At Centura Wealth, we are committed to our clients and their goals. We take our role as stewards seriously and align their goals with our implementation.

This means communication throughout the small life events and changes, and the big “money in motion” events that can bring stress to a family. We are here to take the decision-making burden off your plate.

Communication, Communication, Communication!

Communication is key. This is a phrase thrown around a lot, but it still rings true for wealth advisors. This means that through the constant changing of tax laws or personal life changes, we are transparent with our clients.

There are studies that show that overall, clients want more communication. Over time, there has been a shift in expectations for the relationship between wealth advisor and client— the expectation is hearing from your advisor four times a year.

ReachStack released some alarming statistics about advisor communication that deserve our attention:

“64% of clients hear from their advisor less than 4x a year

50% of clients did not hear from their advisor in the first 3 months of the Pandemic

Yes 85% of clients say advisor communications impact retention & referrals.”

These numbers show the shift that Centura Wealth is hoping to achieve as the standard for wealth management across the board.

Understanding Client Expectations

Client expectations are most successful when established from the beginning. For example, in the age of Zoom, one expectation we might have with our clients is to agree to have the cameras on. There can be miscommunications if a client and advisor are not discussing a financial strategy face-to-face.

If this expectation is set from the beginning between both parties, then there should be no surprises throughout the process of creating a financial plan.

Dynamic Tax Planning

We understand that tax planning needs to be dynamic because tax laws are constantly changing. As advisors, it is our responsibility to be on top of these changes.

Dynamic tax planning is also part of our core because with the responsibility of being a steward; dynamic tax planning is crucial.

There are various factors that contribute to the efforts of dynamic tax planning, which include:

“Timing of income

Size

Timing of purchases

Planning for expenditures.”

These factors are the foundational efforts of dynamic tax planning. For example, the estate tax going into 2022 is likely changing drastically and is a conversation we need to present to our clients.

Staying on Top of Complexities

What do clients actually value in a financial advisor? They just want the advisor to care. Simple enough, right?

Well, there are many complexities when it comes to wealth. We’ve found that wealthy families and individuals carry wealthy burdens. On top of the complexities of changing tax laws, there are changes in family structures, goals, and situations.

With these changes come time-sensitive decisions that the advisors at Centura Wealth take seriously as part of their role.

Things happen quickly so it’s crucial that our advisors keep in touch with our clients. As the survey mentioned above, the general consensus from clients is that they do want to hear from their financial advisors more frequently.

In the end, keeping consistent communication with our clients about financial and personal events is essential. At Centura, one way we like to keep in touch with clients is by consistent Stewardship meetings on a frequency that is agreed upon with the client.

Predicting Client Needs (Past Logistics!)

Picture this:

There is a sudden death in a family, and the looming responsibilities of the immediate family members are already a lot to handle. The already emotional time has the added stress of figuring out financial and succession planning.

But, you haven’t heard a word from your family’s financial advisor. Even if there isn’t a solidified plan for what’s next, when your advisor is willing to communicate, even as simple as, “We’re so sorry for your loss. When you’re ready, we’re here to discuss upcoming financial plans and goals” it makes you feel valued.

Predicting clients’ needs is another way stewardship is at the core of Centura. We recognize that a client is going to need kind direction in the case of sudden life changes. This means our advisors think about what could happen in the future and plan accordingly.

Have these reminders of stewardship made you want to solidify the trust in your relationship with a wealth advisor or client? Start the conversation with the five questions to ask your financial planner.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1049858430.jpg14142121Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2021-12-04 17:04:002025-04-08 16:22:15Why Stewardship is at the Core of Everything We Do

While the terms “wealth manager” and “financial advisor” may be grouped together or used interchangeably, the two professions actually have quite a few significant differences. Individuals looking for assistance in their financial planning should be familiar with these differences to find the best professional help for them and their financial situation.

What is the Difference Between a Wealth Manager and a Financial Advisor?

In simple terms, the difference between a financial advisor and a wealth manager lies in the clients and the forms of wealth they manage.

Financial advisors manage the financial situation of a client. Wealth managers are a type of financial advisor often associated with clients with a high net worth. Both professionals manage and assist with financial planning, but wealth managers typically specialize in assisting clients with large amounts of wealth.

Let’s explore these definitions to learn which would be ideal for your financial needs.

What is a Financial Advisor?

Financial advisors assess and manage the financial status of their clients as well as help them reach their financial goals. Financial advisors manage several aspects of a client’s financial situation, ranging from retirement planning, savings, investing and estate planning.

A financial advisor provides a broad group of services, encompassing most client needs. A financial advisor also has a broader range of clientele compared to a wealth manager. While wealth managers work almost exclusively with high-net-worth clients, financial advisors have a wider range of clients.

Most wealth managers have a minimum net worth amount required to begin an engagement, whereas financial advisors typically do not set a barrier to entry. Individual firms will have criteria by which they determine the suitability of the relationship based on complexity, assets, and expertise.

There are different types of financial advisors who serve a variety of client needs. A Certified Financial Planner (CFP) will work with clients to craft portfolios and future financial planning – this is often focused primarily on retirement planning. A certified public accountant (CPA) may be a part of a financial advisory team to aid in tax planning (consulting) and preparation (compliance), or clients may choose to have a separate CPA relationship.

Although there are different types of financial advisors, with specific expertise and areas of interest, here are some of the overarching services a financial advisor may provide:

Developing a financial plan

Savings allocations

Retirement planning

Tax planning

Inheritance and Trust creation

College funding

Business exit or succession planning

Wealth Manager

Wealth managers are a subgroup of financial advisors, so they provide more specific advice and services. When looking to Liberate Your Wealth®, understanding what each professional provides will save you time and money when choosing the right partnership.

A wealth manager typically works with high-net-worth clients and provides a personal, deeper level of financial management. A High Net Worth Individual (HNWI) falls into the range of a net worth of $1 million or more of liquid investable assets. Their clients’ asset threshold is one of the biggest differentiators between wealth managers and financial advisors. Wealth managers are typically employed by banks, private firms, and brokerages to work with high- net-worth clients.

Since wealth managers mostly work with high-net-worth individuals, they are more hands-on with a family’s or individual wealth. Some of the services that would fall under the wealth manager’s role include:

Investment management

Estate planning

Risk management

Capital gains planning

Philanthropic gifting

Legacy planningTax planning

Real Estate transaction planning

Do You Need a Financial Advisor or a Wealth Manager?

Consider Minimum Asset Requirements

When choosing between these two forms of financial professional help, individuals should consider minimum asset requirements to open an account. Wealth management firms may require a minimum of $250,000 while others require $1 million or even $10 million just to open an account.

While every wealth manager may not require large minimum asset requirements, most might. Individuals who can’t or do not want to comply with these requirements may fit better with a financial advisor.

Do You Want a Hands-on Approach?

Wealth managers typically have a more hands-on approach than financial advisors. If you prefer to simply check in a few times per year, consider a financial advisor instead of a wealth manager.

Any Questions?

Contact Centura Wealth Advisory today to find the financial professional who will help you achieve your financial goals.

As a wealthy individual, family, or institution, you likely carry the burdens of wealth. This includes its complexities, the responsibilities to do right, and the duty to find efficiencies, reduce risk and protect wealth. Learn more about us and liberate your wealth in 5 easy steps.

Or, read on to learn how to plan and invest in a high interest rate environment, here.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1189065444.jpg14142119Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2021-10-03 17:50:002025-04-08 16:16:36Wealth Manager vs. Financial Advisor: What’s the difference?

Professionals have compared structured notes to the innovative mindset behind mutual funds—with the main draw being zero interest rates. In the past, structured notes were a high-risk, high-return investment that only very wealthy investors could get involved in. Recently, however, the transition to using more technology for investing has opened the door for more individuals and families to invest using structured notes.

Centura Wealth Advisory works with clients to build a diversified portfolio when financial planning, and considering structured notes is a step toward having a more diverse portfolio.

Listen to the recent Live Life Liberated podcast, “Structured Notes Simplified with Robert Sowinski,” for a professional perspective.

What Are Structured Notes?

There are different types of structured notes that can be helpful to understand before investing.

There are a few categories to know for understanding structural notes:

Maturity

Underlying Asset

Protection Amount

Return/Payoff

Structured notes can be compared to a “hybrid security.” They combine the features of various financial products into one. Structured notes combine bonds and additional investments to offer the features of both debt assets and investment assets.

Structured notes aren’t direct investments, but derivatives. They track the value of another product. The amount on a structured note will depend on the issuer repaying the premium and underlying bond.

How do they work?

The basic ways structured notes can be ‘structured’ are the following:

Provide downside market protection

Provide upside (or enhanced) participation

Provide regular payments/income in the form of coupons if certain market conditions are met

Provide a payout/return at maturity if certain market conditions are met

The U.S. Securities and Exchange Commission (SEC) provides more detailed information on structured notes: “Structured notes have a fixed majority and include two components—a bond component and an embedded derivative.”

Financial institutions, as a result, are generally responsible for designing and issuing structured notes, so then the Broker/Dealer can sell them to individual investors.

Potential Risks

It’s important to understand that structured investments will not be a perfect match for all investors based on their risk profile and current portfolio. They are risky as your investments can sit idly without growth

The SEC lists the risks that come with investing in structured notes:

Market Risk

Insurance Price and Note Value

Liquidity

Payoff Structure (which is affected by participation rates, capped maximum returns, and knock-in feature)

Credit Risk

Call Risk

Tax Considerations

Talk to us!

If you’re interested in structured notes and diversifying your portfolio, speak to one of our trusted financial advisors today.

https://centurawealth.com/wp-content/uploads/2024/08/Should-You-Consider-Adding-Structured-Notes-to-Your-Portfolio.jpg14092128Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2021-09-05 17:57:002025-04-08 16:16:36Should You Consider Adding Structured Notes to Your Portfolio?

Trust us, it’s never too early to start year-end financial planning.

Year-end is about so much more than just your financial statements. The right year-end planning allows individuals to make the most out of their financial plans and tax strategies while also monitoring their current progress.

Centura Wealth Advisory believes that there are ways to liberate your wealth—that process can be made possible through financial planning.

What are some advantages of getting ahead of the curve? You may be able to:

Lower your taxes with retirement contributions and charitable gifting

Offset taxes on investment gains by selling some assets

Adjust your budget to meet your financial goals as they change

Whether you’re focused on building wealth, fine-tuning your portfolio or preparing for retirement, there are things you should consider before December 31st.

Below are a couple of steps to follow for your annual financial planning. Let’s take the opportunity to get ahead of the curve and reach your financial goals.

First, What is Year-End Financial Planning?

In its simplest terms, year-end financial planning is a way to determine where you are financially as the year comes to a close.

A successful financial plan can help you:

Assess your budget

Cash flow

And other assets

A financial plan can reduce negative spending habits, help manage taxes, savings, debt and more as well as push individuals towards their financial goals.

Now, let’s take a look at some steps to take in your year-end planning.

Review Your Mortgage

It’s unlikely that you want to deal with a mortgage, but there are many benefits to conducting an annual mortgage review. Why? The factors which drove you to that loan choice – such as finances – have likely changed since after the settlement. By taking the time at the end of the year to review your mortgage, you can be sure the loan you have is still the best choice for your financial situation.

For instance, maybe you’re working from home long-term and want to move to a new area, maybe you’re just ready for a change of pace. Either way, evaluating your current mortgage and adjusting can help future plans be set in motion.

Tax Loss

Year-end financial planning should also include a look at your taxes. While Tax Day may not be until April 15th, getting ahead on tax preparation can be beneficial.

Centura Wealth Advisory specializes in tax planning for different categories including:

Short Range Tax Planning

Long Range Tax Planning

Permissive Tax Planning

Purpose-Driven Tax Planning

Some professionals believe in a tax-loss method as a way to invest in returns, but each family and institution is different.

Our investment philosophy is centered around achieving the best absolute returns given a range of likely outcomes. We achieve this through passive investment management, and by offering a unique set of alternative investments that can bring an excess return to your portfolio.

General Planning

Consider what’s coming in the next few months and beyond. The holidays can become spendy and might require further budgeting. This is another reason why financial planning can never be started too early. It can be tempting to wait until after the holidays, but if you start now then there is greater room for financial liberation.

Let’s Talk Insurance: Time to Review Your Coverage

Insurance policies have a tendency to shift depending on changes in the environment. Centura Wealth Advisory acknowledges that a key element of financial liberation is to monitor and pivot your original plans.

Insurance policies can be broken up into categories depending on your lifestyle. General liability insurance or personal liability insurance are a couple of examples that are worth reviewing.

General liability insurance covers your business when costly claims arise during normal business operations. It can help cover your business in the case that your business caused:

Third-party bodily harm

Third-party property damage

Reputational harm

Advertising injury

General liability insurance, however, does not cover your business for work-related injuries or illnesses sustained by employees. It also does not cover damage to your own business property or mistakes made in your business’s professional services.

Meet with a Tax Advisor

Meeting with a tax advisor can save you time, money and the stress of worrying that you might have made a mistake.

At Centura Wealth Advisory, we are dedicated as fiduciaries to our clients’ stewardship of their assets.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1208782670.jpg14152119Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2021-08-14 18:02:002025-04-08 16:16:36Get Ahead of The Curve: Year-End Financial Planning

“I’ll start financially planning next month” is a phrase that’s muttered too often.

At Centura Wealth, there are five steps that make clear how financial planning is key to liberating your wealth.

Knowledge

Knowledge is power, and this rings true especially with financial planning. For some, financial jargon is reason enough to avoid financial planning. The fancy words, however, still fail to cover the truth about financial planning. Wealth has many complexities and responsibilities, but a big part of the burden is simply doing right by your family and your values. In short, grow your knowledge.

Time Management

Life is stressful, and some factors are out of your control. But, if you start financially planning, one element can be in control. Time management plays a major role in creating balanced financial planning.

Statistics show time management is wildly out of control for the general population. Some of these include:

“If you spend 10-12 minutes planning your day, you’ll save up to two hours of time that would have otherwise gone to waste

The average person has tried and/or uses 13 different methods for managing their time

American companies lose roughly $65 billion because their employees are suffering from a lack of sleep”

Time management and financial planning go hand-in-hand. If you can manage your finances, you can manage your time better and prioritize what matters most.

Future Goals

The future matters. If you start financial planning now, however, you’ll be set up for success on all levels of your financial wealth plan. This includes savings, retirement planning, charitable giving, and overall security.

Goals are hard to attain if the planning isn’t present. There is never a better time than now to start financial planning. Feeling overwhelmed with the idea of financial planning? That’s why Centura Wealth Advisory is here.

At Centura Wealth, our approach is to understand your wealth, identify inefficiencies, design new pathways, then liberate and steward your wealth. We achieve this through our unique and comprehensive process: Uncover, Unlock, Design, Liberate, and Steward.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-959028830-scaled.jpg17082560Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2021-07-03 18:15:002025-04-08 16:16:35Why Financial Planning is Important Now

With a swoop of a pen, could thousands of households suddenly face an Estate Tax? If so, is there anything that can be done about it? Why would someone now face this wealth tax when they haven’t before? How does this relate to the current political election?

In this blog post we explore these ideas, and more. Consider the following:

The upcoming presidential election has the potential to radically change tax laws that govern Estate Planning

Democrats are targeting a repeal of the Tax Cuts and Jobs Act and have proposed lowering the estate tax exemption from its all time current high of $11.58MM today if they win the White House and senate1

The possibility of repealing and changing current tax law has created a frenzy of estate planning activity as many more families might face the Estate Tax in coming years

This post discusses a brief history of the estate tax and how it works, explores the current exemption level and highlights potential implications associated with the upcoming election. For a more in depth conversation on your plan, contact Centura Wealth Advisory.

What is the Estate Tax

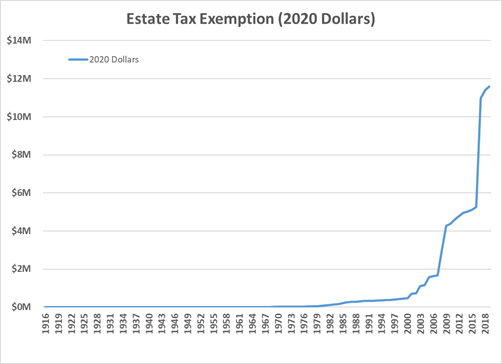

The Estate Tax is a tax on your right to transfer property at your death. Currently, there are very few taxpayers that encounter the Estate Tax and that is because the current exemption level is at an all-time high (see Estate Tax Exemption chart below). A high exemption level ensures that only the wealthiest pay this tax, however a lower exemption level would expose many more American families; and that is the concern as it relates to the upcoming election. To understand the estate tax and how it is used by the federal government, it is important to begin with a historical perspective.

History of the Estate Tax: Prior to 1916

In the United States, the death tax has been used several times to generate revenue in times of war or crisis. In each instance, congress used the death tax as a short term tool to raise funds during times of need and repealed the tax when the need was no longer there. The first example of this was during The Stamp Tax of 1797 when the tax was used to create revenue for an undeclared war with France. The second iteration came with the Revenue Act of 1862, which was used to raise money for troops, ammunitions, and other expenditures during the American Civil War. And finally, when the Federal Legacy tax was created during the Spanish-American War. All these enactments of the death tax were repealed shortly after the wars ended. However, the death tax was once again reintroduced in 1916 during World War I, setting the stage for the Modern Estate Tax.2

History of the Estate Tax: 1916 to present

The Revenue Act of 1916 created the Modern Estate Tax which was a tax on the transfer of wealth from an estate to its beneficiaries. The key caveat here is that this tax was levied on the estate as opposed to an inheritance tax that is levied directly on beneficiaries.

Since inception, the Modern Estate Tax has been amended at least twenty times for various reasons such as, the increase to a $120,000 exemption level at an 18% rate in 1926, and more recently in 2018 when it was amended to an $11.18mm exemption level at a 40% rate due to the Tax Cuts and Jobs Act. Chart 1 shows the Estate Tax Exemption since 1916, adjusted for inflation. As is clear from the chart, the current level of the estate tax exemption (adjusted for inflation) is at an all time high.2

Chart 1– Estate Tax Exemption Over Time (inflation adjusted)

How does the Estate Tax work

There are 2 primary aspects to the Estate Tax: the Exemption Level and the Tax Rate.

Exemption Level – The estate tax exemption level is the threshold at which an estate is subject to estate tax

Tax Rate – The estate tax rate is applied to the amount of the estate above the estate tax exemption level

Through manipulation of the exemption level and/or rate, congress can creatively target revenue (in the form of tax dollars) that would otherwise not exist if the current law of the land were to prevail (i.e., Tax Cuts & Jobs Act).1

What could it mean for me and my family?

Estate tax form

We know that decreases in the exemption level and/or increases in the rate are tools that can be used to target more money from more estates, but at Centura we are increasingly concerned about this wealth transfer risk due to 2 primary factors:

Government Debt: An urgency to raise funds to pay off debt associated with the COVID-19 pandemic as current government debt is at $27 Trillion.3

Revenue Collection Deficit: The current estate tax only affects a small fraction of estates (due to the high exemption level) and raises less than 1% of federal revenue.4

With the U.S presidential election less than 30 days away, the Estate tax has been the subject of significant interest among policy makers, researchers, and the general public. Reasons for this interest range from views on the fairness of the tax to interest in the effects of taxing transfers at death on the overall U.S. economy. No matter what the reason is for reformation, we know that this tax rate is volatile and significant to those affected by it.

Scenario Analysis

A great way to illustrate the potential impact of a revised estate tax is to consider one specific estate, and analyze the tax implications under two different death scenarios. These scenarios differ by the year of death (2021 vs 2026), which has an impact on the estate value, exemption level and potential tax liability. Thus, these are for illustrative purposes and are meant to help the reader contextualize the implications of these political decisions. The four scenarios analyzed are:

Scenario 1: (Baseline) Estate value of $5.0M in 2021 (at death)

Scenario 2: Democratic Proposal Retroactive to 01/01/2021

Scenario 3: $5.0M (2021) Estate in 2026 (Sunset Provision, TCJA)

Scenario 4: $5.0M (2021) Estate in 2026 with Democratic Proposal 01/01/2021

Table 1– Scenario Analysis

Illustration of Tax Risk

Scenario 1 in Table 1 represents the estate tax due under the current law (Tax Cuts & Jobs Act) and Scenario 2 shows the estate tax due under the proposed democratic policy. Both Scenarios 1 & 2 depict a 2021 date of death scenario since the democratic policy would likely be retroactive to 01/01/2021.

Alternately, for Scenarios 3 & 4 we selected the year of death as 2026 which is when the exemption level is scheduled to sunset, based on current law (Tax Cuts & Jobs Act).5

As is clear from this example, a change in estate tax policy to the democratic proposal could have huge tax ramifications. In addition, these taxes may extend to many more families than they otherwise would at higher exemption levels. Thus, the upcoming election should be of keen interest to families with estates of $3 Million or more.

What can you do?

At Centura, we assist individuals and families with navigating the complicated world of estate planning, specializing in strategies designed to help you efficiently transfer wealth to your loved ones and causes you care about. To help you get started we put together a calculator to help you estimate what your estate tax liability could be.

Depending upon the outcome of the 2020 election, we believe many more estates may be exposed to this long standing tax and we can help in planning to address it. Please contact us to learn more or take advantage of our free calculator.

https://centurawealth.com/wp-content/uploads/2024/08/AdobeStock_241616506-Resized-scaled.jpeg12582560Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2020-10-19 18:18:002025-04-08 16:16:35A Brief History of the Estate Tax and Potential Implications for the Upcoming Election

Opportunity Zones (O-Zones) are a unique product of the 2017 Tax Cuts and Jobs Act (TCJA). Since being introduced, opportunity zone investments (OZs) have been a hot topic for potential tax planning. So much so, it’s been reported that Qualified Opportunity Funds have raised over $6.7 billion thru December 2019, a number that grew at a rapid pace at the end of 2019 as taxpayers looked for ways to defer capital gains.

When it comes to O-Zone, tax breaks are the headliner, but the actual underlying investment within the Opportunity Zone shouldn’t be overlooked. Questions investors should ask include:

Where am I investing my money?

Are there enough good investment opportunities in this space?

Will the tax benefits be significant enough to outweigh an under-performing investment?

Would the investor be better off just paying the tax and re-investing in an investment of their choosing?

In this blog post, we’re going to dive into Opportunity Zones, which can be a hybrid tax planning and investment solution for those that have recognized a large capital gain. We’ll define the basics of the Opportunity Zones, discuss the tax benefits, compare O-Zones to other types of investments, and explore the characteristics of an investor that might consider an investment in a Qualified Opportunity Zone.

What is an Opportunity Zone?

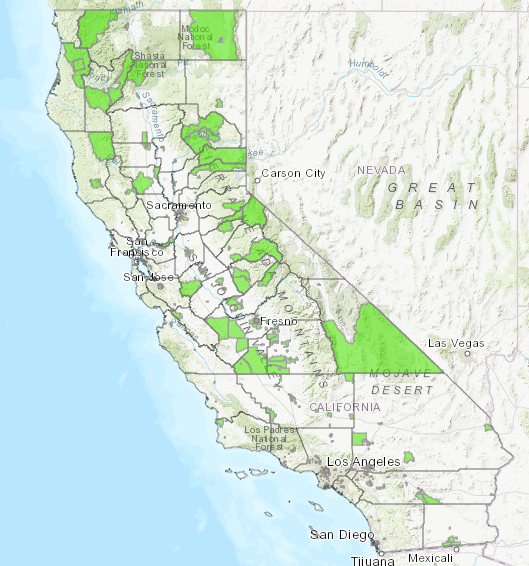

The Tax Cuts and Jobs Act of 2017 brought about a new type of investment offering, Opportunity Zones, which provide a unique way of mitigating capital gains tax. The Opportunity Zones were created to incentivize investment of capital gains into low income or economically distressed communities. By investing in these communities, taxpayers may be allowed to defer capital gains when investing funds into a Qualified Opportunity Fund (QOF) and meeting other requirements.

Check out the California Opportunity Zone map here.

What is a Qualified Opportunity Fund (QOF)?

A Qualified Opportunity Fund is an investment vehicle that files either a partnership (Form 1065) or corporation (Form 1120/1120S) federal income tax return and is organized for the purpose of investing in Qualified Opportunity Zone property.

What are the tax benefits of investing in a QOF?

There are three main categories for the tax benefits:

Deferral of a Capital Gain

Step-up in Basis of the deferred gain amount

Tax free gain on new Qualified Opportunity Fund growth

Deferral of Capital Gain

When a capital gain is recognized on the sale of an asset, you have the option to take any part of the capital gain and re-invest the proceeds into a Qualified Opportunity Fund (QOF). If the capital gain proceeds are re-invested into a QOF within 180 days of the gain being recognized, the dollar amount invested will be eligible for deferring the capital gain until the earlier of:

The tax year when the QOF interest is sold

Or December 31, 2026

At that time, the capital gain amount that was initially deferred when proceeds were invested into the QOF, would be recognized (less any step up in basis, see below) and taxes will be paid. The capital gain tax rate will be based on the tax rate applicable during the year the gain is eventually recognized.

Step-Up in Basis

If the investment in the QOF is held for at least 5 years, there is a 10% step-up in the basis of the deferred capital gain. If the QOF investment is held for 7 years, there is an additional 5% step-up in basis of the deferred capital gain (for a total of 15%). For those investing in 2020 and beyond, there will not be a 5% step up since it will be impossible to reach the 7-year holding period by 2026.

Tax free growth

If the interest in a QOF is held for 10 years or more, the post-acquisition gains in the QOF will be excluded on the sale of the QOF interest, thereby completely avoiding capital gains tax on this portion of the gain. There are several tax incentives that could be a big win for the long-term investor. However, taxes alone should never drive an investment decision, so let’s review a few of the primary risks associated with investing in a Qualified Opportunity Fund.

Risks Abound

The TCJA just put Opportunity Zones on the map in 2017, and as recent as December of 2019, the IRS published its final regulations on Opportunity Zones. The Qualified Opportunity Funds are new vehicles and due diligence is paramount. Investors will be facing questions of operator risk, investment risk, and illiquidity risk to name a few.

Operator risk– There won’t be an extended track record for any of the funds or operators. Are they putting the money to work in good opportunities that will net investors a positive return? Are they operating in compliance to meet the requirements of a Qualified Opportunity Fund?

Investment risk– While the Opportunity Zone rules do encourage more than just real estate development, it is likely that a lot of early projects will be in real estate development. Any real estate development project carries its own risks, not to mention that the developments will be located in Opportunity Zones, which by design are designated as an economically distressed area. As such, investing in these areas could carry additional risk(s) and expectation of returns should be scrutinized closely. Depending on the QOF, there could be single property risk if the fund has only invested in one project versus others that plan to invest in multiple projects.

Illiquidity – depending on the fund, the investment could be illiquid. To capture the tax benefits and defer the gain the maximum number of years, you would need liquidity elsewhere. This will be a 10-year investment if you want to hit the tax trifecta (deferred gains, step-up in basis, and future tax-free growth). If holding the QOF investment for ten years, the investor would also need to set aside cash to pay the initial capital gain tax that was deferred and recognized in 2026, so plan accordingly.

Is an Opportunity Zone Investment Worth Consideration?

For comparison, we ran a hypothetical scenario to help evaluate the break-even return required by an investor that has captured a tax benefit from the Opportunity Zone (OZ) investment:

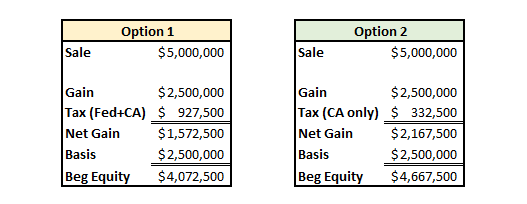

Option 1: Recognize capital gains on an investment, pay tax on those gains for Federal and California (assuming a California tax payer), and reinvest all the net proceeds (gain and basis) into a new investment

Option 2: Recognize capital gains on an investment, pay tax on those gains for California only, and reinvest the net gains in a Qualified Opportunity Fund while putting the basis in a new investment

It’s clear the Opportunity Zone investor has the beginning advantage with more capital to invest in year 1 (Option 2). A larger starting investment can compound at lower rates of return and still arrive at the same future dollar amount over 10 years. But, how much lower can the return be for the tax advantaged investor before the lackluster investment performance wipes out the tax advantages?

The goal here was to find the break-even return required from an Opportunity Zone fund to put the investor on par with just paying the tax and re-investing.

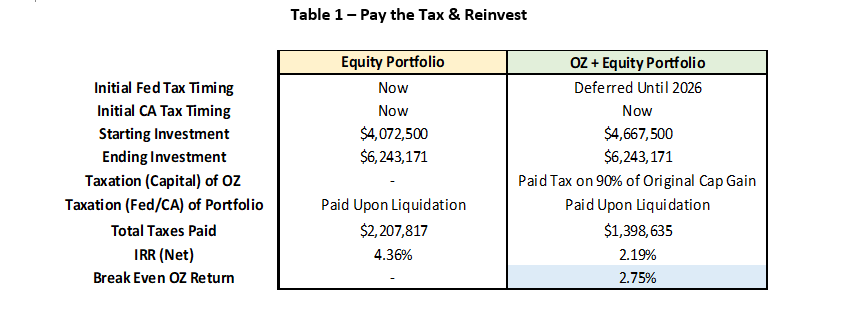

For the first scenario (Table 1), we assumed the investor paid the tax and re-invested the remaining proceeds into an equity portfolio with an expected return of 6.33% (see Capital Market Assumptions Blog). The Opportunity Zone investor invested the gain portion into a QOF and the basis in an equity portfolio. Assumptions are that all investments are liquidated at the end of ten years. The numbers are as follows:

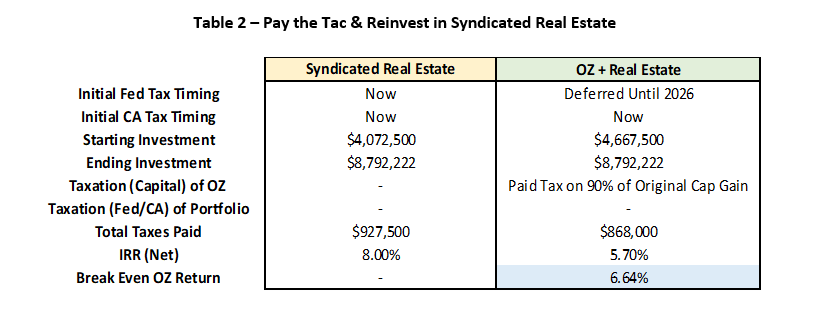

For the second scenario (Table 2), we assumed the investor paid the tax and re-invested the net proceeds into syndicated real estate that is expected to return 8%. The real estate investment has additional tax deferral options at the end of the ten-year holding period. It is still assumed that both options are liquidated at the end of ten years. The breakdown comparison of the options are shown below:

The QOF has merit when compared to paying the taxes and investing in an all equity portfolio. The break-even return required in the QOF of 2.75% (see Table 1) gives the investor a nice cushion provided by the tax savings. However, for accredited investors with the options to place funds within more sophisticated investment vehicles, the results become more convoluted. The QOF investor would require a break-even rate of return at 6.64% which is a much higher hurdle for an Opportunity Zone investment that carries many additional risks outlined earlier.

Conclusion

Let’s summarize where the Opportunity Zone seems to be an optimal solution.

At minimum, it’s an investor that has recognized or will be recognizing a significant capital gain. If the investor:

Has liquidity elsewhere to allow for a 10-year investment horizon in a QOF and liquid assets to pay the deferred tax due in year 2026

Would like to diversify a portion of their portfolio to real estate

Desires to invest money within economically disadvantaged areas for community/social benefits

Based on the comparison we modeled, if the motivation is strictly financial, an accredited investor in California (zero state tax benefits) with access to private syndicated real estate investment opportunities might just consider paying the tax and investing in a lower risk real estate investment. Instead of investing money in projects requiring development, existing properties with current cash flows may be a lower risk option.

Of the tax incentives, the ‘tax free’ growth on a new investment in an Opportunity Zone sounds appealing. However, real estate investments already allow for significant tax efficiency. Real estate investors can defer unrealized gains in future 1031 (IRC Section 1031) exchanges and heirs of real estate property receive a step up in cost basis at death.

In addition, certain types of real estate investments also allow investors to utilize depreciation to shield income from taxation; until exhausted or exchanged into a new property via 1031 exchange.

Given the existing tax efficiency and opportunity to invest outside of economically disadvantaged areas, private syndicated real estate has the potential to outperform a higher risk Opportunity Zone investment in the long run.

If you’ve incurred or will be incurring a significant capital gain and need help evaluating your options, contact Centura Wealth Advisory for a consultation.

Centura Wealth Advisory (“Centura”) is an SEC registered investment adviser located in San Diego, California. This brochure is limited to the dissemination of general information pertaining to Centura’s investment advisory services. Investing involves risk, including risk of loss.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/AdobeStock_75443283-scaled.jpeg14492560Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2020-02-07 17:36:002025-04-08 16:16:35O-Zones (Opportunity Zones): Is the Juice Worth the Squeeze?

Two retirement reform bills (the SECURE Act and RESA) have been circling around Washington, and if passed, may make significant changes to many retirement and estate plans. Notably, the proposed changes outlined in the bill(s) have meaningful implications as the rules on inherited IRA’s are up for debate. Both the House and Senate have different views on the technical aspects of how tax shelters for inherited wealth could be reduced. Read our blog to learn about the differences in proposed changes for “Stretch IRA’s” and what they could mean for tax planning, wealth accumulation and wealth transfer.

Introduction

Retirement savings and tax laws are inextricably linked. For example, IRA’s, 401(k)’s and other tax deferred retirement vehicles have been designed to assist savers in meeting their future income needs so that Social Security is not the sole source of retirement income. While lawmakers have created different ways to save (e.g., traditional IRA vs Roth IRA), the RMD (required minimum distribution) types of accounts that have currently garnered attention from lawmakers are “stretch” IRA’s. This post will examine new bill(s) from both the US House of Representatives and US Senate, as they pertain to stretch IRA’s, evaluating the potential implications from a financial planning perspective (especially taxes).

What is a Stretch IRA?

A stretch IRA is an estate planning strategy that extends the tax-deferred status of an inherited IRA when it is passed to a non-spouse beneficiary. This approach allows for continued tax-deferred growth of an individual retirement account (IRA) and sets limits to the amount that must be withdrawn each year. The goal of this type of strategy is to limit the required distributions on an inherited IRA, stretching them over time, in order to avoid a large tax bill.

The IRS blesses this approach through Required Minimum Distribution (RMD) factors (based on age), which guide how much of an IRA must be withdrawn each year (at a minimum). The RMD amount withdrawn is taxable and therefore represents revenue to the United States government. Thus, while investors seek to extend the period of withdrawal to be as long as possible, lawmakers looking to accelerate tax revenues have honed in on stretch IRA’s.

Proposed Legislation

On March 29, 2019 the House Ways and Means Committee presented HR 1994, also known as the SECURE Act, which eventually passed on May 23, 2019 and is currently awaiting senate approval. SECURE is an acronym for Setting Every Community Up for Retirement Enhancement and represents a bipartisan bill. In the House bill, inherited IRA’s would need to be withdrawn within a 10-year period. Depending upon taxpayer preference, this could be periodically, at regular intervals, or even ballooned on the back end. Taxes will be paid on the distribution(s) when taken and after 10 years the entire IRA balance must be depleted.

Following suit, on April 1, 2019 the Senate introduced a bipartisan bill known as RESA; Retirement Enhancement and Savings Act. The Senate version allows a “stretch” on the first $400,000 of aggregated IRA’s and the exceeding balance must be distributed within 5 years. Taxes would be paid on the distribution(s) when taken.

Both proposed bills cover a wide range of retirement issues, and allow exceptions for distributions to minor children, disabled or chronically ill beneficiaries, or beneficiaries who are not more than 10 years younger than the deceased IRA owner. Both versions would apply to inherited IRA’s for deaths occurring after December 31, 2019 and are applicable to Roth IRA’s as well as traditional IRA’s and Qualified Plans.

Potential Impact

To illustrate the potential impact of this legislation, we will model three scenarios to garner insight into how they compare and what they might mean for a beneficiary. The three scenarios we will model include:

Current Law for stretch-IRA’s

House Bill HR 1994 for stretch-IRA’s

Senate Bill RESA for stretch-IRA’s

The assumptions we use for all three scenarios include a 50-year-old beneficiary with a 30% effective tax rate (federal & state), inheriting a $1,000,000 traditional IRA. For simplicity, we use a flat effective tax rate of 30% to illustrate the effects of legislation on taxation and assume a linear withdrawal rate on non-stretch assets; however, we note that in reality “bracket creep” is likely to occur, absent tax planning.

Bracket creep means that incremental income (e.g., RMD’s) moves you into higher tax brackets and increases the overall taxes that you pay. This would mean that effective tax rates are likely to be higher than 30% when RMD’s are accelerated (ceteris paribus), exacerbating the punitive effect of taxes and increasing the value of tax planning.

Thus, for individuals at or near retirement (and/or in high tax brackets) accelerated RMD’s as proposed by the House and Senate could have detrimental effects on wealth retention, and tax planning strategies should be considered.

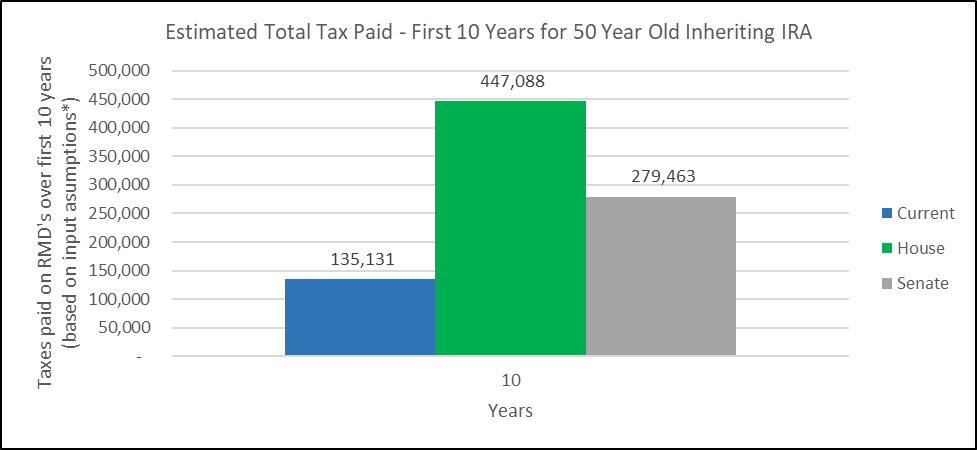

Ignoring the supplemental effects of “bracket creep,” we find that a $1,000,000 portfolio that earns an annualized 8% pays the following taxes over 10 years:

Chart 1 – Estimated Total Tax Paid: Hypothetical Example

Evaluating the results shown above, we find that under the current law a 50-year-old, at a 30% effective tax rate, would pay $135,131 in total taxes over a 10-year period. This compares to $447,088 in total taxes paid over 10 years under the House Bill (HR 1994) and $279,463 under the Senate Bill (RESA). Intuitively these results make sense as the House Bill is asking beneficiaries to deplete entire account balances over 10 years, whereas the Senate Bill only asks that a portion (in this example 60%) is accelerated over 5 years. See summary results in Table 1.

These proposed legislative changes have huge financial planning implications as increased tax burdens are never welcome. At Centura, we specialize in tax and estate planning, designing plans for 10, 20, 30+ year periods so these changes create new opportunities and strategies for us to discuss (and potentially use) with clients.

For example, under these proposals Roth conversions become increasingly valuable as does charitable giving; pairing the two together in the right way can liberate wealth transfer, decrease taxes and fulfill philanthropic goals for your estate. Additionally, permanent life insurance will be more valuable as it can be used to pass death benefits tax free to heirs, mitigating the negative impact of taxation on their inherited assets.

Challenges beget opportunities and we believe this legislation has the potential to make sweeping changes to many estate plans. As such, we are closely following this legislation and diligently working to be ahead of the curve with strategies and solutions to deploy. We encourage clients (and advisors) to follow this proposed legislation, and if passed, contact us to discuss the ramifications and appropriate solutions.

Disclosures

Centura Wealth Advisory (“Centura”) is an SEC registered investment adviser located in San Diego, California. This brochure is limited to the dissemination of general information pertaining to Centura’s investment advisory services. Investing involves risk, including risk of loss.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/AdobeStock_164050571-scaled.jpeg17072560Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2019-08-16 17:24:002025-04-08 16:16:35Stretch IRA – What Proposed Legislation Could Do to Your Wealth Transfer Plans

The current low interest rate environment affords savvy financial planners certain tax planning strategies that leverage charitable giving. These strategies utilize charitable contribution limits, as a percentage of Adjusted Gross Income (AGI), to plan for and mitigate taxes the current year and up to the next five following years. This article explores the new 60% deduction introduced by Tax Cuts and Job Act (TCJA)5 and highlights the following:

Charitable giving in the United States is alive and well

Tax Cuts and Jobs Act provides added incentive for taxpayers to give to charity: a 60% deduction

Type of gift and recipient organization determine the AGI deductibility percentage

Rules for determining deductibility are complex and change over time

Only cash gifts to public charities qualify for new 60% deduction

50% limit will still apply on cash gifts to private foundations and gifts including non-cash items

Introduction

Charitable contributions allow taxpayers to deduct gifts of money or property made during the taxable year to nonprofit organizations1. It is generally accepted that these organizations improve society and are afforded the ability to avoid taxation as a result. This avoidance of taxation serves as an incentive mechanism to shift public good to the private sector by encouraging private giving and if done correctly, can help reduce the incentive for politicians to raise taxes in the name of public good.

As such, charitable giving is an integral part of tax and estate planning in the United States. Consider the following statistics from 20172:

Americans gave $410.02 billion in 2017 (5.2% increase from 2016)

70% of total giving came from individuals, 16% from foundations, 9% bequests and 5% from corporations

Charitable giving accounted for 2.1% of gross domestic product in 2017

High net worth donors gave on average $29,269 to charity vs $2,514 for the general population

Based on these numbers, charitable giving is alive and well, with high net worth individuals leading the charge. However, many rules affecting tax incentives have changed with introduction of the TCJA including one notable change to charitable giving thresholds; a 60% AGI limitation.

Charitable Giving Thresholds: Spirit & Letter of the Law

Charitable contribution deductions are outlined under Section 170 of the Internal Revenue Code (IRC) and IRC Section 170 has been through countless changes since being enacted in 19173. The spirit of the law has been to allow “wealthy” taxpayers to receive a deduction for charitable giving, but the letter of the law has evolved into a complex set of rules. These rules are designed to maintain an equitable statutory scheme that encourages charitable giving but prevents tax abuse and are therefore purposefully complex3.

Charitable Giving Thresholds: Tax Cut & Jobs Act 2017

When taxpayers make charitable donations, they may utilize those donations as deductions against AGI, to reduce taxable income6. The caveat being that the amount of charitable deduction which could be recognized in any one year was limited to a certain percentage of AGI (e.g., 20%, 30%, 50%) based on the type(s) of assets contributed and the type of organization receiving the benefit. The top AGI percentage limitation was 50% until in 2017, the TCJA introduced a new figure, 60%. But what does it mean and when is it applicable?

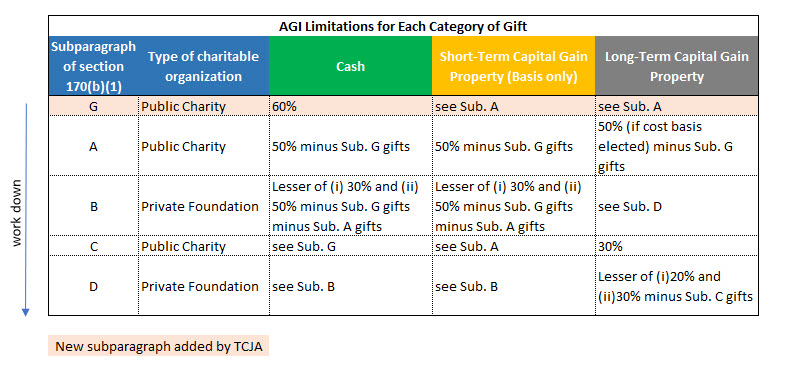

Types of Gifts4

To understand when the 60% limit is applicable, it is necessary to understand how the IRC classifies gifts as not all gifts are created equal. Per section 170(b)(1) of the IRC, there are 5 distinct types:

Subparagraph G Gifts

Subparagraph A Gifts

Subparagraph B Gifts

Subparagraph C Gifts

Subparagraph D Gifts

Subparagraph G Gifts

This is where the calculation now begins, and this is the newest section added by the TCJA. Under a new temporary rule enacted under the TCJA, for tax years after 2018-2025, an individual donor may deduct up to 60% of the donor’s contribution base for gifts of cash (and only cash) to a public charity. To qualify, these gifts must be “to” the public charity, not “for the use of”.

Subparagraph A Gifts

These include all gifts “to” (not “for the use of”) a public charity and taxpayers may deduct up to 50% of contribution base, reduced by amount of any subparagraph G deduction allowed, for subparagraph A gifts.

Subparagraph B Gifts

Gifts of cash or short-term capital gain property to a private foundation, and for gifts that are “for the use of” rather than “to” a public charity. Taxpayers may deduct up to the lesser of:

30% of contribution base – or –

Excess of 50% (not 60%) of the donor’s contribution base for the year reduced by the combined amount of subparagraph G gifts and subparagraph A gifts.

Subparagraph C Gifts

This subparagraph operates as a limitation on deductibility of subparagraph A gifts involving long-term capital gain property and sets forth that except for gifts of conservation easements, an individual may deduct up to 30% of contribution base for gifts of long-term capital gain property to a public charity.

Subparagraph D Gifts

Include gifts of long-term capital gain property to a private foundation of which taxpayers may deduct the lesser of:

20% of contribution base – and –

Excess of 30% of contribution base for the year over the amount of subparagraph C gifts

For all types of gifts, excess contributions can be carried forward for up to 5 tax years but may only be used within the same category (i.e., AGI % limitation) in those future years.

Exhibit 1 shows the AGI limitations as percentages of contribution base for each category of gift.

Exhibit 1- AGI Limitations4

The primary takeaway is that the new 60% limitation is only applicable on cash contributions to public charities; period. This means that the 60% limit will be reduced to 50% on cash donations when the taxpayer also donates any non-cash property to any type of charity, whether public or private, or when the taxpayer donates cash to a private foundation.

Conclusion

A donor must rely solely on cash gifts to public charities in order to reach the higher 60% limitation afforded by subparagraph G. While the new 60% limitation may grab headlines, it is limited in its applicability and caution must be paid for donors looking to utilize the 60% limitation in their planning. For example, charitable contribution deductions from prior years, as well as other forms of giving (e.g., household goods, clothing, stocks, bonds, etc.) could void qualification for the 60% limit on cash donations to public charities and reduce it to 50% instead. These rules and limitations are incredibly complex, and ever changing, which means that working with knowledgeable tax professionals is of paramount importance.

At Centura Wealth Advisory, we utilize charitable giving strategies in tax and estate planning, which requires us to be up to date on current tax law and on the cutting edge of tax planning innovation. As a result, we work with select tax, legal and financial planning professionals who keep us armed with intricate knowledge of strategies, related sections of IRC code and applicable case law. In addition, these professionals allow us to seamlessly implement, manage, and if necessary, defend such strategies. We believe that this coordinated approach to advanced tax planning is what sets us apart.

Finally, today’s low interest rate environment affords many charitable planning opportunities that many advisors and donors have never even considered. If you are interested in utilizing charitable contributions to mitigate income taxes for you or your clients, contact us today for a tax planning evaluation.

Centura Wealth Advisory (“Centura”) is an SEC registered investment adviser located in San Diego, California. This brochure is limited to the dissemination of general information pertaining to Centura’s investment advisory services. Investing involves risk, including risk of loss.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/AdobeStock_178187166-scaled.jpeg8532560Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2019-07-09 16:52:002025-04-08 16:33:31Charitable Giving: Breaking Down the 60% Deduction