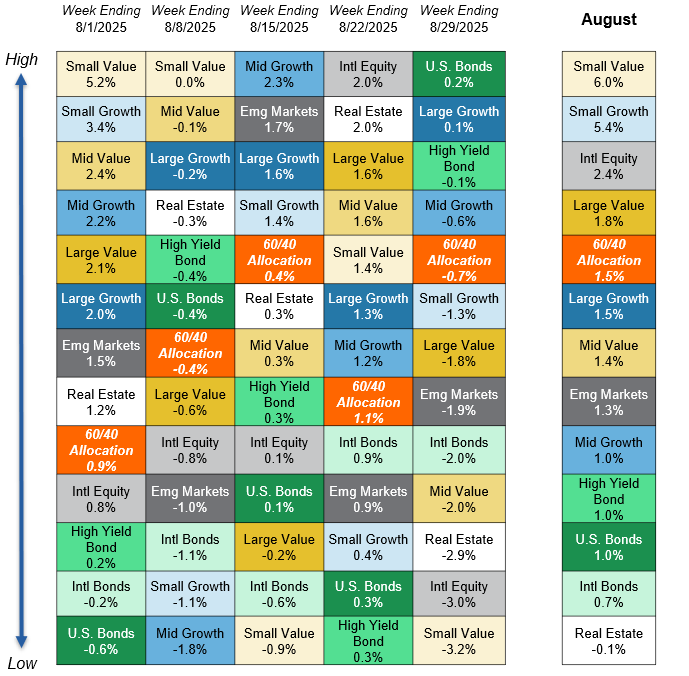

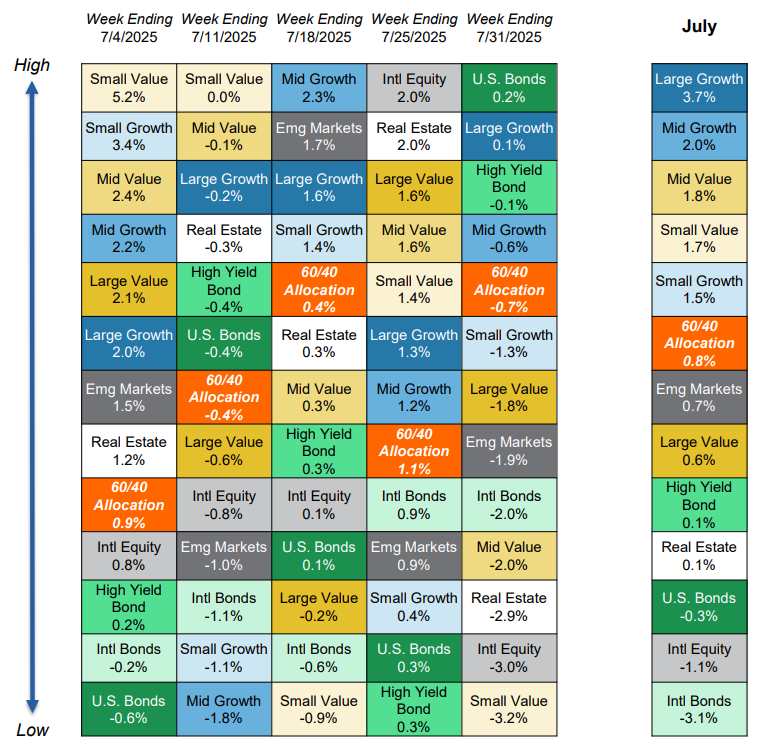

Asset Class Performance Quilt

Markets are ever-changing, making diversification across asset classes and sectors a critical component to portfolio construction. As illustrated below, a Balanced 60/40 portfolio provides greater consistency of returns and less volatility over time.

Source: YCharts. Asset class performance is presented using market returns from an exchange-traded fund (ETF) proxy that best represents its respective broad asset class. Returns shown are net of fund fees for and do not necessarily represent performance of specific mutual funds and/or exchange-traded funds recommended by Centura Wealth Advisory. The performance of those funds may be substantially different than the performance of broad asset classes and to proxy ETFs represented here. U.S. Bonds (iShares Core U.S. Aggregate Bond ETF); High Yield Bonds (iShares iBoxx $ High Yield Corp Bond ETF); Intl Bonds (Invesco International Corporate Bond ETF); Large Growth (iShares Russell 1000 Growth ETF); Large Value (iShares Russell 1000 Value ETF); Mid Growth (iShares Russell Mid-Cap Growth ETF); Mid Value (iShares Russell Mid-Cap Value ETF); Small Growth (iShares Russell 2000 Growth ETF); Small Value (iShares Russell 2000 Value ETF); Intl Equity (iShares MSCI ACWI ex US ETF); Emg Markets (iShares MSCI Emerging Markets ETF); and Real Estate (iShares US Real Estate ETF). The return displayed as “60/40 Allocation” is a weighted average of the ETF proxies shown as represented by: 40% U.S. Bonds, 12% International Stock, and 48% Large Blend.

https://centurawealth.com/wp-content/uploads/2024/11/iStock-1816227914.jpg12242448Cailyn Changhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngCailyn Chang2026-05-05 10:10:292026-05-05 13:31:34Market Month in Review – April 2026

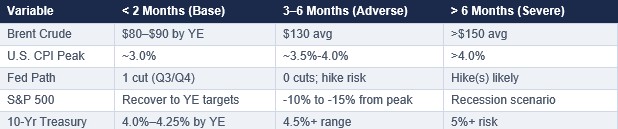

On February 28, 2026, coordinated U.S. and Israel military strikes on Iran escalated into the effective closure of the Strait of Hormuz – the first time in history this chokepoint has been blocked. Approximately 20% of global oil and LNG supply transits this corridor and its closure caused Brent crude to surge from roughly $80 per barrel to nearly $119 within weeks. This single event has reshaped the investment outlook across every asset class covered in this report and represents the most significant geopolitical supply shock since at least the 1970s, according to the International Energy Agency. The outlook for the conflict remains highly uncertain and how it plays out will define how assets perform for the remainder of the year.

Scenario Framework: Iran Conflict Duration Is the Key Variable

Source: Capital Economics, Goldman Sachs, EY-Parthenon, Charles Schwab, Federal Reserve March 2026 projections, Al Jazeera/Chatham House economic analysis. Oxford Economics Alpine Macro baseline does not expect conflict to extend beyond two months.

Key Cross-Asset Themes in Q1

U.S. Macro: The Iran conflict introduced a stagflationary risk premium not seen since the 1970s oil shocks. Energy-driven inflation is tracking toward 3.5% to 4.0%, while the labor market continues to soften, with volatile monthly reports. GDP growth for 2026 was revised to approximately 2.0%, contingent on a conflict resolution within 2-3 months. Compounding the macro uncertainty, the incoming Fed Chair, Kevin Warsh, has yet to be nominated, creating implications for monetary policy moving forward.

U.S. Fixed Income: The standard safe-haven bid for Treasuries failed as yields rose, not fell, with inflation expectations dominating sentiment. The 10-year Treasury climbed from 3.97% pre-conflict to 4.30% as of quarter-end. At their March 18 FOMC meeting, the Fed held rates unchanged for the second consecutive meeting, with only one cut now projected for 2026. Rate hike risk is non-trivial: the Atlanta Fed shows a ~20% probability of a 25 bps increase. Moving forward, TIPS and short-duration agency MBS are preferred over assets like long-duration Treasuries. The attitude of the Fed will be critical for risk assets. Do they “look through” the price spike associated with the change in oil prices or react?

U.S. Equities: The S&P 500 ended the quarter down approximately 6.5% from its January peak (with daily swings of up to 2%). Over the quarter, defense, energy, and AI adoption beneficiaries outperformed; consumer discretionary, companies displaced by AI (namely, software), and airlines underperformed. History suggests geopolitical-driven drawdowns recover within 12 months if the conflict is contained, but the 2026 EPS estimate of $305–$313 per share remains under revision as the Iran conflict continues.

International Equity: Asia – particularly India, South Korea, and Southeast Asia – is most vulnerable to the energy shock whereas Europe faces moderate spillover. Despite the headwind of the Iran conflict, the structural case for international equities remains intact: valuations remain cheaper than U.S. equivalents, and dollar weakness is likely to resume post-conflict. As the Iran conflict continues, Latin American energy exporters (Brazil, Colombia) and Gulf sovereign equities should benefit.

Private Equity: Near-term dealmaking has stalled as GPs await resolution of the Iran conflict. Defense contractors, domestic energy infrastructure, and AI-integrated portfolio companies are the clear near-term beneficiaries. The structural M&A recovery thesis remains intact: a H2 2026 reacceleration is expected once macro uncertainty clears. Secondaries and continuation vehicles remain the primary liquidity mechanism for legacy 2021–2022 vintage holdings.

Private Debt: A coordinated wave of retail redemptions swept major BDC and interval fund vehicles in Q1, notably forcing gating events at Blackstone (BCRED: $3.8B requested, 7.9% of AUM – injected $400M firm capital), BlackRock (HPS HLEND: $1.2B requested, 9.3% of NAV; $620M approved), Blue Owl (OBDC II permanently frozen), and Cliffwater ($33B fund: 14% of shares requested vs. a 7% cap), in addition to Morgan Stanley, Ares, and Apollo. Two structural risk drivers are converging: AI-driven disruption of SaaS borrowers (~19% of direct loans) eroding creditworthiness and a structural liquidity mismatch in semi-liquid vehicles. Payment in kind (PIK) loan usage and covenant-lite structures are the leading indicators of deeper credit stress. Morgan Stanley projects default rates could reach 8%; UBS warns of up to 13% in a severe scenario.

Real Estate: Rising Treasury yields have deferred cap rate compression and the core real estate recovery with the outlook for the U.S. multifamily sector uncertain as the Iran conflict has disrupted expectations for interest rate cuts in 2026. Data centers and industrial logistics remain secular overweights; office is structurally impaired. The $936B CRE debt maturity wall is generating a growing pipeline of distressed refinancing opportunities for well-capitalized opportunistic investors.

Bottom Line: The conflict in Iran has come at a time when U.S. equity valuations and credit spreads are at all-time highs and tights, respectively, and when the U.S. economy is suffering from stubborn inflation and a weakening labor market. Moving forward, we expect continued volatility and potential downside risks. The outlook for the medium-term (3+ years) remains intact, but the longer oil prices stay elevated, the more that thesis will be challenged.

U.S. Macroeconomic Landscape

Q1 2026 Market Review

The U.S. macroeconomic picture in Q1 2026 was defined by a fragile but resilient economy suddenly confronting a major exogenous shock. The quarter began with GDP momentum on solid ground – Q3 2025 had printed an exceptional 4.3% annualized growth rate – but Q4 2025 slowed sharply to below 1%, reflecting the combined drag from a 43-day government shutdown in October and November, softening consumer spending, and a decelerating labor market. January data confirmed these trends: core PCE inflation rose to 3.1%, above the Fed’s 2% target, while consumer confidence approached recessionary levels. February brought further deterioration: the economy shed an unexpected 92,000 nonfarm payroll jobs, pushing the unemployment rate to 4.4%. This “low-hire, low-fire” equilibrium – where the labor market is too weak to generate jobs but too stable to trigger Fed easing – placed the FOMC in an uncomfortable holding pattern. Then, on February 28, the U.S.-Israel strike on Iran transformed the macro outlook. Brent crude surged above $100 per barrel within days and ended the quarter at around $119/bbl. National average gasoline prices climbed from $2.98/gallon pre-conflict to $4.02/gallon by March 31 – crossing $4.00 for the first time since August 2022 – directly and immediately pressuring consumer purchasing power. The Fed held rates unchanged for the second consecutive meeting on March 18, with Chair Powell acknowledging the “uncertainty” while projecting year-end core PCE at 2.7%.

2026 Forward Outlook

The U.S. macroeconomic outlook for the remainder of 2026 now hinges critically on the duration and intensity of the Iran conflict. The pre-war base case – GDP growth of 2.0%–2.6%, gradual Fed easing to 3.0%–3.25%, and core PCE declining toward 2% by year-end – has been materially revised across most institutional forecasters.

The inflation path has worsened significantly. Before the Iran strikes, core PCE was running at 3.1% and headline CPI was at 2.4%. Higher energy costs now threaten to push headline inflation to 3.5%–4.0% in the near term, with potential second-round effects on food, transportation, and utilities. CNBC quotes economists warning of “a familiar but uncomfortable dilemma,” alluding to an energy shock generating inflation alongside a slowing labor market. J.P. Morgan notes that “there’s never a good time for an adverse supply shock, but ideally the starting point would be low and stable inflation,” a precondition that clearly did not exist entering the conflict. The CBO had already projected PCE inflation at 2.7% for 2026 before the conflict, above the Fed’s pre-conflict estimates.

The stagflation risk – rising inflation alongside slowing growth – is the dominant macro concern. Federal Reserve officials, including Powell, have pushed back against the “stagflation” label, arguing that the 1970s comparison requires double-digit unemployment and inflation that does not apply today. However, the structural parallels are uncomfortable: an oil shock in an environment of above-target inflation, weakening employment, and politically constrained monetary policy. The Atlanta Fed’s probability tracker shows a nearly 20% probability of a rate hike this year – a scenario that would have been broadly inconceivable three months ago.

The One Big Beautiful Bill Act’s (OBBBA) fiscal stimulus, including an estimated $150 billion in consumer tax refunds flowing in Q1–Q2 2026 and full equipment expensing benefits, provides a partial offset, supporting consumer spending and business investment in the near term. However, the CBO’s warning of $3.4 trillion in added deficits over 10 years remains a structural constraint, and rising defense spending from the Iran conflict will widen this deficit further, potentially exerting upward pressure on long-term Treasury yields.

Lastly, the May 15 Fed Chair transition remains a significant institutional wildcard, particularly as Kevin Warsh’s nomination remains stalled in the Senate. If Powell departs without a confirmed successor, markets face an extended period of leadership uncertainty at the FOMC during one of the most complex monetary policy environments in decades. Powell has stated he has “no intention” of leaving voluntarily until a related investigation is resolved and his successor is confirmed.

Bottom Line: The most likely base case is that the conflict proves shorter than feared, oil retreats toward $80–$90 per barrel by H2 2026, the Fed delivers one 25-basis-point cut in Q3, and GDP growth lands near 2.0% for the full year. But the tail risks, particularly a prolonged Strait of Hormuz closure, are more severe today than at any point since 2020 and the 2008 financial crisis.

U.S. Equity Markets

Q1 2026 Market Review

U.S. equity markets entered Q1 2026 with considerable momentum following the S&P 500’s strong 2025 close, where the index gained 17.9% for the year and posted its third consecutive year of double-digit returns. Q4 2025 closed with notable leadership rotation: value outperformed growth; cyclical sectors, including financials, industrials, and healthcare led; and Magnificent 7 correlations fractured for the first time in the cycle. Small caps, as measured by the Russell 2000, were up 2.2% in Q4, finally beginning to perk up on improving macro expectations. January 2026 extended this momentum, supported by strong Q4 earnings releases and fiscal stimulus optimism from the OBBBA. However, the quarter was violently interrupted on February 28, when joint U.S.-Israeli military strikes on Iran triggered retaliatory attacks across the Gulf and the closure of the Strait of Hormuz. The S&P 500 finished the quarter down 4.6%, led by the energy sector while consumer discretionary and technology faced pressure from rising oil prices compressing consumer purchasing power. Equity markets swung sharply in March as conflict headlines drove outsized daily moves – falling as much as 1.7% on March 26 before surging 2.9% on March 31 to close out the quarter. Healthcare and defense-related names outperformed as AI capex narratives gave way to geopolitical risk-premium repricing. The more economically sensitive small- and mid-cap market reversed its outperformance and underperformed their large cap peers.

2026 Forward Outlook

The U.S. equity outlook for the remainder of 2026 has bifurcated sharply: the base case before February 28 (continued AI-driven earnings growth, multiple expansion, broadening leadership) must now be weighed against a scenario where elevated oil prices compress consumer spending, reignite inflation, and complicate the Fed’s easing path.

The Iran conflict has introduced a stagflationary risk premium into equity valuations that was absent entering the year. Morgan Stanley notes that markets have historically posted double-digit gains three and six months after the onset of major conflicts, but this historical pattern is conditioned on conflicts being contained and energy disruption temporary.

For corporate earnings, the consensus S&P 500 EPS estimate for 2026 of $305–$313 is actively under review. Energy companies and defense contractors benefit directly from the Iran conflict and increases in defense spending could drive multiyear demand for aerospace, drone, satellite, and missile defense technologies, a structural shift that could outlast the immediate conflict. Conversely, consumer discretionary, airlines, shipping, and energy-intensive industrials face near-term margin pressure.

History counsels patience. In 20 major military conflicts since World War II, the average market recovery following the initial geopolitical shock has been positive within 12 months. Investors who exit during geopolitical downturns typically miss the recovery, supporting the notion that portfolios constructed with appropriate diversification should remain in place. The key tactical pivot is from broad market beta to sector-specific positioning: overweight defense, energy infrastructure, TIPS-linked assets, and AI adoption beneficiaries with pricing power. Investors can also consider going underweight consumer discretionary, airlines, and yield-sensitive sectors where the combination of higher rates and higher energy costs creates a dual squeeze. Mid- and small-cap exposure may face near-term headwinds as higher-for-longer rates bite on financing costs and higher energy prices impact margins.

Bottom Line: The conflict in Iran has come at a challenging time for the U.S. equity sector, with stretched valuations, a stalled rate-cutting cycle, and a weak labor market. We would expect substantial sector rotation as the market tries to find safe havens against the geopolitical turmoil causing the indices to gyrate substantially.

International Equities

Q1 2026 Market Review

International equity markets carried extraordinary momentum into Q1 2026 following the most decisive year of outperformance versus U.S. equities in over a decade. The MSCI EAFE returned 31.9% in 2025 and the MSCI EM returned 34.4% in USD terms – roughly double the S&P 500’s 17.9% – with approximately 10 percentage points of the EAFE return attributable to U.S. dollar weakness. The MSCI EM Index opened 2026 with approximately 7% gains through early February, clearing major resistance at its 2021 highs, with broad participation (over two-thirds of constituents trading above their 200-day moving averages). European equities extended gains through January on German fiscal stimulus optimism. This constructive picture was disrupted materially when U.S. and Israeli forces struck Iran on February 28. Asia appears most vulnerable to the energy supply shock given its dependence on Persian Gulf oil and LNG imports, while Europe faces meaningful exposure through energy price pass-through and slowing growth. The near-term dollar appreciation impulse – historically a headwind for international equity returns for USD-based investors – has arrested the dollar’s decline, at least temporarily, removing one of the key 2025 tailwinds for international equities.

2026 Forward Outlook

The Iran conflict has introduced the most significant near-term headwind to international equity performance since the 2022 Russia-Ukraine crisis, but the structural case for an international allocation remains compelling, and, in some respects, is strengthened by the conflict’s dynamics.

The divergence in vulnerability is stark. Asia, particularly India, South Korea, Japan, and Southeast Asian manufacturing economies, faces the most acute near-term pressure from higher energy import costs. India, with thin foreign exchange reserves and heavy Middle Eastern crude dependence, faces elevated vulnerability to prolonged disruption, with higher energy costs feeding inflation and weakening the rupee. South Korea, home to Samsung and other global technology players, faces energy cost pressure on semiconductor manufacturing. Wheat prices have also risen, with food-importing countries facing acute stress from the conflict’s agricultural disruption.

Europe’s exposure is meaningful but more manageable. Chatham House estimates that if the conflict is contained, European inflation in 2026 would be approximately 0.5 percentage points higher than pre-conflict forecasts. A more severe scenario – oil at $130 per barrel – could push Eurozone inflation to over 4% year-over-year, potentially forcing the ECB to raise rates and causing the Eurozone economy to contract in Q2. Germany’s fiscal stimulus, however, remains a powerful structural support for European equities, and the MSCI EAFE’s high cyclical weighting (60% in Financials, Industrials, Materials, and Consumer Discretionary) provides exposure to sectors that can absorb energy cost increases through pricing power.

Despite near-term headwinds, the structural bull case for international equities remains intact. Valuations are still significantly cheaper than U.S. equivalents even after 2025’s strong run. The dollar’s longer-term downtrend, driven by geopolitical fracturing and a shift away from dollar-denominated assets, may actually be reinforced by the unilateral nature of the U.S. decision to strike Iran. Dollar weakness will likely resume once hostilities subside, providing a renewed tailwind for international equity returns.

Emerging markets require the most careful differentiation. Energy exporters – Gulf states, Brazil, Colombia, Nigeria – benefit directly from higher oil prices. Latin America, particularly Brazil and Mexico, remains a high-conviction overweight on outsized monetary policy stimulus, supply chain reconfiguration, and oil export revenue. China, despite modest 2026 growth headwinds from higher energy costs, is relatively insulated given its massive renewable energy investments, diversified hydrocarbon suppliers, and strategic petroleum reserves. In fact, some Chinese analysts see the war as a net positive for China’s competitive position.

Bottom Line: While in the short-term, overseas markets are vulnerable to the impact of higher energy prices, there will be winners and losers in that space depending on the oil reliance coming from the Strait of Hormuz. On the assumption that the conflict will end, we expect this to accelerate the shift out of U.S. equity markets and U.S. dollars into overseas markets where valuations are more supportive.

U.S. Fixed Income

Q1 2026 Market Review

Q1 2026 opened with fixed income markets navigating a complex cross-current of moderating inflation, a cautious Federal Reserve, and – most disruptively – the outbreak of the U.S.-Israel military conflict with Iran on February 28, 2026. The quarter began with the Bloomberg U.S. Aggregate enjoying tailwinds from the Fed’s Q4 2025 rate cuts (which brought the federal funds rate to 3.50%–3.75%) and investor optimism around a gradual easing cycle. The 10-year Treasury yield briefly traded as low as 3.93% in late February, reflecting a rally driven by soft economic data, weakening consumer confidence, and falling oil prices. That dynamic reversed sharply when U.S. and Israeli forces launched strikes on Iran, closing the Strait of Hormuz. The 10-year Treasury yield climbed from 3.96% to as high as 4.4% in March, defying the typical safe-haven bid for Treasuries. The Fed held rates unchanged at its March 17–18 FOMC meeting, their second consecutive hold, as policymakers weighed oil-driven inflation risks against a softening labor market that shed 92,000 payroll jobs in February.

2026 Forward Outlook

The remainder of 2026 presents one of the most complex fixed income environments in years, with the Iran conflict reshaping nearly every element of the rate, inflation, and credit outlook. The direction of oil prices – and the duration of Strait of Hormuz disruption – is now the single most important variable for fixed income investors, outshining the previous concerns of a weakening labor market and stubborn inflation.

The Iran conflict has materially complicated the Fed’s policy path. Before the February 28 strikes, consensus forecasted two 25-basis-point cuts in 2026. The Atlanta Fed’s Market Probability Tracker has shown a nearly 20% probability of a rate hike, a sharp contrast to the December 2025 “Dot Plot.” Some economists project Brent crude averaging $150 per barrel over the next six months if the conflict lasts three months, which would push headline PCE inflation well above 3% and force the Fed’s hand to hike rates. The OECD recently raised the inflation outlook for the U.S. to 4.2%, illustrating the potential for rising prices as a result of the conflict. The Fed’s updated March projections forecast year-end core PCE at 2.7%, with Chair Powell acknowledging that “nobody knows” the full economic impact and signaling the central bank will act as needed. Powell’s term ends May 15, and Kevin Warsh’s nomination to succeed him remains stalled in the Senate amid a Justice Department probe, adding a layer of institutional uncertainty.

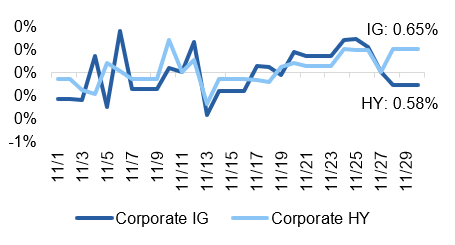

Investment grade credit faces elevated spread risk. Prior to the conflict, IG spreads were near multi-decade tights of 80 basis points with little cushion. AI infrastructure issuance, which dominated 2025 supply, will continue to absorb market capacity, but rising uncertainty and potential economic slowdown from the oil shock may trigger spread widening in lower-rated IG names.

Agency MBS retains its most-favored status within core fixed income. Spread levels relative to IG corporates remain attractive, and the asset class benefits from its relative insulation from energy-driven credit risk. The technical backdrop – supplementary leverage ratio (SLR) regulatory relief and the end of QT – remains intact.

USD EM debt faces headwinds from the Iran conflict. While EM fundamentals remain broadly sound, higher oil import costs are pressuring India, South Korea, and other net importers, illustrating the outsized impact of the oil disruption on Asian economies.

Bottom Line: U.S. fixed income returns will be a function of whether the market sees the inflationary pulse coming from higher oil prices as temporary or more permanent. Against the backdrop of a weakening labor market, the Fed will be forced to pick between looking through the inflationary surge or increasing rates and slowing the economy further. All eyes will be on Warsh and how he is interpreting the data.

Private Equity

Q1 2026 Market Review

Private equity entered Q1 2026 with genuine momentum after a rocky 2025. Total deal value reached $1.2 trillion across 9,000+ transactions in 2025 – only the second time on record above $1 trillion – with exit activity recovering strongly to $682 billion, the best since 2021. The H2 2025 acceleration, driven by macro clarity and Fed rate cuts, carried into January 2026 with sponsor confidence returning, financing costs lower, and bid-ask spreads narrowing on quality assets. The Fed’s three 2025 rate cuts had reduced the average cost of PE middle market term loans by approximately 300 basis points from cycle peaks, directly improving LBO return profiles. However, the Iran conflict outbreak on February 28 introduced a new source of macro uncertainty that has caused GPs to pause M&A processes and limited partners to reassess portfolio exposure. Deal processes underway at quarter-end have been paused or extended as buyers wait for clarity on the conflict’s economic duration. The disruption echoes the Q2 2025 tariff-induced lull, suggesting that H1 2026 deal momentum may disappoint with recovery a function of the outlook on the conflict. Fundraising remains a structural challenge: global PE capital raised fell 11% in 2025 for the second consecutive annual decline, with LPs withholding commitments pending improved distribution metrics.

2026 Forward Outlook

Private equity’s 2026 outlook has been complicated by the Iran conflict but the structural cycle recovery remains intact, with activity expected to rebound once geopolitical uncertainty clears.

The most immediate impact of the Iran conflict on PE is the re-widening of bid-ask spreads and the deferral of exit processes. Rising rate expectations following the Fed’s hawkish hold at the March meeting reduce the DCF-driven uplift to asset valuations that had been building since late 2024. For leveraged buyouts specifically, any reversal of the rate-cut path meaningfully dampens return assumptions, since PE’s carried interest economics are highly sensitive to the entry and exit multiple gap. Morgan Stanley estimates that the cost of PE middle market financing has declined 300 basis points from cycle peaks, but the Iran conflict risks narrowing this advantage if rates stay higher for longer.

The Iran conflict also creates sector-specific opportunities. Defense, aerospace, and energy infrastructure are receiving increased government spending that could drive multiyear demand – exactly the type of predictable, contracted revenue stream that PE platforms prize. Energy infrastructure (pipelines, LNG terminals, grid modernization) and digital infrastructure (data centers, power generation) remain high-conviction deployment themes, and the conflict arguably accelerates both: the Strait of Hormuz closure has renewed calls for energy diversification and domestic production, while defense budgets across NATO are being revised upward.

The secondaries market and continuation vehicles (CVs) remain critical tools for portfolio management in 2026. LPs are increasingly using secondaries for liquidity (due to the explosive growth over “evergreen” funds) and portfolio rebalancing rather than as a last resort, and GPs are using CVs to manage legacy 2021–2022 vintage positions that remain below acquisition cost. Dry powder, while declining from record levels, remains ample to fund large buyouts once clarity surrounding the macro picture returns. The key milestones to monitor are, once again, the duration of the Iran conflict, the Fed’s June meeting for interest rate insights, and Q2 earnings season, which will reveal the extent of energy cost pass-through to PE portfolio company margins.

Bottom Line: PE remains an attractive asset class, however the excess returns generated over public equity may be more muted than in previous decades. Higher borrowing costs, an increase in the number of managers, and more price transparency mean that being selective in choosing your manager is more important than ever.

Private Debt

Q1 2026 Market Review

Private debt markets entered Q1 2026 facing their most significant liquidity test since the asset class became a dominant source of non-bank financing. What began as isolated fraud-driven failures in 2025 with First Brands and Tricolor in the U.S. auto parts sector cascaded into a broad reassessment of BDC and interval fund structures as retail investors sought exits. The wave of gating events in Q1 was unprecedented in scale: Blackstone’s BCRED faced $3.8B in requests (7.9% of its $82.5B AUM) and injected $400M of firm capital to avoid formal gating; BlackRock’s HPS Corporate Lending Fund (HLEND) received $1.2B in withdrawal requests (9.3% of NAV) – its first-ever redemption breach – approving only $620M; Blue Owl permanently froze OBDC II; Cliffwater’s $33B flagship fund received requests for 14% of shares, double its 7% regulatory maximum quarterly cap; and more asset managers followed. Beneath the liquidity headlines, two structural fault lines are widening: first, AI-driven disruption of SaaS and enterprise software borrowers – approximately 19% of total direct loans and 15–17% of BDC portfolios by deal count – is eroding cash flows and threatening the revenue models underpinning loan valuations; second, covenant erosion through covenant-lite structures and escalating PIK usage – approximately 10% of BDC interest income now accrues as PIK rather than cash, a measurable proxy for shadow credit stress. The Iran conflict added a third layer: higher energy costs increase operating expenses for borrowers, higher-for-longer rates intensify refinancing pressure on 2020–2021 vintage floating-rate debt, and resurgent inflation threatens the collateral values underpinning loan marks.

2026 Forward Outlook

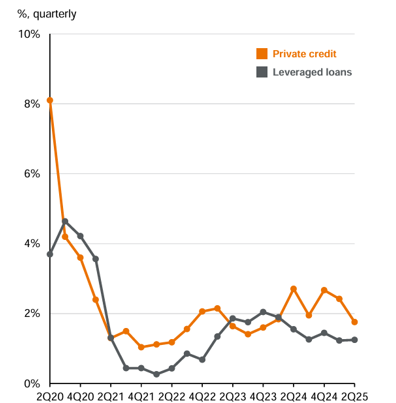

The 2026 outlook for private debt is defined by two compounding risk streams that will fundamentally differentiate returns across managers and vintages. On credit quality: AI disruption is systematically eroding the revenue models of SaaS and enterprise software borrowers – the single largest borrower category in direct lending at approximately 19% of outstanding loans. Software stocks fell ~30% between October 2025 and February 2026 with roughly 15% of SaaS borrowers struggling to cover interest expenses. Morgan Stanley projects direct lending defaults could reach 8%; UBS warns of 13% in a severe AI disruption scenario. However, both agree this would reprice, not break, the asset class given its distributed structure and superior bank capitalization versus 2008.

On structure and liquidity: covenant-lite terms have compressed workout timelines and the first observable signal of borrower distress is now often a missed payment rather than a covenant breach. 23 of 32 rated BDCs face $12.7B in unsecured debt maturities in 2026 – a 73% increase over 2025 – creating a compounding refinancing wall. The opacity of private credit valuations is a structural liability: managers who mark their own assets delay stress recognition, creating conditions for sudden gaps when secondary market transactions or forced sales reveal true pricing. Widening credit spreads and higher bank collateral charges are raising effective back-leverage costs and compressing net returns. The Q1 gating events at Blackstone, BlackRock, Blue Owl, Cliffwater, Ares, and Apollo have exposed a fundamental structural tension: retail capital expecting quarterly redemption access is mismatched with assets requiring months or years to liquidate at fair value. We favor senior secured, hard-covenant structures with documented workout capabilities and limited software sector concentration and intend to avoid covenant-lite legacy vintages from 2020–2022.

Bottom Line: Private debt as an asset class is here to stay however they are not immune to the stresses causing their publicly traded peer’s spreads to widen. We expect a continued tough ride for the near term – not just because of liquidity issues but also because the economic fundamentals are changing.

Real Estate Markets

Q1 2026 Market Review

Real estate markets entered Q1 2026 with cautious optimism – valuations had stabilized after two years of cap rate expansion and transaction volumes were recovering (up 25% year-over-year in Q3 2025). The $936 billion CRE debt maturity wall arrived in earnest in Q1, with a wave of commercial real estate loans requiring refinancing in an environment where interest rates remained elevated and cap rates had not compressed sufficiently to generate equity value. Office properties – impaired structurally by remote work trends – and hospitality assets are facing the softest transaction markets. Industrial and multifamily assets maintained the strongest fundamentals, supported by persistent housing supply constraints and e-commerce demand. The Iran conflict added new complexity: surging energy costs directly affect real estate operating expenses (utilities, HVAC), rising long-term Treasury yields push up commercial mortgage rates, and increased macro uncertainty has deferred transaction decisions from buyers who had been poised to re-enter the market.

2026 Forward Outlook

Real estate’s path for the remainder of 2026 is now shaped by three competing forces: the structural recovery driven by supply discipline and stabilizing valuations; the $936 billion debt maturity wall creating forced transaction activity; and the Iran conflict’s impact on rates, energy costs, and investor risk appetite.

The Iran conflict introduces a specific set of real estate dynamics. Higher energy costs increase operating expenses, particularly for industrial and office properties with high utility consumption. Rising long-term Treasury yields directly increase commercial mortgage rates and cap rate expansion pressure, delaying the cap rate compression necessary for core real estate revaluation.

Data centers represent the most compelling secular growth story in real estate and are directly reinforced by the Iran conflict: the energy security focus accelerates domestic power generation investment, while AI infrastructure demand, which was already driving unprecedented data center development, remains undiminished by geopolitical events. Industrial and logistics real estate maintains strong fundamentals. New construction remains muted across property types, supporting occupancy and rent growth. Supply chain reconfiguration away from the Strait of Hormuz has increased demand for domestic warehousing and logistics infrastructure, a direct near-term tailwind. The outlook for multifamily is likely a mixed bag: housing supply constraints remain acute and affordability pressures prevent many renters from transitioning to homeownership. Office remains a challenged sector of the real estate market as work-from-home structural trends are entrenched. Additionally, the Iran conflict’s uncertainty may further defer corporate real estate decision-making. Hospitality faces a compound headwind: surging jet fuel costs are driving airline ticket prices sharply higher (Gulf carriers are operating under major airspace restrictions), dampening business and leisure travel demand.

The base case for core real estate returns in 2026 is low-single-digit total returns with capital appreciation remaining negative or flat. Value-add and opportunistic strategies targeting distressed debt and repriced assets offer the most compelling risk-adjusted entry in the current cycle.

Bottom Line: Real estate may have a challenging year ahead but given the ebb and flow of supply it is setting the stage for future growth a few years out. In this environment, it makes sense to keep powder dry and consider distressed or opportunistic assets.

DISCLOSURES

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on the market and other conditions. These documents may contain certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Centura Wealth Advisory is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Centura Wealth Advisory and its representatives are properly licensed or exempt from licensure. 12255 El Camino Real, St. 125, San Diego, CA 92130.

https://centurawealth.com/wp-content/uploads/2024/10/iStock-1699822168-scaled-1.jpg11592560Cailyn Changhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngCailyn Chang2026-04-08 10:46:212026-04-08 16:27:35Q1 2026 Market Wrap: The Oil Shock: Reassessing the Outlook for Growth, Inflation, and Capital Markets

Macro Indicators: The economic backdrop remains solid but is getting bumpier. Inflation remains stubbornly above the Fed’s 2% target and chaotic tariff policy is only adding fuel to that fire. Growth is slowing, with GDP decelerating from 2.8% in 2024 to 2.2% in 2025, and Q4 coming in at a soft 1.4%. Meanwhile, the labor market is quietly losing steam, with unemployment hitting 4.3% in January as AI-driven job cuts move from headline risk to reality.

Trump 2.0: The Supreme Court dealt the Administration a legal blow, ruling its IEEPA tariffs unconstitutional, but the White House pivoted fast, slapping a 10% tariff back on under a different law (Section 122 of the Trade Act of 1974). The clock is now ticking as Congress has 150 days to approve an extension of the tariffs, setting up a high-stakes vote in the middle of re-election season. On the geopolitical front, a joint U.S.-Israel military operation in Iran resulted in the assassination of Iran’s Supreme Leader, sending geopolitical risk sharply higher and putting global markets on edge to end the month.

Fed & Monetary Policy: Rates are expected to stay on hold through the end of Chair Powell’s tenure. His likely successor, Kevin Warsh, is expected to come in with a rate-cutting bias and a desire to slim down the Fed’s balance sheet, but the macro data may threaten these plans.

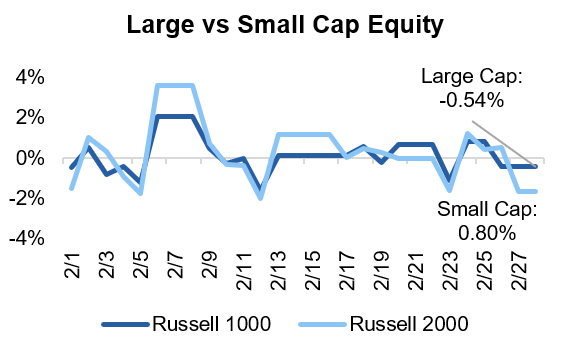

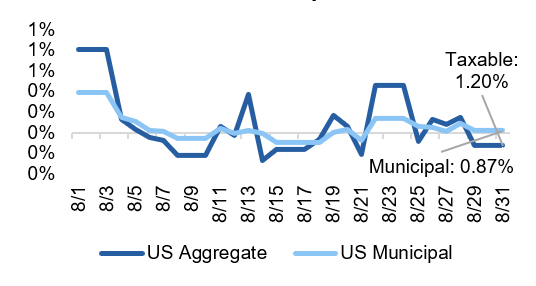

Capital Markets: February was a rough month for U.S. stocks, which saw broad declines, with investors quietly rotating out of last year’s darlings (tech and financials) and into energy and materials. Meanwhile, international equities kept outpacing domestic ones, with emerging markets standing out as a particularly attractive pocket of value. On the fixed income side, yields held relatively steady and credit spreads remain tight by historical standards.

Asset Class Performance

U.S. large cap equities posted negative returns in February as AI pressures prompted sell-offs in the technology and financials sectors. Longer-term Treasury yields declined over the month, contributing to positive total returns. International equities continued their run-up, driven by Asian markets.

Source: YCharts. Asset class performance is presented using total returns for an index proxy that best represents the respective broad asset class. U.S. Bonds (Bloomberg U.S. Aggregate Bond TR), U.S. High Yield (Bloomberg U.S. Corporate High Yield TR), International Bonds (Bloomberg Global Aggregate ex-USD TR), U.S. Large Cap (S&P 500 TR), U.S. Small Cap (Russell 2000 TR), Developed International (MSCI ACWI ex US TR), Emerging Markets (MSCI EM TR), and Real Estate (Dow Jones U.S. Real Estate TR).

Markets & Macroeconomics

A Lot to Digest

One year into President Trump’s second term and markets have been taken on a wild ride, and February was no exception. The Supreme Court struck down IEEPA tariffs, but the White House didn’t skip a beat: a new 10% tariff was back in place almost immediately, this time under a different law (Section 122 of the Trade Act of 1974). The message? Tariffs aren’t going anywhere. The catch? Section 122 tariffs expire after 150 days unless Congress votes to extend them. That vote lands in mid-July – right in the middle of re-election season, with midterms in November. Expect politics to get very tangled with policy as we progress through the year.

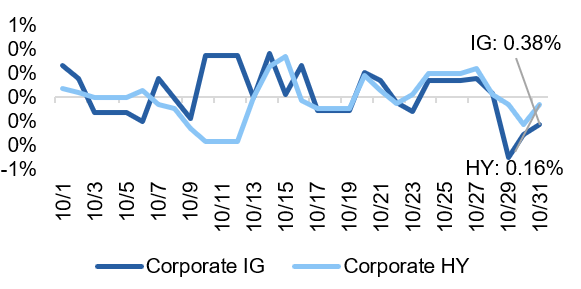

Exhibit 1: Effective Federal Funds Rate

Sources: FRED, Federal Reserve Board

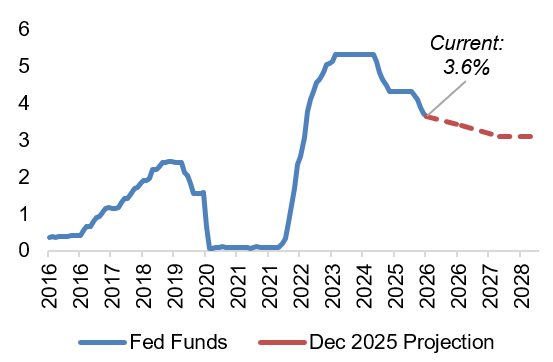

On the rates front, uncertainty continues to be the name of the game. Current Fed Chair Powell is on his way out, with Kevin Warsh set to take the helm in May. Fed officials expect interest rates to settle around 3.0% by the end of 2028, illustrated in Exhibit 1, but the road there is anything but clear. Normally, slowing growth and a softening job market would be a green light to cut rates. However, tariffs and fiscal policy continue to pose challenges for the Fed, meaning any hint of rising inflation could pump the brakes on cuts entirely. Warsh has also made no secret of wanting to shrink the Fed’s balance sheet, a move that would effectively tighten financial conditions even if rates are being cut. Per usual, the path forward for monetary policy remains unclear and highly dependent on macroeconomic data.

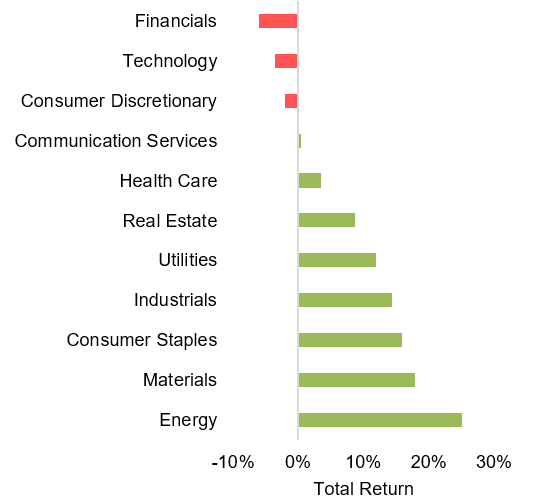

Exhibit 2: Year-to-Date Equity Sector Returns

Source: YCharts. Data through 2/28/26.

AI is still the topic du jour, but lately it has become a source of turbulence, not just excitement. Some of last year’s biggest winners, like the financials and tech sectors, have flipped to become the worst performers this year, illustrated in Exhibit 2. And just when markets had enough to chew on, geopolitical turmoil reared its ugly head with fresh conflict in Iran to end the month. Middle East instability and oil prices have a long history together, and a prolonged conflict in the region could stoke domestic inflation just as these concerns had started to fade, reigniting not just the potential for further price increases, but the dreaded stagflationary environment. So how should investors make sense of all this? The short answer is stay diversified and look for value rather than just safety. One of the most important things to keep in mind is that markets don’t move on headlines, they move on surprises. The risks everyone is already talking about? They are largely priced in. The real wildcard is always the risk nobody is modeling yet.

The Bottom Line: The market continues to digest a lot – tariff turmoil, Fed leadership changes, midterm election build-up, geopolitical risk, and AI implications – but the real danger isn’t what’s making headlines; it’s what isn’t, making valuations and current market expectations the most important things for investors to keep in focus.

Looking Ahead

Where Are We in the Market Cycle?

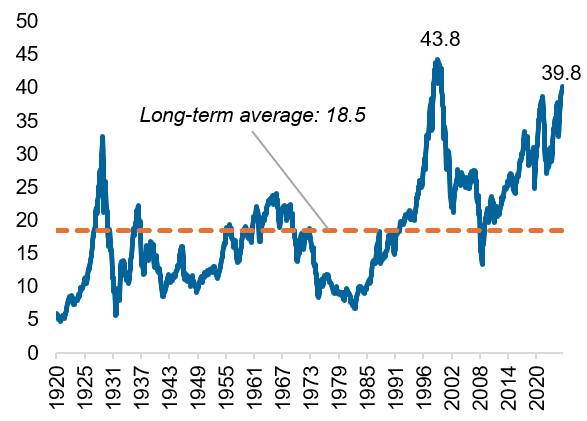

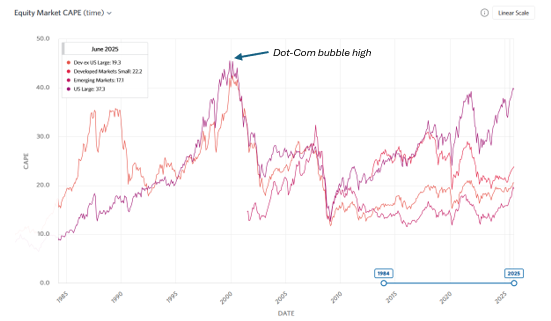

The business cycle refers to the natural fluctuations in the economy over time, implying that the economy moves through periods of expansion and contraction. The business cycle is broadly comprised of four stages: recovery, expansion, late cycle, and recession. There is no set length of a business cycle, meaning the only way we can determine where we are in the cycle is by looking for clues. Right now, the clues are increasingly pointing to a late cycle environment.

What does late cycle look like? This cycle stage is broadly characterized by slowing economic growth, tighter monetary policy, pricey markets, and widening credit spreads. More anecdotally, this stage can also be characterized by excess – leverage, investor exuberance, and a “nothing can go wrong” attitude, characteristics we are seeing in today’s environment. On the valuation front, the numbers are hard to ignore. The Shiller Cyclically Adjusted P/E or “CAPE” ratio, widely considered the gold standard for measuring whether stocks are cheap or expensive, is at levels only seen once before in history: early 2000, right before the Dot-Com bubble burst, illustrated in Exhibit 3. While there is real earnings growth propping up these valuations, history suggests these stretched ratios are far more likely to come down than go higher moving forward.

Exhibit 3: Historical CAPE Ratio for the S&P 500

Source: YCharts

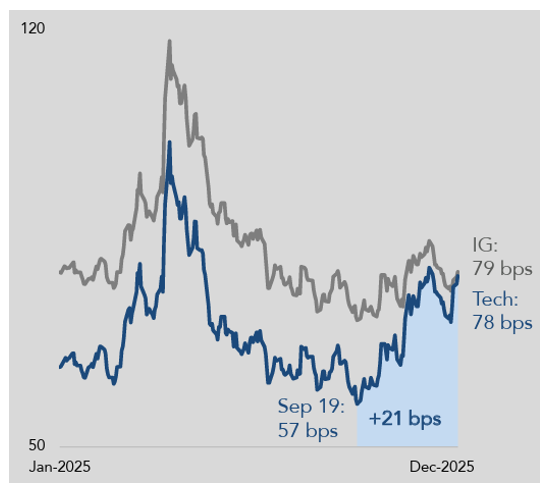

The credit markets are flashing similar signals of excess and late cycle behavior. The biggest AI players are spending at eye-watering levels to build out infrastructure, and they are increasingly borrowing to do it. These companies have historically had fortress balance sheets and ratcheting up debt issuance will naturally reduce the quality of their financial statements. Some hyperscalers, like Meta, are even using Special Purpose Vehicles to keep debt off their balance sheets – a type of financial engineering that is classic late cycle behavior. While some of these trends may raise eyebrows, including increasing investment grade spreads in the tech sector, illustrated in Exhibit 4, late cycle doesn’t mean sell everything. Stages of the business cycle can last longer than anyone expects, but it does warrant attention from investors with February’s market rotation serving as a preview. Investors are already quietly repositioning toward tomorrow’s opportunities, but the playbook here isn’t to chase what has been hot, but rather to stay anchored to valuations and think about where you want to be when the cycle turns.

Exhibit 4: Investment Grade (IG) Index vs. IG Tech Spreads

The Bottom Line: Today’s market is flashing a late cycle warning with stretched valuations and rising leverage. Rather than chase yesterday’s winners, investors should be thinking about valuations and where they want to be positioned when the music stops.

Capital Markets Themes

What Worked, What Didn’t

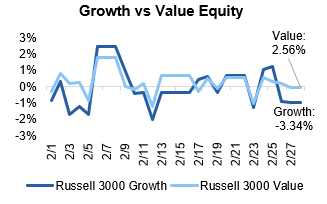

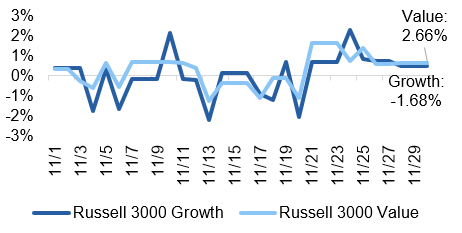

•Value Continues its Outperformance: Growth stocks had another rough month as lofty tech valuations continued to deflate, a trend that has been gaining steam since late 2025.

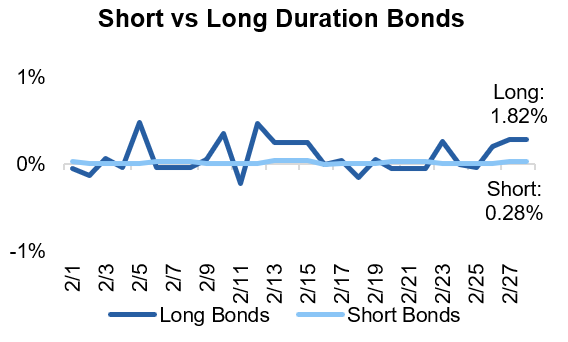

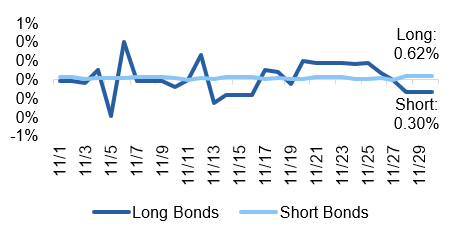

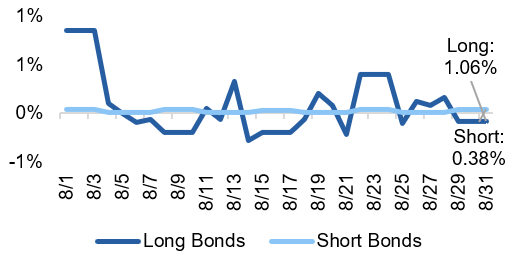

•Long Duration Looks Attractive: With uncertainty running high, investors fled to safety and pushed further out on the yield curve, rewarding long duration bonds with a 1.82% return in February.

•Large Cap Equities Falter: U.S. large cap equities slipped into the red as investors rotated away from risk assets. The culprits? A trifecta of fiscal policy uncertainty, geopolitical tensions, and AI-driven disruption. The trade that worked for years is showing cracks.

Source: YCharts. Data call-out figures represent total monthly returns.

On Alternatives

The Basics of BDCs

Business development companies or “BDCs” have been in the headlines recently, prompting an explainer on what they are, why investors like them, and why they have been coming under pressure. At their core, BDCs pool investor money and either lend it out or take equity stakes in small and mid-sized businesses that cannot easily do business with a big bank. They are required to pay out at least 90% of their taxable income as dividends, which makes them a natural fit for income-hungry investors. Some BDCs trade on public exchanges with a daily price, while others are non-traded and harder to access. The appeal for retail investors is high yields, but these yields typically come with a more concentrated portfolio. BDCs are not known to spread risk across hundreds of positions – instead, they are more concentrated in specific sectors and parts of the capital stack. This type of approach is fine in calm markets, but in choppy ones, there is no natural cushion when something goes wrong. Additionally, loans are typically more difficult to trade than stocks, creating additional difficulties when everyone heads for the exit at once.

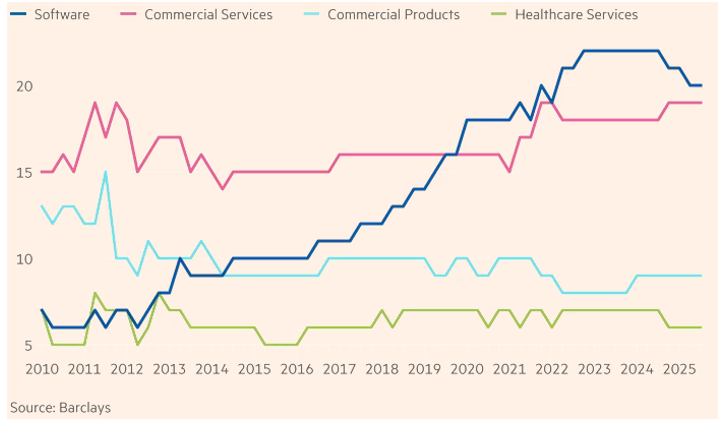

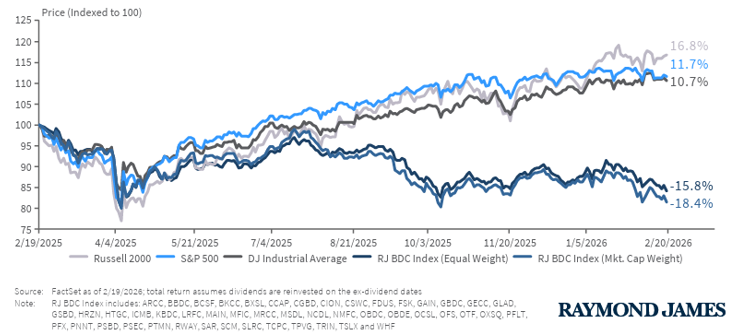

So why are BDCs in the news today? Over the past decade, they have steadily loaded up on software companies – and for good reason. Enterprise software historically has had low default rates thanks to sticky customers and a predictable, recurring revenue stream, prompting BDCs to increase their exposure, illustrated in Exhibit 5. With rapid advancements in AI in recent months, this thesis is starting to crack open, threatening not just the revenues of these software companies, but their existence as a whole. While the AI-driven sell-off in BDCs began in earnest in mid-2025, illustrated in Exhibit 6, it has accelerated in recent weeks, fueling headlines. Importantly, the structure of BDCs has played a role in this sell-off – the combination of daily pricing, a concentration in illiquid underlying holdings, and a roughly 20% exposure to software created the perfect storm. The lesson here is not that BDCs are bad investments, but that an investment’s vehicle is an important consideration. Put another way, investors should be reminded that it is not simply what you own that matters, but how you own it. When markets get jittery and everyone rushes for the door at once, structure matters just as much as substance.

The Bottom Line: Publicly traded BDCs have experienced drawdowns recently thanks to their heavy concentration in software, a sector now squarely in AI’s crosshairs, and the resulting sell-off is a masterclass in why vehicle selection matters just as much as manager selection, especially in private markets.

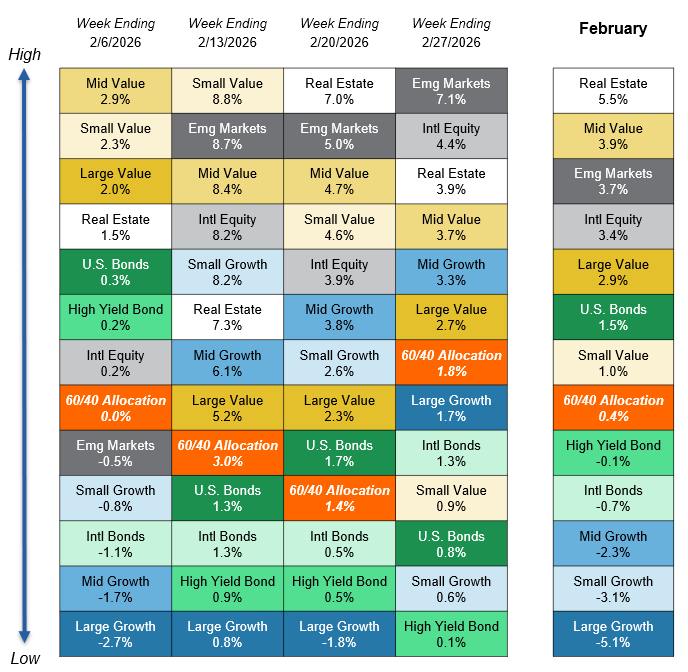

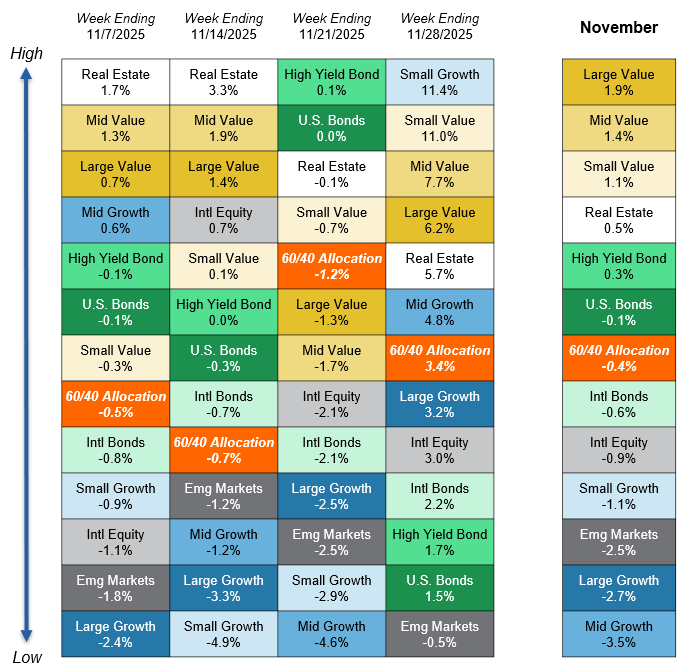

Asset Class Performance Quilt

Markets are ever-changing, making diversification across asset classes and sectors a critical component to portfolio construction. As illustrated below, a Balanced 60/40 portfolio provides greater consistency of returns and less volatility over time.

Source: YCharts. Asset class performance is presented using market returns from an exchange-traded fund (ETF) proxy that best represents its respective broad asset class. Returns shown are net of fund fees for and do not necessarily represent performance of specific mutual funds and/or exchange-traded funds recommended by Centura Wealth Advisory. The performance of those funds may be substantially different than the performance of broad asset classes and to proxy ETFs represented here. U.S. Bonds (iShares Core U.S. Aggregate Bond ETF); High Yield Bonds (iShares iBoxx $ High Yield Corp Bond ETF); Intl Bonds (Invesco International Corporate Bond ETF); Large Growth (iShares Russell 1000 Growth ETF); Large Value (iShares Russell 1000 Value ETF); Mid Growth (iShares Russell Mid-Cap Growth ETF); Mid Value (iShares Russell Mid-Cap Value ETF); Small Growth (iShares Russell 2000 Growth ETF); Small Value (iShares Russell 2000 Value ETF); Intl Equity (iShares MSCI ACWI ex US ETF); Emg Markets (iShares MSCI Emerging Markets ETF); and Real Estate (iShares US Real Estate ETF). The return displayed as “60/40 Allocation” is a weighted average of the ETF proxies shown as represented by: 40% U.S. Bonds, 12% International Stock, and 48% Large Blend.

https://centurawealth.com/wp-content/uploads/2024/11/iStock-1816227914.jpg12242448Cailyn Changhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngCailyn Chang2026-03-06 11:47:282026-03-06 11:49:14Market Month in Review – February 2026

Macro Indicators: Inflation measures remain above the Fed’s long-term 2% target; however, there are greater concerns about the labor market, which is experiencing softening amid the “low hire, low fire” environment. GDP growth is surprising to the upside with third quarter data showing growth of 4.4%, driven by strong consumer spending and business investment, particularly within the technology sector.

Trump 2.0: The President made his nomination for the new Fed Chair, Kevin Warsh, who is expected to replace current Fed Chair Jerome Powell in mid-May. The Trump Administration also increased geopolitical pressures over the month, with the forced removal of Venezuelan President Maduro, threats to take over control of Greenland, and increased pressure on Iran. Tariffs remain in place unless the Supreme Court rules they are illegal.

Fed & Monetary Policy: The Federal Open Market Committee (FOMC) left interest rates unchanged in January. Current Fed Chair Powell’s term ends in mid-May and it is still undetermined whether he will stay on the Board after the fact. While concerns about Fed independence re-ignited over the month as the Department of Justice initiated a criminal probe into Chair Powell over the costly renovation of the Fed’s HQ, President Trump’s pick of Kevin Warsh as the next Chair quelled concerns.

Capital Markets: Geopolitical shocks and policy moves prompted volatility in commodity markets like gold and silver alongside continued weakness in the U.S. Dollar, but these trends reversed upon Warsh’s nomination. Early earnings releases point to another solid quarter, but elevated expectations in the tech sector fueled volatility across equity markets.

Asset Class Performance

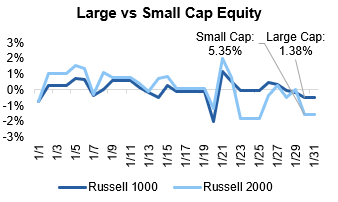

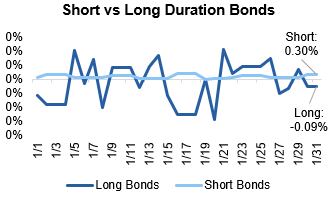

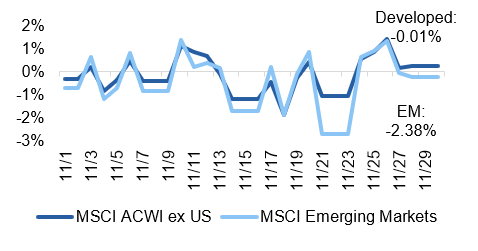

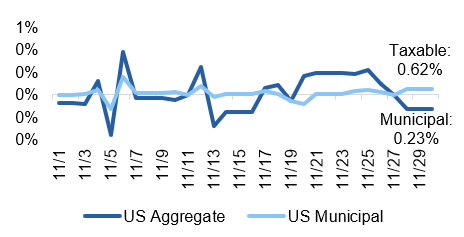

After a stand-out performance in 2025, international equities continued the momentum in January, outpacing domestic equity markets. Within the U.S., small cap stocks outperformed large cap stocks, and fixed income markets experienced relatively muted performance to kick-off the first month of the new year.

Source: YCharts. Asset class performance is presented using total returns for an index proxy that best represents the respective broad asset class. U.S. Bonds (Bloomberg U.S. Aggregate Bond TR), U.S. High Yield (Bloomberg U.S. Corporate High Yield TR), International Bonds (Bloomberg Global Aggregate ex-USD TR), U.S. Large Cap (S&P 500 TR), U.S. Small Cap (Russell 2000 TR), Developed International (MSCI ACWI ex US TR), Emerging Markets (MSCI EM TR), and Real Estate (Dow Jones U.S. Real Estate TR).

Markets & Macroeconomics

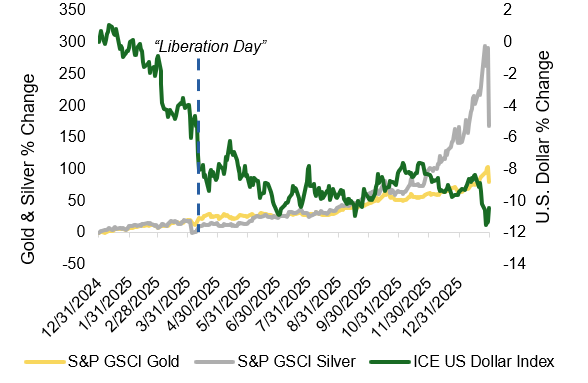

Does Interest in Gold & Silver Spell Trouble for the Dollar?

Ever since the Trump Administration’s “Liberation Day” in April 2025, markets have witnessed a broader diversification away from U.S. assets, prompting a decline in the global reserve currency. President Trump’s policies, in addition to concerns over persistent federal deficits, have popularized a “debasement trade,” a trade centered around a fall in value of a currency, in this case, the U.S. dollar. This trade has manifested itself in metal markets, which can be used as a hedge against a falling dollar, prompting greater interest and precipitous rises in the prices of gold and silver over the past year, illustrated in Exhibit 1.

Exhibit 1: Gold, Silver & U.S. Dollar Returns

Sources: YCharts

Geopolitical concerns are likely also driving commodity prices to start the year as global tensions have risen in place like Venezuela, Greenland, and Iran, most of which have been precipitated by the U.S. This combination of factors caused gold and silver to hit record highs in January, with gold prices topping $5,500/oz, nearly doubling in price since the beginning of 2025. Silver has experienced a more speculative run-up, surging to over $121/troy oz in January. While both metals offer intrinsic value that is attractive during currency downtrends, silver’s role as an industrial component, specifically for AI hardware, has helped fuel its growth. This dual purpose is likely responsible for silver’s parabolic rise that began last fall, but it can also lead to greater volatility than its gold counterpart.

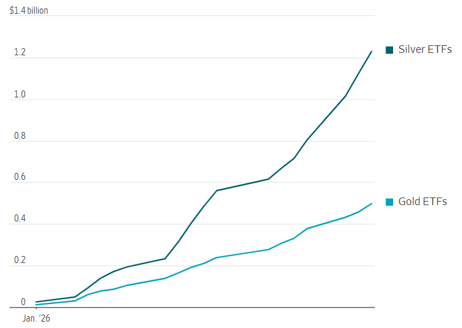

The U.S. dollar index is trading at lows not seen since 2022, and this depreciation is a concern for markets, with retail participants driving the surge in gold and silver, illustrated by the rise in ETF flows in Exhibit 2.

Exhibit 2: Cumulative Net Retail Flows

Source: Vanda Research (via Wall Street Journal)

President Trump acknowledged the dollar’s depreciation this month and, unlike markets, demonstrated a lack of concern. There are reasons why a falling dollar could be a good thing, including increasing the global competitiveness of domestic producers and domestically-manufactured goods abroad; however, there are some perils to a depreciating currency, like potential inflationary effects of higher import costs and a general erosion of confidence in the nation. Amid the current uncertain policy backdrop, investors are looking for reassurance that U.S. assets are a “safe” investment. The announcement of new Federal Reserve Chair Kevin Warsh offered much-needed comfort about Fed independence to markets to end January, prompting a rise in the dollar and a subsequently volatile fall in gold and silver. Time will tell on whether the debasement traders are correct, but, for now, the U.S. dollar remains the world’s most utilized currency.

The Bottom Line: President Trump’s policies, rising federal deficits, and geopolitical concerns have driven gold and silver prices to new highs, fueling the “debasement trade;” however, the recent appointment of new Fed Chair Kevin Warsh prompted a reassuring reversal in this trade to end January, illustrating how much markets are focused on policy decisions in the U.S.

Looking Ahead

Policy Remains at the Forefront

The month ended with monetary policy headlines: interest rates were held steady at the January FOMC meeting and President Trump nominated former Fed Governor Kevin Warsh as the new Fed Chair. This nomination came after intense speculation over who would replace current Chair Powell amid threats to central bank independence from the Trump Administration. The choice of Warsh, once a self-proclaimed “hawk” or a governor who supports higher interest rates, brought initial reassurance to independence concerns to close out the month.

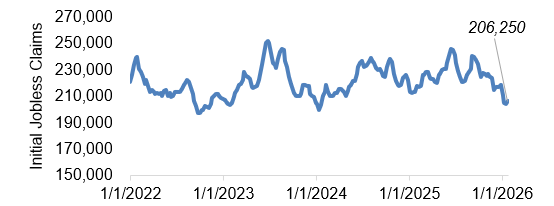

Now that markets have clarity on the next Fed Chair, attention can turn back to what matters most: the health of the economy. According to CME FedWatch, markets are currently expecting one to two 25-bps interest rate cuts in 2026 as inflation remains above-target, the labor market cools, and economic growth remains robust. The labor market remains the key concern for policymakers: major layoffs were announced by Nike, Amazon, UPS, and Home Depot in January, and the post-college graduate working cohort is experiencing the highest rates of unemployment, even as broader federal unemployment remains steady around 4.4%.

Exhibit 3: 4-Week Moving Average of Initial Jobless Claims

Source: FRED

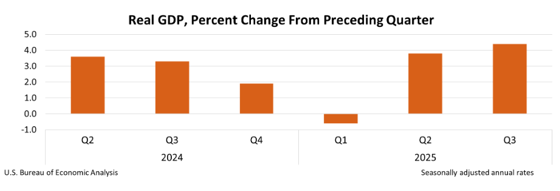

Part of why the unemployment rate has not ticked higher is due to stricter immigration policies from the Trump Administration, which has contracted the amount of labor supply in the market, which, when met with more muted labor demand, has kept the unemployment rate moderate by historical standards. While labor softening trends are evident, other metrics support a relatively stable labor market, like the 4-week moving average of initial jobless claims, illustrated in Exhibit 3 with levels above 250,000 typically signaling greater labor market weakness. Should the labor market begin deteriorating across numerous metrics, the Fed is likely to cut interest rates more aggressively. One reason holding the Fed back from cutting interest rates further in 2026 is robust GDP growth, illustrated in Exhibit 4. While tariffs have skewed some of the GDP data, the key driver of economic growth has been consumer spending, followed by business investment, which has been fueled by AI capex.

Exhibit 4: GDP Growth

Source: FRED

Despite gloomy survey data, the American consumer continues to spend, and the Trump Administration is hoping this trend continues in the lead-up to midterm elections in November. As we look ahead to the next 11 months of 2026, there are a few key policy matters to keep on the radar: 1) the “One Big Beautiful Bill” Act is expected to deliver a bumper crop of income tax refunds this spring, padding consumers’ wallets and supporting economic growth; 2) the Supreme Court will rule on the legality of the majority of President Trump’s tariffs, which could usher in a reversal of existing tariffs in their current form as well as add further uncertainty about how to unwind the tariffs; 3) rhetoric from the new Fed Chair about how he plans to manage the central bank’s dual mandate differently than his predecessor; and 4) the all-important midterm elections. All in all, the U.S. economy remains in solid condition, but with a changing of the guard at the Fed occurring in mid-May and an unpredictable fiscal policy agenda with major elections late this year, volatility is expected. Investors should understand the policy backdrop, but, at the end of the day, valuations should drive investment decision-making, not who is in charge at the Fed or whether the government is shut down.

The Bottom Line: Both fiscal and monetary policies are expected to be a driving force in 2026 as the Trump Administration focuses on spurring growth and the Fed manages its dual mandate under new leadership, with all eyes on the midterm elections later this year.

Capital Markets Themes

What Worked, What Didn’t

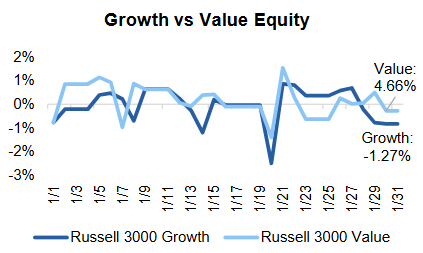

•Value Outperforms: Value stocks outperformed their growth counterparts as tech valuations continued to come under pressure, following a trend set at the end of 2025.

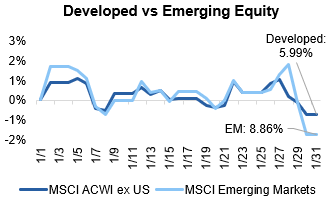

•International Run Continues: International equity markets continued their run-up in January after a banner 2025, with emerging markets outperforming developed international equities, boasting cheaper valuations and a boost from a depreciating U.S. dollar.

•Is this the year for small caps?: Small cap stocks outperformed their large counterparts in January, and the asset class’s outlook involves a positive earnings growth picture and a supportive environment as interest rates expect to decline further.

Source: YCharts. Data call-out figures represent total monthly returns.

On Alternatives

How IPOs and M&A Activity Shapes Private Equity Returns

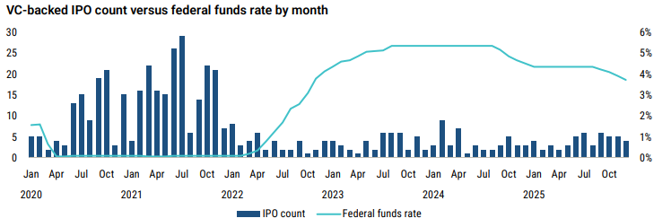

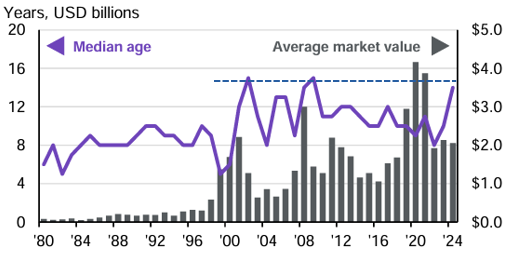

Private equity value creation is driven by several factors, but investor returns ultimately depend on successful exits. IPO (Initial Public Offering) and M&A (Mergers & Acquisition) activity are the primary pathways that allow private equity firms to realize gains and return capital to investors. To understand why these exit channels are so critical, it helps to first look at how private equity (PE) firms generate value. While not all private equity firms operate identically, most follow a similar model: acquiring companies they believe are undervalued or can be operationally improved, with the goal of selling them later at a higher price. However, these strategies only translate into investor returns if firms are able to access viable exit opportunities. There are three main channels that PE firms use for exits: 1) IPO – the gold standard, typically offering the highest upside potential 2) Strategic – the sale of a portfolio company to another company looking to grow or strengthen its business (often through M&A) 3) Secondary Market – the sale of a portfolio company to another PE firm that believes it can create additional upside. These three exit channels work in harmony to ultimately drive returns for PE funds and their investors.

Exhibit 5: IPO Count vs Federal Funds Rate

Source: PitchBook

As with many sensitive ecosystems, when a new variable is introduced, it has the capacity to disrupt the entire system. Enter the Federal Funds Rate. For years following the GFC (Global Financial Crisis), interest rates hovered near zero.

After the pandemic and subsequent government stimulus, inflation ran rampant, forcing the Fed to raise rates and disrupt the homeostasis of these markets. As interest rates rose, the cost of borrowing increased, causing growth to become more challenging. During this time, IPO activity faced a steep decline, illustrated in Exhibit 5.

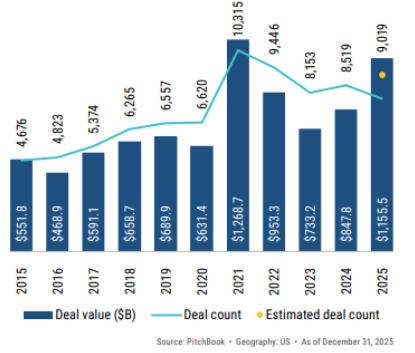

Exhibit 6: PE Deal Activity

Knock-on effects included a reduction in M&A activity and a general slowing of PE deal flow. This slump has resulted in fewer exits for PE, which in turn has delayed capital returning to investors and made the fundraising environment more challenging for new funds looking to raise capital. While activity remained challenging, 2025 was expected to mark a resurgence and reopening in the market. Tariff-related volatility in the first half of ’25 delayed that recovery, but once markets adjusted, the second half of the year began moving in the right direction. As shown in Exhibit 6, 2025 trended positively, with deal activity in both count and value reaching the highest levels since ’21 peaks. Looking forward to ’26, we expect this trend to continue, bolstered by AI-driven efficiency improvements and continued investment, additional rate cuts under new Fed leadership, and an administration focused on positive economic sentiment heading into the November midterm elections.