Life insurance is an important consideration when it comes to securing your family’s financial future. In the event of your death, life insurance policies can provide financial protection to your loved ones, ensuring that they are taken care of in your absence. However, not all life insurance policies are created equal. For high net worth individuals, a private placement life insurance (PPLI) policy can offer unique advantages over traditional life insurance policies.

In this article, we’ll explore the differences between PPLI and traditional life insurance, and explain why PPLI may be the better choice for high net worth individuals & families.

Traditional Life Insurance

Traditional life insurance policies operate in a relatively simple manner. Policyholders pay a premium in exchange for a death benefit that is paid out to their beneficiaries when the insured dies. After premiums are paid, insurance charges are deducted and the net premium is invested in some sort of mechanism, dictated by the policy type. In the case of traditional variable universal life (VUL), this net premium is allocated to the carrier’s “segregated” account that is separate from the general account (thus not subject to the carrier’s creditors).

Limited Investment Pool

One of the main drawbacks of traditional VUL policies is that they limit investment choice to a pre-selected pool of options. Similar to the investment selection of a 401k menu, there are typically anywhere between 75-150 funds to choose from. Also, these funds do not include alternative style investments, thus limiting the potential growth of the cash value. As a result, traditional life insurance policies may not be an ideal option for qualified purchasers and/or accredited investors who are seeking to grow their wealth tax-efficiently and with more significant returns.

Accessibility

It’s essential to note that traditional life insurance policies are generally more accessible than PPLI policies, as they do not require nearly as significant investment upfront. However, traditional life insurance policies do not offer the same level of flexibility and customization over investment selection as PPLI policies.

PPLI (Private Placement Life Insurance)

Private placement life insurance (PPLI) policies operate in a similar manner to traditional life insurance policies. However, PPLI policies are specifically designed for serving as a tax efficient wrapper for tax inefficient assets.. Also, with a PPLI policy, the policyholder can invest in a separately managed account (SMA), which can be customized relative to the fixed menu of “off the shelf” offerings on the carrier’s platform. These SMAs can hold a range of investment types, including hedge funds, private equity, private credit and real estate to name a few.

Tax Efficiency

One of the most significant benefits of cash value life insurance policies is tax efficiency. PPLI policies allow policyholders to defer taxes on their investment gains and income while the policy is active. Additionally, PPLI policies can provide tax favored access to policy distributions, either by withdrawing up to cost basis tax free or utilizing tax free policy loans. The death benefit is also received tax free by the policy holder’s heirs.

Asset Protection and Estate Planning Benefits

PPLI policies can also offer asset protection and estate planning benefits. PPLI policies are typically structured to provide a level of asset protection, shielding investments from creditors and lawsuits. Additionally, PPLI policies can be designed to reduce estate taxes, providing a tax-efficient way to transfer wealth to the next generation.

PPLI vs. Traditional Life Insurance

When comparing PPLI and traditional life insurance policies, the key differences lie the investment flexibility, costs and liquidity. Since life insurance policies grow tax deferred, they trade off investment tax drag for insurance costs. Assuming the policies are designed properly, these insurance charges for the death protection are minimized and this can be a very favorable trade-off. PPLI amplifies this trade-off versus traditional coverage in two ways:

PPLI tends to have much lower upfront fees relative to traditional coverage

PPLI allows the underlying investments to be comprised of assets with higher return potential but that would normally come with higher tax drag. PPLI eliminates the tax drag while keeping the higher return potential

PPLI vs. Traditional Life Insurance: Which Is Right for You?

For high net worth individuals who seek to grow their wealth and manage their investments in a tax efficient manner with greater flexibility, PPLI policies may be the better option. However, PPLI policies require a significant investment upfront and may not be accessible to everyone.

If the goal is to minimize premiums paid for maximum death benefit coverage traditional life insurance policies can serve as a very effective tool for estate liquidity and generational wealth leverage for your loved ones. However, if you’re a high net worth individual looking to grow your wealth tax-efficiently, protect your assets, and provide ancillary estate planning benefits, a PPLI policy may be the better choice for you. By working with a knowledgeable wealth advisor, you can explore your options and make an informed decision that meets your unique financial goals and needs.

If you’re interested in learning more about PPLI and how it can help you achieve your financial goals, contact Centura Wealth Advisory today. Our experienced advisors can help you create a customized wealth management strategy that meets your needs and provides the protection and growth you deserve.

Connect With Centura

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients with fully transparent reporting and tools to make informed decisions around their wealth plan.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1188909800.jpg14142119Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2023-07-01 18:51:002024-08-19 18:53:20PPLI vs. Traditional Life Insurance: What’s the Difference?

San Diego, CA – Centura is proud to announce that Derek Myron, the company’s Managing Director, was featured in the recent wealth management roundtable organized by the San Diego Business Journal (SDBJ).

The roundtable discussion brought together eight of the region’s leading financial planners and wealth managers to share their expertise and advice on retirement planning and estate planning management.

Derek Myron’s Experience and Commitment to Helping Others:

With over 25 years of experience, Derek Myron has been serving high net-worth individuals and families since 1998, assisting them in the creation and implementation of carefully crafted plans to achieve both their financial and life goals. His dedication to helping others reach their highest potential, both professionally and personally, has been his guiding principle throughout his career.

Strong Foundation and Qualifications:

Growing up in a two-parent-teacher household that emphasized academic excellence and community service, Derek developed a strong foundation of values centered around education and helping others. He earned his undergraduate degree in Business Administration with a Finance concentration from the University of Washington and has held the Certified Financial Planner (CFP(R)) designation since 2001.

Passionate about Liberated Wealth® Plans:

Passionate about making a positive impact on his clients’ lives, Derek finds great joy in developing and implementing Liberated Wealth® plans for Centura Wealth Advsiory’s clientele. By facilitating an impactful change to their financial well-being, he helps them achieve their life goals with a focus on long-term prosperity.

The Great Retirement: Insights From Wealth Management Expert, Derek Myron

The latest issue of the San Diego Business Journal magazine’s Wealth Management section explores the challenges faced by Baby Boomers, the generation born between 1946 and 1964, who currently represent 28% of the U.S. population. With retirement rates rapidly accelerating, approximately 75 million Baby Boomers are expected to retire by 2030, marking a significant shift in the demographic landscape.

Top Concerns for Retirement Planning

As Baby Boomers approach or enter retirement, ensuring financial stability throughout their golden years becomes a paramount concern. Factors such as longer life expectancy, rising healthcare costs, and market volatility contribute to the complexity of retirement decisions. Navigating the financial path during retirement presents challenges that require careful consideration and expertise.

The Largest Intergenerational Wealth Transfer in History

In addition to retirement planning, Baby Boomers face the task of transferring wealth to their children, marking the largest intergenerational transfer of wealth in history. However, despite the magnitude of this responsibility, a majority of U.S. households lack sufficient plans in place to effectively manage this transition. Many individuals overlook the opportunity to seek guidance from wealth managers and financial planners who possess the expertise to structure comprehensive plans that facilitate the growth and management of wealth.

Let’s review Derek’s insights.

What potential challenges can arise during the transfer of a family business, and what are the associated complexities? When passing on a business, what are the primary goals to consider: fairness or equality?

Derek Myron explains the complexities associated with passing on a family business: “A family business can be extremely complicated to pass on and continue running after the death of the primary owner. This often arises due to family dynamics, disproportionate involvement in the business, and various other factors… Should it be passed on to those involved, benefiting them more than others? Or should it be divided equally… The right solution depends on the facts, circumstances, and preferences of the business and family. Proper business succession planning is crucial…”

What are common issues/problems heirs may encounter that wealth managers can help with?

Derek Myron sheds light on the issues heirs may face and how wealth managers can assist: “A good estate plan allows heirs to inherit wealth with help and support in how to manage it… Certain assets can pose challenges for heirs… Having a competent, experienced, and qualified financial advisor will help assess whether your current estate plan aligns with your goals and make necessary modifications as needed. They can also assist in setting up business succession plans, facilitating the sale of directly managed real estate assets, and transitioning into syndicated deals where management is delegated… without proper planning, wealth can become burdensome.”

What actions can be taken to Mitigate Tax Exposure in a Trust/Estate Plan?

Derek Myron provides insight on actions that can be taken to mitigate tax exposure in a trust/estate plan. He explains: “At present, gift tax and estate tax exemptions are around $13 million per individual and around $26 million per married couple… the exemptions will sunset on Jan. 1, 2026, back down to the level pre TCJA; adjusted for inflation… anyone with assets expected to exceed these estate tax exemption levels in 2026… should consider the design and construction of their current wealth transfer plans.”

Centura’s Ranking in San Diego Business Journal’s List of Wealth Management Firms

Centura Wealth Advisory has secured the notable position of #22 on the San Diego Business Journal’s list of wealth management firms. SDBJ’s list was ranked by assets managed locally for fiscal year 2022.

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients with fully transparent reporting and tools to make informed decisions around their wealth plan.

Read on to learn more about our 5-Step Liberated Wealth Process and how Centura can help you liberate your wealth.

Disclosures

Centura Wealth Advisory does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither attorneys nor accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

SDBJ’s Wealth Management list was ranked by assets managed locally for fiscal year 2022. The ranking should not be viewed as representative of any one client’s experience and should not be taken as an indication of performance by Centura and any of its clients. SDBJ requested Centura to participate in the special report. Centura paid a fee to participate in the special report.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1432326796.jpg14242106Christian Duranhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngChristian Duran2023-06-16 18:41:002024-08-19 18:42:22Centura’s Managing Director, Derek Myron, Featured in San Diego Business Journal’s Wealth Management Roundtable

A PPLI policy can be a highly effective solution for both privately held business owners and high net worth individuals/families seeking tax efficient cash accumulation.

PPLI is an elegant type of variable life insurance contract that leverages the tax advantages of traditional coverage and provides access to a wider array of investment options. If structured properly, funds may be allocated across a highly customized pool of investments. Surplus premiums (premiums paid in excess of death benefit costs) are added to the policy cash value, growing tax deferred. PPLI can serve as an excellent strategy for mitigating ongoing income taxes, acting as a tax efficient wrapper for assets that:

Generate high levels of tax inefficient income, such as private credit or high-turnover hedge funds.

Are expected to significantly increase in value within the foreseeable future, and will ultimately be prepared for disposition.

Typical PPLI Candidate:

Net worth of $10 million or greater

Access to significant liquidity

Ability to fund $2-$5 million, cumulative within the first five years

Appetite for alternative style investments

Desire for sophisticated income tax & wealth transfer planning

Common Investments Inside PPLI Include:

High Turnover Hedge Funds

Private Credit

Direct Lending

Real Estate

Private Equity

Traditional Mutual Funds

Investment Customization Vehicles Include:

Off-the-Shelf Platform Funds (predetermined fixed menu of VITs & IDFs already available)

Institutional Pricing (typically < 100 bps per annum)

Trades investment tax drag for costs of insurance

No Surrender Charges

Favorable Policy Lending Terms

PPLI Discovery Process

The financial advisor and client collaborate to determine the client’s investment objectives, risk tolerance, as well as income tax & estate planning needs.

A risk/return analysis is conducted. The financial advisor works with the client to create a customized policy that meets their specific investment goals and tax planning needs. It includes review of cost to set-up and administer.

PPLI Policy in Action

Initial Set UpGrantors draft an irrevocable trust that will own a life insurance policy.

Contribution of FundsFunds are contributed to the trust, which are used by the trustee to purchase a PPLI policy.

InvestmentLiquid funds are allocated to various investment options within a separate account managed by an independent financial advisor.

Tax Favored Access to Policy ValueOver time, any investments acquired in the account grow tax-free. The policyholder can access funds tax-free by taking loans against the policy’s cash value. Upon policyholder’s death, the death benefit is paid out tax free to beneficiaries named in the policy.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1457585755.jpg13792173Christian Duranhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngChristian Duran2023-06-15 18:49:002024-08-19 18:51:45Private Placement Life Insurance (PPLI)

Private Placement Life Insurance (PPLI) is a financial tool that offers unique benefits for high net worth individuals. PPLI is a form of life insurance designed for accredited investors and qualified purchasers, providing a broad range of investment options with significant tax advantages.

In this article, we will explore the benefits of PPLI and compare it with traditional life insurance coverage.

What is PPLI?

In a nutshell, PPLI serves as a tax efficient wrapper for tax inefficient assets. It is essentially a tailored variable universal life insurance policy that is offered exclusively to accredited investors and qualified purchasers, allowing for a wider array of investment options that can include alternative style investments (i.e., such as private equity, private credit, hedge funds, etc..). These policies are treated as private offerings that when structured properly, can be highly customized to suit the policy holder’s needs & investment philosophy. PPLI is often designed as a highly tax efficient investment vehicle that provides tax-deferred growth on the policyholder’s underlying investments as well as tax favored distributions from the policy.

How Does PPLI Work?

The Mechanics of PPLI:

PPLI operates similarly to cash value universal life insurance contracts. It provides a death benefit to beneficiaries when the insured passes away. The policyholder pays an insurance premium, which, after deducting insurance fees, is allocated to an investment mechanism that generates a cash value component. The growth of this cash value depends on the net performance of the underlying investments and the deduction of ongoing insurance charges. If the investment performance exceeds the policy charges in a given year, the cash value increases. As long as the cash value remains above zero, the policy remains active.

Maximizing Premiums within IRS Limits:

In PPLI, policyholders often pay the maximum allowable premium relative to the death benefit set by the IRS. This approach minimizes the costs associated with insurance protection (death benefit). With proper asset management, the tax-deferred investment performance within the policy tends to outperform the costs of insurance over time. When comparing similar investment strategies outside of PPLI, policyholders make a trade-off. They trade the tax drag on investments outside the policy for the insurance fees within the policy. When structured correctly with suitable investments, this trade-off favors the “tax efficient” PPLI vehicle, with insurance charges minimized compared to outside investment tax drag.

Segregated Account and Investment Options:

Since PPLI falls under the category of variable universal life insurance, the net premium is allocated to the carrier’s segregated account, separate from the general account and protected from creditors. The segregated account consists of various pre-determined investment options provided by the carrier, including a range of alternatives. These options are fixed or locked-in, similar to investment offerings in a 401K menu. However, the inner workings of the segregated account can be highly customized by utilizing separately managed accounts (SMAs), creating customized insurance dedicated funds (IDFs), or a combination of both.

By understanding the mechanics of PPLI and utilizing the flexibility offered within the segregated account, individuals can optimize their tax efficiency while protecting their assets and beneficiaries.

PPLI vs. Traditional Life Insurance: What’s the Difference?

Traditional Life Insurance

Permanent life insurance (regardless of PPLI or traditional) provides a death benefit to beneficiaries upon the policyholder’s death. It also offers the following four tax advantages (assuming Non MEC status):.

Tax deferred growth of underlying investments (i.e., cash value)

Ability to withdraw funds tax free, up to the cost basis in the policy

Ability to loan from the policy tax free, via direct carrier loan or pledge the policy for collateral (VUL & PPLI policies will have more stringent collateral requirements relative to fixed insurance products such as Whole Life)

Death proceeds are received income tax free to the beneficiaries

Traditional life insurance has several limitations, such as limited investment options, higher relative fees, and inflexibility. With traditional VUL, policyholders are restricted to investing in a limited number of funds chosen by the insurance company. As a result, they miss out on the potential for higher returns that alternative investments can offer. Traditional life insurance also tends to have higher upfront fees and expenses that can eat into the policy’s returns and delay a positive return on investment. Finally, traditional life insurance policies are less flexible and often include surrender charges.

PPLI Investment Flexibility and Tax Efficiency

PPLI, on the other hand, offers a range of investment options with tax-deferred growth. Policyholders can allocate their investments to various asset classes, including private equity and hedge funds. This offers PPLI a significant tax advantage over traditional life insurance as policyholders can invest in a range of assets that offer higher growth potential, without taking on the added tax drag often associated with some of those investment classes. This makes PPLI an attractive option for those looking to minimize their tax liability.

How PPLI Supports Tax-Efficient Financial Planning

Asset Protection and Estate Planning Benefits

Asset protection and estate planning benefits are significant advantages of PPLI policies. One of the primary benefits of PPLI is its ability to provide maximum asset protection. By shielding assets from potential lawsuits and creditors, PPLI policies can help protect the wealth of high net worth individuals who are at greater risk of being sued. This protection is possible when the policy is owned by an irrevocable trust, assuming the policy holder is not a named beneficiary (unless drafted in a self-settled spendthrift state)

Estate Planning Benefits

PPLI can also be an effective tool for estate planning. Policyholders can transfer their wealth to future generations while minimizing estate taxes by using PPLI. The policy is held in an irrevocable trust outside the taxable estate, and when the insured(s) passes away, the death proceeds are paid out to their beneficiaries free of income and wealth transfer tax. This influx of liquidity can then be used for estate taxes. Additionally, PPLI policies can be structured to allow for gifting to beneficiaries, which can further reduce the policyholder’s taxable estate. This can be particularly beneficial for individuals with large estates who want to ensure their assets pass on to their heirs in a tax-efficient manner.

Tax Benefits

As previously mentioned, the tax benefits of PPLI make it an attractive option for high net worth individuals looking to invest in a tax-efficient manner. One of the key benefits of PPLI is tax-deferred growth. Policyholders can invest in a range of assets, and any gains on these investments are deferred from taxes until the policy is surrendered (not taxed at all if planned appropriately).

Good and Bad Investments for PPLI

While PPLI offers a range of investment options, it is important to not only choose investments that are suitable for the policyholder’s investment objectives and risk tolerance, but also balance in investments that tend to generate unfavorable taxable income while also providing the potential for attractive returns. These include private credit, high turnover hedge funds, direct lending, private equity, etc. However, there are also various risks associated with certain investments. For instance, investing in hedge funds may lead to high mgt. fees and volatility. Private equity investments may also be risky due to the lack of liquidity and potential for significant losses. It is important to conduct due diligence and carefully evaluate the risks associated with each investment before making a decision.

Connect With Centura

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients with fully transparent reporting and tools to make informed decisions around their wealth plan.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1475002191.jpg14142121Christian Duranhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngChristian Duran2023-06-09 18:52:002024-08-19 18:54:32The Role of PPLI in Tax-Efficient Financial Planning

The combination of the Federal Reserve’s lenient monetary policy before and after the pandemic, and substantial economic stimulus measures, resulted in a considerable swelling of bank deposits. Last March, the Fed commenced the fastest tightening cycle in decades, increasing the overnight lending rate from essentially 0% to 5%. When the Fed increases bank borrowing rates and interest rates increase, banks generally raise the rates at which they lend money, while usually maintaining the interest paid on deposits. As a result, this boosts their net interest income. When 6-month Treasury Bills pay more than 5% and money market funds pay over 4% while bank deposits average less than 0.50%, depositors are incentivized to direct their money out of the bank and invest in Treasury Bills or money market funds. What happened with Silicon Valley Bank (SVB) was a collapse of confidence in unprecedented circumstances – an exodus of large investor deposits, more than the FDIC-insured limit of $250,000. This unexpected development caught SVB specifically, and other banks, off-guard, resulting in significant losses showing up on their balance sheets, as detailed next.

Take That to the Bank

According to the Wall Street Journal, in the days following SVB’s collapse, the 25 biggest US banks gained $120 billion in deposits. Small banks experienced $108 billion in outflows over the same period, resulting in the largest weekly deposit decline for small banks on record. Meanwhile, more than $220 billion has flowed into money-market funds.

A bank’s business model is to take in deposits, lending to individuals and businesses, and investing the balance (often a portion in long-term fixed-rate bonds), classifying investments they expect to hold for one year or longer as Held-To-Maturity. These Held-to-Maturity securities are held on bank balance sheets at amortized cost, and therefore do not reflect the traditional mark-to-market pricing as securities classified as available for sale; thus, bank balance sheets do not reflect the magnitude of losses resulting from the Fed increasing rates by 5% over the last year.

Because the demand from SVB depositors was too great, SVB had to convert their long-dated Held-to-Maturity assets to available for sale, triggering a loss of $1.8 billion on the conversion from Held-to-Maturity to available for sale securities. Ultimately, financial regulators stepped in and took over operations of SVB. Days later, Signature Bank (SBNY) followed suit, and UBS acquired Credit Suisse (with the forced intervention of Swiss regulators) to prevent them from facing the same fate as SVB and SBNY.

To prevent a bank-run contagion, the Fed stepped in on March 12th, providing liquidity to institutions through the Bank Term Funding Program (BTFP). Under this program, banks can, if needed, borrow reserves against their assets up to the par value; this is to provide liquidity to depositors without recognizing losses by preventing the sale of Held-to-Maturity assets. Through the BTFP, the Fed has injected approximately $400 Billion into the economy, working counter to their current $95 billion monthly balance sheet reduction.

Banks rely on deposits to fund their lending and expansion, so as they experience declines in their deposit base, lending activity decreases, negatively impacting borrowers’ ability to access capital moving forward. Consequently, this situation could restrict consumer demand and accelerate the Federal Reserve’s fight against inflation, forcing them to pause rate hikes after May’s meeting.

Market Recap

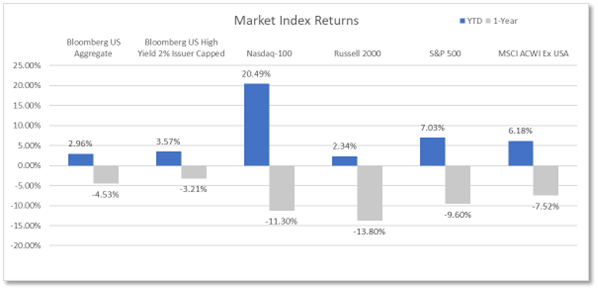

Equities – In what has shaped up to be primarily a low-quality rally despite mounting obstacles, the market demonstrated resilience for the second consecutive quarter. Many of 2022’s worst performers have been 2023’s darlings. The first quarter of 2023 saw the S&P 500 post a 7.03% return, marking the third time (1981 and 1938) in the last 15 bear markets the index posted back-to-back quarterly gains. Though the Fed continues to tighten monetary policy, the market anticipates the rate hiking cycle is nearing the end and expects the Fed will reverse course and lower rates later this year, especially on the heels of the unfolding banking challenges.

Interest rate-sensitive stocks led the charge, with the tech-heavy NASDAQ producing a first-quarter return of 16.77%. Among the biggest beneficiaries of investors shifting from financials to cash-rich companies were the largest growth-oriented equities, as evidenced by the NASDAQ 100’s Q1 return of 20.49%. With a gain greater than 20%, the NASDAQ 100 has technically entered a bull market, with the NASDAQ composite knocking on the bull’s door, returning 19.67% since bottoming in December 2022.

While market participants expect the Fed to pivot in the coming months, the Fed’s February meeting minutes suggested that further rate hikes are needed to dampen inflation. The Fed’s vow to keep rates elevated for longer signaled the peak for small-cap equities. From the start of the year through the Fed’s announcement on February 2, the small cap Russell 2000 index had gained 11.33%. Bank liquidity challenges are compounding the concerns for small cap equities as access to capital and lending standards tighten. The combination of these fears pushed the Russell 2000 nearly 10% lower from the Fed’s February meeting through the end of the quarter, with the Russell 2000 ending Q1 up only 2.34%.

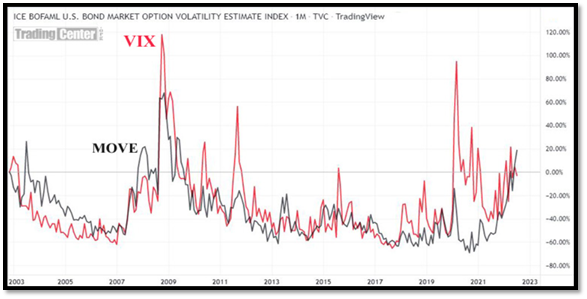

Bonds – Traditionally considered ‘safe’ investments in a portfolio, bonds continue to take investors on a wild ride. Treasury Bond volatility (as measured by the MOVE index) outpaced equity volatility (as measured by the VIX) in the first quarter, leading many to question the validity of the Treasury security as the ‘safest asset.’ Periods like the first quarter serve as a reminder that investing in Treasury securities removes credit risk, but not volatility, from consideration.

At the beginning of the New Year, concerns about long-term growth prospects and anticipation the Fed would cut rates by year end caused yields on the 10-Year Treasury to decline by 0.51%, dropping from 3.88% to 3.37%. After January’s inflation report and the Fed’s February meeting, market expectations abruptly shifted, pushing the Fed Funds peak rate expectations from ~5% to close to 5.5%, and pushing the 10-year back above 4%.

Queue the collapse of Silicon Valley Bank, forcing investors to flock to the safety of Treasury securities and pushing the 10-year back below 3.4%. In light of the Fed’s comments following their March meeting, along with the apparent stabilization of the country’s banking system, yields have risen, with the 10-Year Treasury now at 3.48%. As volatile as yields were in the year’s first quarter, bonds still produced a return of 2.96%.

Source: YCharts

Economy: Feel the ‘Pain’

After two consecutive quarters of negative real GDP growth in 2022 of -1.6% and -0.6%, real GDP rebounded to 3.2% and 2.6% in the third and fourth quarters.

Underpinned by a robust labor market and solid wage growth, consumers have proven resilient in the face of 40-year high inflation and higher interest rates. The fourth quarter’s final GDP reading showed that consumers may be starting to feel the pain with spending advancing only 1%. Reduced consumer spending leads to slower economic growth (and potential recession). Additionally, declines in exports, nonresidential fixed investment, and state and local government spending contributed to lower growth figures.

Inflation & Interest Rates

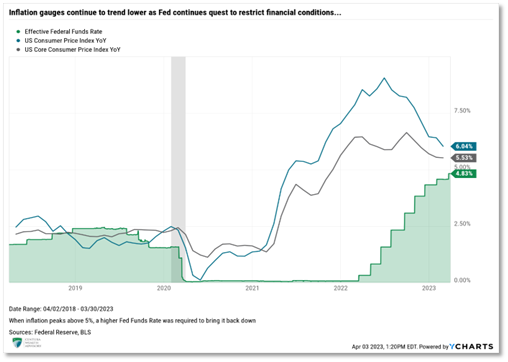

Month-over-month readings continue to post positive marks. Year-over-year inflation trended lower from its June 2022 peak of 9.06%. Though inflation came in higher than expected in January causing equity markets to sell off and yields to rise, February’s reading was in line with expectations.

January’s and February’s headline CPI came in at 6.41% and 6.0%, respectively, while core CPI (excluding energy and food) registered 5.55% and 5.53% year-over-year readings over those same periods, as both measures still increased month-over-month. The most problematic component of inflation is the resiliency of price pressure on core services, particularly shelter – a sticky and not-so-transitory variable representing about 1/3 of CPI. Shelter continued to trend upwards, increasing 8.1% over the last year – the highest growth rate since 1982. On a positive note, rents are coming down, and home prices are off their June 2022 peak, pointing to lower inflation readings ahead.

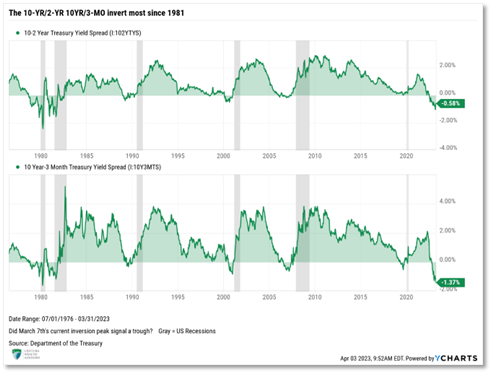

Prior to the banking failures, we continued to see larger increases on the front-end of the yield curve, causing the inversions to worsen across several maturities, sending even stronger and more ominous recession signals to the market.

Recession has been a headline topic over the last few quarters. One of the most prominent and accurate yield curve inversion points is on the 2-Year US Treasury versus the yield on the 10-Year US Treasury (10/2). Its peak reached an inversion of -1.07% on March 7th and narrowed slightly to close the quarter inverted -0.58%, only 0.05% higher than the start of the year. The last statistically meaningful yield inversion was in the fourth quarter, with the 10-Year to 3-Month Treasury spread crossing into negative territory on October 26. Remaining inverted for the rest of 2022, it picked up momentum through the year’s opening quarter to -1.37%.

At their current levels, both inversion points mark the largest inversions since 1981. Inverted yield curves have proven solid predictors of a recession. Typically, a recession follows anywhere from 12 to 24 months after the initial inversion. For reference, the 10/2 yield curve remains inverted since July 2022.

According to LPL Research Fixed Income Strategist, Lawrence Gillum, one of the timelier signals derived from inversions is when the curve troughs and the yield curve finally begins to steepen, with the spread moving from negative, back to positive territory. Outside of the early 1980s, the steepening of the curve toward positive territory proved to be a timelier indicator, as the average time from an inverted yield curve trough to a recession shortened to roughly 12 months during these periods.

Finding Balance

After its balance sheet ballooned to nearly $9 trillion post-pandemic, the Fed commenced its initiative to reduce its holdings. In Mid-March, the Fed confirmed the pace of their balance sheet reduction of $95 billion per month for the foreseeable future. Since the start of the year, the Fed has reduced its balance sheet by $167 billion through March 1, bringing the total reduction to $598B from the April 2022 peak. Since the SVB collapse, the Fed has injected nearly $400B into the economy, reinflating its balance sheet and marking a pivotal moment for The Fed. For the first time in nearly a year, liquidity is being pumped into the system (Quantitative Easing). At the same time, the Fed is aggressively engaged in Quantitative Tightening (raising rates and reducing its balance sheet by $95 billion per month).

Nonetheless, on Wednesday, March 22, the Fed decided to continue rate hikes by increasing the Federal Funds Target Rate by 0.25% to the range of 4.75% – 5.00%. Federal Reserve Chairman, Jerome Powell, pursued the narrative that inflation has run too high, and the labor market continues to remain too tight. The Federal Reserve, still committed to do whatever it takes to contain inflation, will likely raise rates another 0.25% during their May meeting. This would bring rates in line with the projected peak rate provided in the Fed’s March Dot Plot of 5.10%.

Source: www.federalreserve.gov

Unemployment

The labor market remains robust, having now recouped all jobs lost during the pandemic-induced recession. Unemployment fell to pre-pandemic levels of 3.4% through January, matching the lowest reading since 1969. Although February saw an uptick to 3.6% as the increase in the participation rate outpaced the rate of hiring for the month, there are still more than one-and-a-half job openings for every unemployed person (1.67:1).

Wage growth is one of the Fed’s primary concerns. Although wage inflation has been trending lower, it remains elevated, which worries the Fed. Strong wage inflation increases the risk of a wage-price spiral that could prolong elevated inflation. February’s CPI print marks the 26th consecutive month inflation has outpaced wage growth. Based on its updated March projections, the Fed forecasts the unemployment rate to increase to 4.5% in 2023. The strength in the labor market continues to serve as a beacon for the Fed. It provides a cushion and signals they can continue tightening monetary policy.

Centura’s Outlook

The Fed confirmed its commitment to do whatever it takes to control 40-year high inflation – not letting concerns about a potential banking crisis derail its tightening efforts. Interest rates remain at levels not seen since before the Great Financial Crisis (2008-09), so it’s no surprise to witness tighter financial conditions slowing the economy, with a likely recession on the horizon.

We still believe the two most problematic and impactful risks today are inflation and the resulting Federal Reserve monetary policy response. Concerns around bank liquidity and possible economic recession have prompted analysts to revise earnings lower. According to FactSet, the estimated earnings growth for the S&P 500 in the fourth quarter is –6.6%. If accurate, this would represent the largest decline the index delivered since the second quarter of 2020 (-31.8%). These negative revisions highlight the challenges companies must traverse to deliver profit in 2023. While the Fed’s March meeting was seen as a dovish rate increase, we believe it’s important to note that even when the Fed does stop raising rates, maintaining the current level of rates is still restrictive, and should not be viewed as the end of their tightening cycle.

A company’s ability to service debt is negatively impacted with rates expected to remain elevated. Factoring in the increased cost of labor and companies struggling to pass the increased cost of goods onto consumers, we believe the road ahead likely remains challenging to navigate. With earnings releases starting in mid-April, both top and bottom-line misses and negative management sentiment will likely dampen return expectations on equities. Forward 12-month P/E ratios are around 17.8, slightly below their five-year average of 18.5. This indicates additional drawdowns may be in store before equities become attractive from a valuation standpoint.

In addition to the Fed’s tightening regime and banks losing approximately $400 billion of deposits in March, market volatility is likely to persist through 2023, with financial conditions tightening significantly. This puts further pressure on both business and personal balance sheets. Until inflation breaks to lower levels, the Fed provides more clarity on their forward-looking monetary policy, and banking conditions stabilize, we remain cautious and anticipate that equities will experience turbulence as the first half of 2023 continues to unfold.

Our cautious outlook informs our allocations which remain underweight to respective equity targets. Our quality bias and slight value bias has served as a slight headwind in the year’s first quarter. Our underweight to foreign equities continues to provide support to client portfolios. Though the markets face a wall of worry, it’s important to remember they are forward-looking, often pricing in future economic recoveries before they happen. Given the strength of the equity market recovery since late last year, we began bringing some of our equity positioning back towards neutral or in line with our long-term target allocations. We intend to exercise caution going forward while also monitoring for opportunities to capitalize on further market dislocations.

Our fixed-income allocation continues to utilize non-traditional fixed-income investments to mitigate further risks of rising rates. The short duration of our fixed-income allocation has protected client portfolios from spiking yields and loss of principal. We have incorporated larger-than-average cash allocations to provide additional support against interest rate volatility. Furthermore, yields on cash money market funds became attractive for the first time in several years. These cash allocations generate an attractive income stream and allow us to pivot as we identify opportunistic investments for superior risk-adjusted returns.

We continue to succeed in improving returns and reducing risk by incorporating many private and liquid alternative investments to our allocations. The ramifications of spiking interest rates still impact private real estate and we anticipate additional downward valuation adjustments in many markets. We are particularly concerned with commercial office real estate, as several cities are experiencing office vacancies above the national average of 18.7% (the highest ever). With approximately $46 billion of variable rate office debt, we believe defaults on commercial real estate loans could increase over the balance of 2023, potentially adding to challenges in the banking sector.

Our focus on real estate industries possessing a large favorable supply/demand imbalance, like multifamily real estate, should help mitigate losses relative to other real estate sectors not possessing similar disparities. Despite the expected challenges in the real estate market, we maintain our dedication to exercising patience and selectivity in our decisions.

As Centura continues to enhance our alternative investment platform, we will remain focused on high-quality, conservative core exposure, with an eye toward opportunities to capitalize on the dislocations that often happen in private markets due to illiquidity and information disparities.

Thank you for your continued confidence and support. While we face multiple challenges, we remain anchored to our core principles which we believe will allow us to navigate toward achievement of your wealth building objectives. If you have questions or concerns, please contact your Centura Wealth advisor.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on the market and other conditions. These documents may contain certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Centura Wealth Advisory is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Centura Wealth Advisory and its representatives are properly licensed or exempt from licensure. 12255 El Camino Real, St. 125, San Diego, CA 92130.

https://centurawealth.com/wp-content/uploads/2024/08/AdobeStock_581041271-scaled.jpeg17072560Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2023-04-04 20:04:002024-08-19 20:06:46Market Wrap: The Fed Brings the ‘Pain’ to Banks

As you start thinking about the process of selling your business, compare this process to a game of baseball. Where do all pick-up baseball games start? With picking your team.

So, captain, who’s your first pick?

While captains are typically great players also, they may not have the expertise needed to fill the roster with the best possible team. You’ve built your business to what it is today, and that’s exactly where your expertise lies. So, how would you know how to assemble the correct team to help sell your business?

The short answer: You don’t have to. That’s where the coach comes in.

By coach, we’re referring to your wealth advisor. At Centura, we help facilitate the sale of your business by providing forensic analysis of your current professional roster and recruiting heavy hitters when necessary.

So, what do we look for when recruiting for your business’ sales team?

The Team You Need to Sell Your Business

Although there are various other positions you might need to fill depending on your unique business, here are five non-negotiable team players that can help sell your business.

Accountant/CPA – The Catcher

The right accountant or CPA acts as your catcher because they can help recommend the best course of action through an analysis of your business.

Depending on the complexity of the sale, a CPA who has specific experience structuring a business for the sale can act more as a consultant during the selling process.

What is the Accountant’s Role On the Team?

Your accountant or CPA plays an integral role in the sale of your business. They are involved in the pricing, due diligence, and negotiation process of the sale. The accountant will need to review your records and advise you on the best structure for your business sale while considering one of the biggest challenges in the sale of your business: taxes.

Appraiser – The Shortstop

People say that the secret to building a successful baseball team is to be strong up the middle. Here’s where your shortstop, or appraiser, comes in.

What is the Appraiser’s Role On the Team?

The appraiser’s role on the team is to evaluate your business’ value. Does your business involve intellectual property, proprietary processes, brand awareness, and other assets that can be difficult to put a monetary value on?

If so, it may be helpful to enlist the help of an appraiser. This professional thoroughly understands your business and what other, similar businesses are selling for. Their main goal is to set you up for success with the appraisal.

Attorney – The Umpire

Like an umpire, the attorney ensures the rules are followed; the attorney is responsible for making sure you can walk away without any potential liabilities and with the money you intended to collect.

What is the Attorney’s Role On the Team?

Your attorney plays a key role in preparing to sell your business, including a guiding hand in both:

The due diligence process

And, the negotiation process

Your attorney oversees the entire process and helps make sure your business is compliant throughout the sale.

Business Broker – Long-Relief Pitcher

Your business broker helps call the shots during the sale of your business. They are involved in the pricing, marketing, due diligence, negotiation, and closing process of the sale.

What is the Business Broker’s Role On the Team?

Every decision that is made is run through the business broker to ensure it is best for your business. Business brokers are in it for the long haul and have the stamina to last throughout the entire sales process.

Wealth Advisor – The Coach

Your wealth advisor helps see the game from a high level, making sure your team plays as effectively as possible. Where do you need to fill in the gaps to get a better business valuation? What players do you need to ‘win’ the sale?

What is the Wealth Advisor’s Role On the Team?

If you’ve ever been a part of a sports team, you know that the coach has the ability to make an exponential impact on the game. At Centura, our goal is to do just that; to positively impact your selling experience by understanding what will make you most successful. How exactly do we provide this exponential value to our clients? Read on to understand our process and see how our advisors bring value and expertise to every encounter.

https://centurawealth.com/wp-content/uploads/2024/08/Business-Selling-Team.jpg13862163Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2022-10-13 19:45:002024-08-23 19:47:09Who Am I Missing on My Team to Sell My Business?

With rising interest rates and inflation reaching a 40-year high, investors, planners and affluent individuals are searching for solutions to create financial strategies to meet their goals.

In this article, we’ll discuss several investment and planning strategies to address some of the most common financial issues faced by affluent individuals: high interest rates, inflation, and high income taxes.

Tips to Navigate a Rising Interest Rate Environment

The primary risks of a rising interest rate environment include the potential for a loss in principal value as well as a loss of buying power. Let’s take a look at some strategies that address and mitigate these risks.

Consider Investing in Private Credit

Investors may enter private credit investments because of their floating rate loans, which will limit the interest rate risk associated with other forms of investment, such as traditional fixed-income investments.

Additionally, private credit transactions are direct negotiations between the lender and the borrower. This allows investors to access a wide range of private transactions and negotiate terms that best work for their situation.

Collateralized Loan Obligations (CLOs)

A collateralized loan obligation (CLO) is “single security backed by a pool of debt….Collateralized loan obligations (CLO) are often backed by corporate loans with low credit ratings or loans taken out by private equity firms to conduct leveraged buyouts.”

With collateralized loan obligations, an investor receives scheduled debt payments from the underlying loans. The investor is offered greater diversity and the potential for higher-than-average returns in exchange for taking on the default risk.

Life insurance can be a powerful vehicle for alternative investments. It provides downside protection, high liquidity, and an attractive upside potential relative to investments with a similar risk profile.

Check out episode 31 of our podcast, Live Life Liberated, to learn more about how life insurance solutions can be used as an alternative to fixed-income investments.

Structured Notes

Structured notes, written by high credited banks, are customizable and well-suited for a rising interest rate environment and can help investors maintain returns.

Tips to Invest Against the Effects of Inflation

Multifamily real estate can provide opportunities for investors to protect themselves against their declining purchasing power.

Consider Multifamily Real Estate as a Hedge Against Inflation

Investors often view multifamily real estate as “inflation resistant.” Why? This form of investment doesn’t typically drop in value as much as other assets during challenging market times. Additionally, multifamily real estate tends to recover faster than other investments.

Further, multifamily real estate is an attractive investment during a market with rising inflation because it:

Has intrinsic value

Provides owners with the ability to adjust rent to combat the effects of inflation

Short-term bonds are less sensitive to inflation and the increased rates of a high-interest rate environment than longer-maturity bonds. Longer-maturity bonds may lock in rising rates for longer-time periods whereas shorter-term bonds require a shorter commitment to the high rates and will allow investors to move on to better opportunities.

How to Get Started With These Insider Tips

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients fully transparent reporting, and tools to make informed decisions around their wealth plan.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1341621051-1-1.jpg14142121Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2022-10-08 19:47:002024-08-23 19:49:27Insider Tips From High-Level Financial Advisors

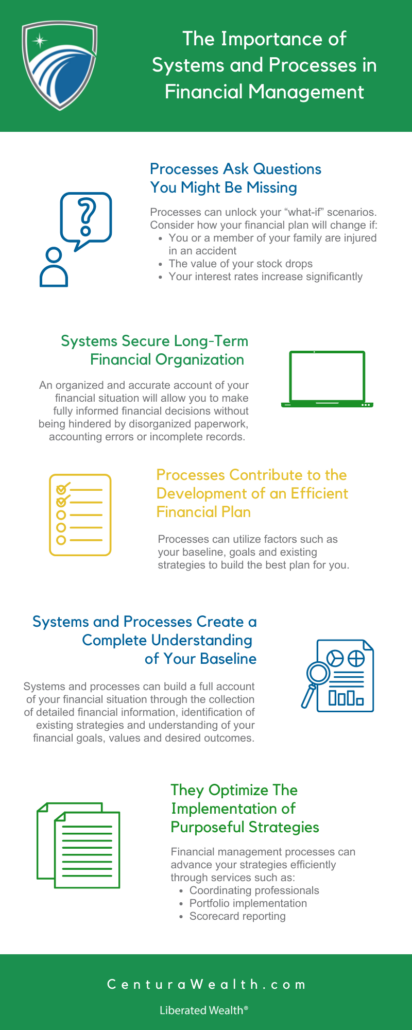

Financial management is a process by which an individual or an organization organizes and enhances its financial situation through strategies such as:

Investment management

Retirement planning

Tax planning

Estate planning

And more

Managing your financial portfolio alone can feel overwhelming. At Centura, we act as a financial partner to our clients, as we steward them toward the strategies that will work best for their unique situations. With that being said, we often use systems and processes to assist in the financial management process.

What are Financial Management Systems?

A Financial Management System (FMS) is the software and processes an organization uses to manage income, assets, and expenses. The FMS utilizes several functions to simplify financial management, such as maintaining complete audit trails as well as coordinating income statements, expense statements and balance sheets.

Further, a Personal Management System (PFM) performs similar functions to enhance the financial management of an individual or family, such as reducing accounting errors, maintaining audit trails, balancing checks, and automatically paying bills.

Why are Financial Management Systems Important?

Financial management systems and personal management systems are important because they secure long-term financial organization and efficiency. This organization will allow you to make fully informed decisions about your finances without being hindered by disorganized paperwork, accounting errors, or incomplete or inaccurate records.

What are Financial Management Processes?

Financial management processes are, in their simplest terms, plans and procedures which will help an individual, family or institution reach their financial goals. These processes can include a series of steps, such as:

Identifying financial goals

Gathering financial and personal information

Analyzing financial information

Developing a customized financial plan to achieve these goals

Processes can build an accurate and complete account of your existing financial situation through the meticulous collection of detailed financial information, identification of existing strategies, as well as the development of an understanding of your financial goals, values and desired outcomes.

You are in a Better Position to Plan for the Future

Going through a financial plan can unlock your “what-if” scenarios. Consider how your financial plan will change if:

You have to take care of your parents or family members

You or a member of your family are injured in an accident

You decide to become more philanthropic

The value of your stock drops

Your interest rates increase significantly

You decide to move

The college tuition for your child(ren) increases

Financial Management Processes Set You Up for Future Success

Regularly creating a financial plan can help you analyze your baseline, goals, existing strategies, and what-if scenarios. Through this analysis, you find what plan would best fit your needs.

At Centura, our advisors aim to understand not only your financial needs but also life events that may impact your finances. We work to create a relationship with you in order to guide you toward the best financial decisions.

It Helps You Keep a Pulse on Your Financial Performance

Implementing financial systems and processes that work for you is an essential aspect of analyzing your financial performance. Performing these processes on a regular basis allows you to make adjustments when necessary and gain a better understanding of your overall performance.

These regular adjustments ensure your plan is efficient, evolving with market conditions, and continues to align with your financial goals.

Interested in using financial processes to enhance your financial management but not sure where to start?

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1299881295-2.jpg14142121Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2022-05-29 16:11:002024-08-27 16:14:09The Importance of Systems and Processes in Financial Management

At Centura, we are dedicated to providing superior risk-adjusted returns and employing passive, active, and alternative investment strategies in our portfolio designs for our clients. As per our investment philosophy, our goals are to:

Build diversified, cost-efficient portfolios

Integrate alternative investments

Implement tax mitigation strategies

We believe that to achieve these goals, our role is to act as stewards for our clients through:

Helping them fully understand their investments and portfolios

Outlining their options

Providing purposeful strategies to ensure their success.

One of the tools we use to connect to our clients is our podcast, Live Life Liberated. It provides and breaks down relevant financial information in a detailed discussion geared towards our clients.

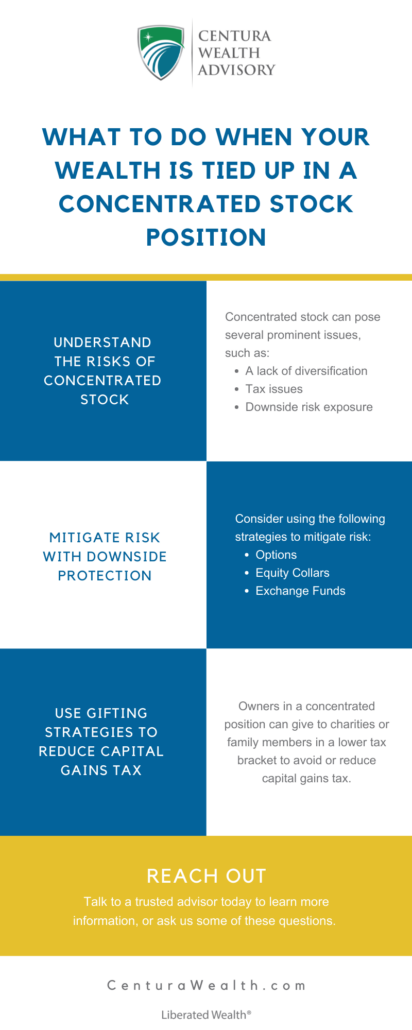

Concentrated stock can be defined as “the holding of a single stock that represents 10% or more of your overall portfolio.”

Those who may find themselves in a position of high concentrated stock include:

Founders of companies

Long-term executives

Long-term investors

Pre-IPO employees

Concentrated stock can “cut both ways” by bringing great fortune by increasing the total value of a portfolio as well as posing several prominent issues. These issues include but are not limited to:

A lack of diversification

Tax issues

Downside risk exposure

For example, Yahoo’s stocks peaked in 2000, benefiting investors with a concentrated position, before severely dropping a few years later and tanking the portfolios of investors.

Mitigating Risk with Downside Protection

While a concentrated stock position can prove to be a high-risk investment, there are strategies investors can employ to minimize this risk.

Options

Options can be used to mitigate downside risk exposure through hedging strategies that increase in value when the investments you are protecting drop.

Sean and David simplify this practice as “buying insurance to the downside of your position or giving up the upside of this position and [earning] income for doing that.”

Options can include:

Listed Options

Publicly Traded Options

Over-The-Counter Derivative Contracts

Equity Collars

The equity collar method includes “buying an out-of-the-money put option while simultaneously writing an out-of-the-money call option.” This combination provides downside protection for the owner because the put option gives them the right to sell their stock position at a given price in the future while the sale of the call option provides the investor with the income they can use to pay for the purchase of the put option.

Sean and David describe this flexible strategy as “giving up part of the upside to buy insurance for the downside.”

Exchange Funds

Owners can also choose to enter their stock in a non-taxable event, or exchange fund. An exchange fund is an arrangement or partnership between shareholders of different companies in which owners pool their large holdings of a single stock for exposure to a broader index.

Exchange funds allow the owners to:

Diversify their holdings while maintaining their concentrated position if they wish to hold onto their stock

Avoid taxes from capital gains

Use Gifting Strategies to Reduce Capital Gains Tax

Gifting to a Charity

An owner that has a highly appreciated stock with unrealized gains may benefit from a charitable gifting strategy. The owner collects credit for the charitable gift while the receiving organization gets the full value of the gift at the time it was given.

David and Sean break down this strategy in the following scenario:

If an owner has 30% basis and 70% gains and chooses to give away $100,000 of that to a charity, the owner can earn a $100,000 worth of deductions for their contribution without having to realize the $70,000 of gains. The charity can sell this gift in a non-taxable transaction and earn the full $100,000 of value.

Gifting to Family Members

An owner may also choose to give to a family member of a lower tax bracket in order to shift to a lower tax environment. While the family member will not be able to sell the gift tax-free, such as a charity can, they can potentially pay a significantly lower rate in taxes.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1167117653-1.jpg14142121Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2022-05-26 16:21:002024-08-27 16:25:45Strategies For Managing a Concentrated Stock Position

Net worth goes beyond searching for your favorite artists, musicians, and authors on Google to see how financially liberated they are. Hypothetically speaking, any individual could calculate their own net worth by counting their assets, debts, and liabilities.

But why would you do so? What value does knowing one’s net worth provide? In short, net worth is a practical tool that can help indicate a person’s financial health. This considered, let’s discuss how to calculate your net worth.

What is Net Worth?

Net worth is the value of all of your assets, minus the total of all your liabilities.

Why Is Net Worth Important?

At Centura Wealth Advisory, we unlock your wealth through innovative planning methods to find new pathways and change your wealth trajectory.

Net worth is a key tool in financial planning, especially when it comes to big life events such as mapping out your retirement strategy or purchasing a home or even a business. This figure reveals if your assets are worth more or less than what you owe, and can help predict how your wealth will grow or decrease over the course of your life.

How Do You Calculate Your Net Worth?

Formulaically speaking, calculating one’s net worth shouldn’t be all that difficult.

Again, net worth is the value of all of your assets, minus the total of all your liabilities.

Assets – Liabilities = Net Worth

It should, in theory, be a simple subtraction. However, the tricky part comes in when respectively calculating assets and liabilities.

One’s assets might include but are not limited to, an individual’s liquid and fixed assets, which might include a hodgepodge of:

Savings accounts

Checking accounts

Personal property (Real estate, automobiles, collectibles, jewelry, etc.)

Investments (annuities, bonds, cash value of life insurance policies, mutual funds, pensions, retirement plans, stocks)

A liability is any sum of money that you owe—whether it be to an institution, person, or bank. One’s liabilities might include, but are not limited to:

Mortgages

Student debt

Consumer debt

Personal loans

Auto loans

In an effort to make this process easier, we’ve created a free net worth calculator for your use.

The easiest, and most precise way to calculate your net worth, however, is to instead reach out to our team of stewards at Centura Wealth Advisory.

At Centura, we focus on generating excess cash flow to drive long-lasting wealth. Setting up your estate plan with one of our trusted advisors—so your cash flows exceed your standard of living—provides you with what we call Liberated Wealth®.

https://centurawealth.com/wp-content/uploads/2024/08/NetWorth.jpg14142121Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2022-05-20 16:28:002024-08-27 16:29:37How Do You Calculate Your Net Worth?