At Centura, we’re proud of our team and company culture. Why?

Everyone on our team has their own North Star. They center around serving our clients, our community, and their aspirations.

Wondering what our team has to say about Centura? We’ve already asked. Read on to learn more about us, what we do, and what our culture is like here at Centura Wealth Advisory.

Why Centura Wealth Advisory?

Chris Osmond, Chief Investment Officer at Centura Wealth Advisory, describes what makes Centura different from our competition.

Watch the video below or read on to learn more.

There are many reasons why advisors choose to join a new firm.

Chris remarks, “Of course, economics plays a role in their decision. You need to be able to care for your family, retire someday, etc. But, there are also a few other factors that lead advisors to join a new firm.”

One of the major factors Chris Osmond describes is “the opportunity cost of spending two-thirds of your time doing the administrative work that no one wants to do or worry about software contracts that need to be negotiated. The operational and logistic tasks take away from actually producing and spending time doing what you do best.

The business development area is where advisors typically shine; bringing in new clients, adding value, and enriching clients’ lives. At Centura, we provide infrastructure to help alleviate the cumbersome administrative tasks for our advisors, so they can do what they do best.”

What is Your Favorite Part of Centura’s Company Culture?

Click the link or read on to hear about Samantha’s favorite part of Centura’s company culture.

According to Samantha Lawrence, Associate Advisor, her favorite part about company culture are the Fridays. Why? Samantha explains:

“While at Centura, we do plan large events for the whole company, the routine Fridays are what make Centura great. Fridays are fun at Centura. We aim to make our employees excited to come to work and excited for their weekend. And we want Centura to be a place where our employees are excited to be here on a Friday afternoon.”

What is the Company Culture like at Centura?

Zoe Singh, Associate Advisor, describes the company culture at Centura. Click the link to learn more.

We take pride in the culture we’re creating here at Centura Wealth Advisory. Zoe describes the culture as “like a family in a way, we want to be close to everybody…I get questions about how I’m doing at work, but also how I’m doing in my personal life.”

“Working here for five years, I’ve seen a family-like environment, where everyone cares about each other. Managers care about their employees, and the whole team is really focused on the experience of new people coming in.”

At Centura, we want to make every new member of our team feel welcome. It’s important to us to have a positive work culture. After all, you’re spending so much of your day with the people you work with.

Final Thoughts

Headquartered in San Diego, California, Centura is passionate about our client’s objectives and owns the fiduciary responsibility of protecting their interests.

We strive to be the best in our chosen lines of business, not the biggest.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1322908184.jpg12992309Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2024-08-23 19:30:392025-04-08 16:22:16Centura’s Company Culture: Hear From Our Team

Multifamily real estate has long been recognized as a resilient and potentially lucrative asset class. In a recent episode of Live Life Liberated, Chris Osmond, CFA, CAIA®, CFP®, Chief Investment Officer at Centura Wealth Advisory, sat down with Rob Ireland, Managing Director at Continental Realty Assets (CRA), to explore the advantages, strategies, and market trends shaping multifamily investments today.

In this discussion, they break down how strategic real estate investments can enhance portfolio diversification, reduce tax liabilities, and capitalize on long-term housing demand.

The Strategic Benefits of Multifamily Investing

According to Rob Ireland, multifamily real estate remains a strong investment choice due to its necessity-driven demand. “You don’t necessarily need a place to work anymore. You don’t necessarily need to have a brick-and-mortar store to sell your product, but you need a place to live,” he explains.

Some key advantages of investing in multifamily real estate include:

Tax Efficiency: Investors can leverage depreciation, cost segregation analysis, and capital gains treatment to enhance returns.

Steady Demand: Housing is a fundamental need, with supply constraints further driving long-term demand.

Resilience in Market Cycles: Multifamily real estate has historically outperformed other commercial real estate asset classes.

Navigating Market Challenges & Opportunities

Despite current economic fluctuations, CRA remains optimistic about multifamily real estate. “Single-family homes are simply unaffordable for many,” says Ireland. “There’s a $680 delta between the cost to own a home and the cost to rent, so demand for multifamily housing remains strong.”

However, the market is not without challenges. Ireland notes that “high financing costs have slowed down new housing developments, which will compound the supply-demand imbalance in the coming years.” For investors, this creates an opportunity to acquire assets at a discount before the market corrects.

Centura & CRA: A Strategic Partnership

One of Centura’s guiding principles is ensuring strong alignment between investors and asset managers. “When we make any investment, particularly in alternatives, we want to establish a win-win-win outcome: a win for our clients, a win for our asset managers, and a win for Centura,” explains Osmond.

CRA’s rigorous market research and data-driven approach align well with Centura’s investment philosophy. “We look at job-to-permit ratios, affordability metrics, and economic trends before making any acquisition decision,” says Ireland. “We treat every market like a stock analyst would approach equities, ensuring we invest in the right locations at the right time.”

The Long-Term Outlook for Multifamily Investing

As interest rates stabilize and new supply dwindles, Ireland sees significant upside for investors in the coming years. “We believe that in 2025 or 2026, some markets may see double-digit rent growth again,” he predicts.

Quoting Warren Buffett, Ireland emphasizes, “Be fearful when others are greedy, be greedy when others are fearful. Right now is one of the best times in the last 20 years to invest in multifamily real estate.”

Learn More

For those interested in multifamily real estate investments and Centura’s approach, connect with Centura Wealth Advisory or reach out to CRA for more insights.

https://centurawealth.com/wp-content/uploads/2025/02/investing-in-multifamily-real-estate-with-rob-ireland-Episode-98.jpg14532064Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2024-08-21 10:22:002025-04-08 16:16:43Ep. 98 Investing in Multifamily Real Estate with Rob Ireland

After rising more than 10% in the first quarter of 2024, the S&P 500 stumbled out of the gate in the second quarter. The index contracted more than 4% in April and produced the first negative month of the year as the market reassessed the timing of the Fed’s first rate cut. While the Fed’s higher for longer mantra has not changed, they are stressing their dependence on data, which has proven mixed. The market, on the other hand, has become Fed-dependent, placing great emphasis on each major economic reading, primarily inflation, labor, and economic production. With hopes that the Fed will initiate rate cuts sooner, the market applauds lower inflation and negative growth signals, like a slowing economy or consumer spending. Conversely, traditionally well-received data points, such as a robust and resilient labor market, can trigger market selloffs. This counterintuitive reaction occurs because positive economic news suggests that the Federal Reserve might delay its first rate reduction, extending the timeline for monetary easing.

Following two positive reports that inflation is trending lower, the S&P 500 witnessed solid rebounds of 4.80% and 3.47% in May and June, respectively, driven primarily by gains in Big Tech stocks. With hopes of an early rate cut, the equity markets continued to fuel the Nvidia-led AI frenzy. The sustained AI rally is heavily influenced by expectations surrounding the timing of monetary policy adjustments.

In line with the April selloff in equities, bonds saw the yield on the 10-year US Treasury whipsaw 0.37% higher, from 4.33% to 4.70%, before peaking on April 25. Like their equity counterparts, longer-dated bonds have become too reliant on the path of monetary policy, with return expectations tied to the timing of the Fed’s first cut. As the Fed provides clarity on their path forward, yield volatility should ultimately subside, leading to more stable outcomes. Until then, we expect continued bond volatility.

Market Recap

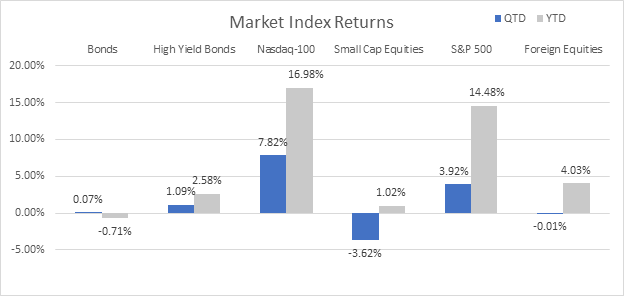

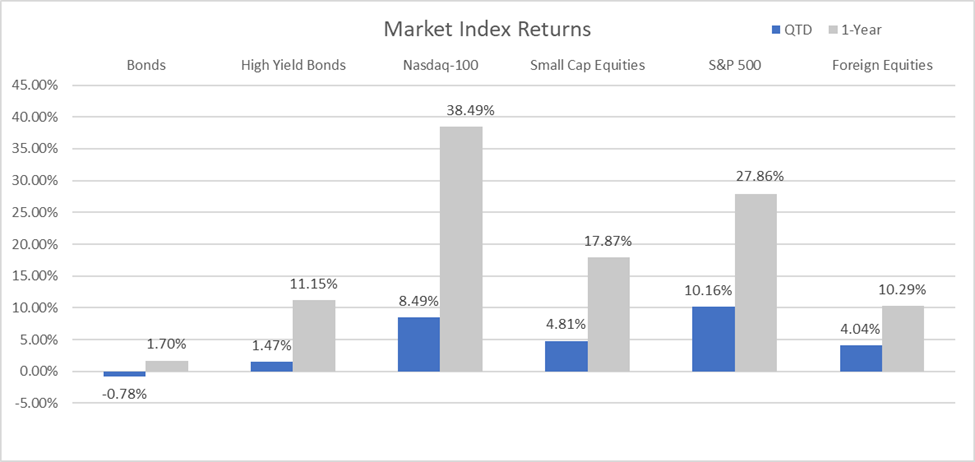

Equities – Unlike the ‘everything rally’ that closed out 2023, where small caps and technology stocks – both sensitive to elevated interest rates – were the largest benefactors, 2024 has witnessed further decoupling amongst asset classes. Any projected rate cut speculation has tended to support higher returns by the Magnificent Seven and technology stocks, though small caps have lagged behind. Small caps, measured by the Russell 2000, produced only about half the return of their large cap counterparts in the first quarter. The second quarter witnessed smaller companies contract -3.62%, bringing the year-to-date gains to a paltry 1.02%. Meanwhile, the S&P 500’s price advances for the second quarter was 3.92%, bringing the index’s return for the year to 14.48%.

Bonds – As yields reversed course, bonds kicked off the quarter in the red, adding to their multi-year downward trend. With stronger-than-expected economic data and Fed uncertainty, the market repriced Fed expectations, and the yield on the 10-year U.S. Treasury rose sharply. As inflation readings and consumer spending data continued trending lower, the market again reassessed their rate cut projections, sending the 10-year U.S. Treasury yield back to 4.2% and bringing the bond index back into positive territory for 2024. The Fed’s messaging that it needs to witness several months of sustained data before feeling comfortable lowering rates prompted another yield reversal upward with the 10-Year U.S. Treasury closing the quarter at 4.36%. While the market has appeared to reprice monetary policy changes, robust U.S. debt issuance and the demand for U.S. Treasury securities remains relatively weak, failing to absorb supply and applying additional upward pressure on yields. The Bloomberg U.S. Aggregate Bond Index rose by a modest 0.7% in the quarter, while it declined -0.71% for the year.

Source: YCharts. The Bloomberg US Aggregate Index was used as a proxy for Bonds; the Bloomberg US High Yield 2% Issuer Capped Index was used as a proxy for High Yield Bonds; the Russell 2000 Index was used as a proxy for Small Cap Equities; and the MSCI ACWI Ex USA Index was used as a proxy for Foreign Equities. All returns are based on price returns as of 06/30/2024.

Though economic data remains mixed, base case expectations still call for the Fed to successfully achieve a ‘soft landing’ and avoid recession. However, many growth metrics continue to moderate, leading many to question the Fed’s decision to keep rates elevated for longer.

Economy: The Consumer continues to slow

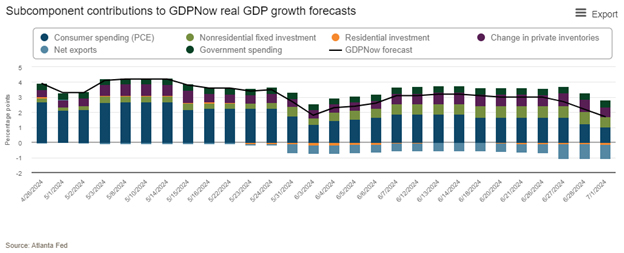

After growing approximately 2.5% in 2023, the U.S. economy continues growing at a moderate pace. Driven primarily by softening consumer spending, the first quarter of 2024 GDP grew 1.4%. Reflecting an uptick over the first quarter, as of July 2, 2024, the Atlanta ‘Fed’s GDPNow model for Q2 has been revised from 2.2% to 1.7%. This revision is primarily due to lower projections for consumer spending and net exports, which have contracted from the initial growth forecast.

The combination of unwavering spending in the face of rising prices and a robust labor market has underpinned the strong economic growth of recent years. However, with the $2 trillion of pandemic savings now exhausted as of March, household debt has reached record levels, and delinquencies are beginning to mount, threatening the sustainability of the nation’s growth. Despite elevated borrowing costs, the consumer continues to spend, albeit at a slower pace, thanks in large part to a strong labor market, producing wage increases that have outpaced inflation for more than a year. While the market is hoping for the labor market to soften and result in an earlier Fed rate cut, too much labor market deterioration could result in further spending reductions, ultimately leaving little room for the Fed to thread the needle and both produce a ‘soft landing’ and avoid a recession.

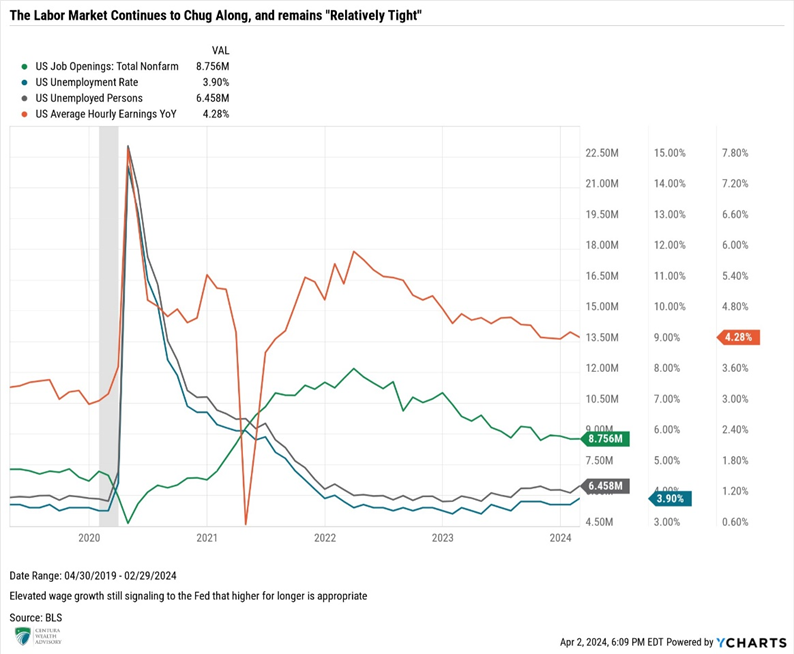

Unemployment

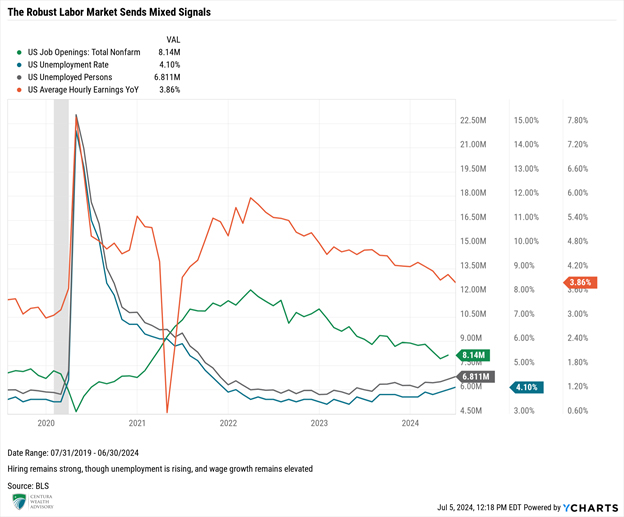

June’s Labor Market Report registered the 42nd consecutive month of job gains. Estimates called for 200,000 jobs in May, and the market once again surprised to the upside with the addition of 206,000 jobs. On the other hand, the unemployment rate edged up slightly to 4.1%, the highest level since October 2021.

The labor market continues to post robust results. While trending lower since peaking in 2022, job openings (JOLTs) surprisingly broke its three-month trend of fewer job openings in May. They reversed back above eight million (8.14 million), bringing the ratio of job openings to those unemployed to down to 1.22:1. While the ratio of 1.22:1 is still elevated above levels historically witnessed, the ratio has fallen significantly from nearly two job openings for every job posting in 2022, indicating slack is working itself out of the system and the labor market is showing signs of tightening. The number of open jobs has fallen, while the number of unemployed job seekers has trended higher, as evidenced by the additional 687,000 unemployed persons from January to May.

For now, the strength and resiliency of the labor market have given the Fed the confidence to keep rates higher for longer. However, the data point that is giving the Fed continued anxiety is wage growth. Despite falling below the key level of 4% in April for the first time since 2021, wage growth has exhibited stickiness and has been hovering around the 4% threshold, rising 4.1% and 3.9% year-over-year in May and June, respectively. While wage growth outpacing inflation bodes well for continued consumer spending, prolonged, elevated wage growth raises concerns about a potential resurgence in inflation. Several readings below the 4% threshold would certainly be welcomed by the Fed.

Inflation

On the surface, all major inflation readings have fallen below 4%, with both PCE readings coming in at 2.6% in May. Core services increased by 0.2% in May, lifted by higher housing, utilities, and healthcare, and financial services, while insurance costs declined by 0.3% after five consecutive months of growth. Housing, financial services, and insurance costs were among the major drivers supporting elevated services costs, so witnessing a reversal in two of the three variables presents a positive affirmation that inflation is indeed heading lower.

Just as elevated wage growth is troublesome to the Fed, the stickiness of core services, particularly housing, fortifies the decision to exercise patience before cutting rates. Federal Reserve Chair Jerome Powell stated “we want to be more confident that inflation is moving down towards 2%” before lowering rates.

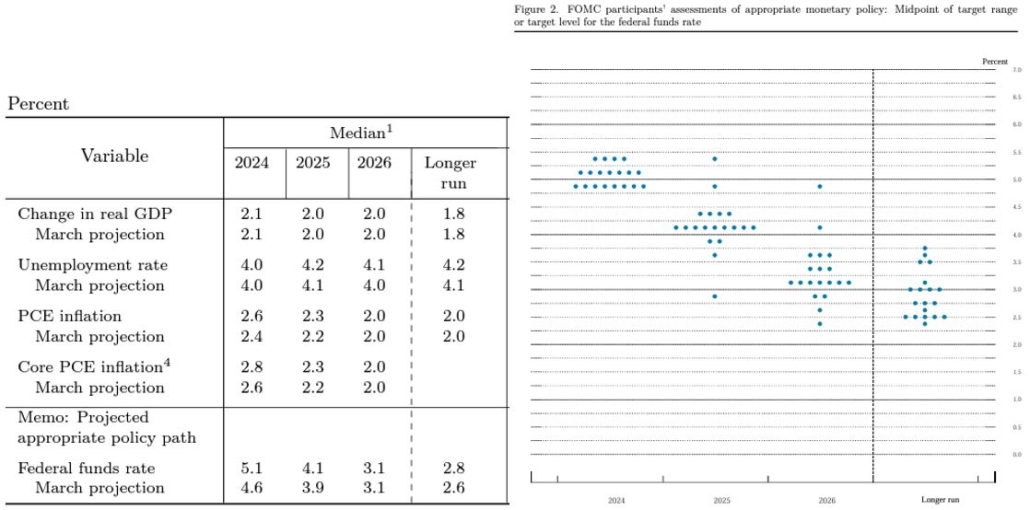

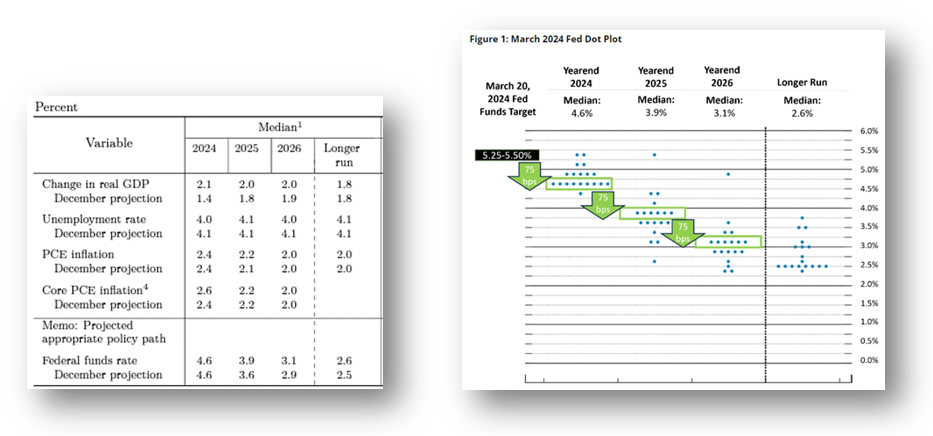

More Evidence Needed

The Federal Open Market Committee (FOMC) elected to keep rates unchanged in June for the seventh consecutive meeting. While the Fed’s decision was largely expected, the big news was centered around the Fed’s changes to their Summary of Economic Projections, particularly their median projection for rate cuts, where policymakers adjusted their expectations from three rate cuts in 2024 to only one 0.25% rate cut. The Committee also raised its projection for 2025 as well, indicating a slower pace of change as the Fed adopts a more patient data-dependent position. The number of Fed officials who projected no cuts in 2024 doubled from two to four, and not one official anticipated cutting rates more than twice. We also saw the Fed lift economic projections for 2024 increasing their 2024 inflation expectations and revising their 2025 rate normalization path.

Powell acknowledged that inflation has begun trending lower, yet expressed concerns that cutting rates too early may jeopardize the progress made towards reducing inflation. Interestingly, the Core PCE print in May was 2.6%, which is higher than the Fed’s year-end projection for Core Inflation. This indicates that the Fed anticipates a slight increase in prices from this point, which would likely be accompanied by ensuing market volatility.

Barring any resurgence of inflation, we believe the Fed has finished its rate-hiking regime and is nearing its first rate cut. Our base case assumptions have not changed given the Fed’s steadfast commitment to bringing inflation down. We continue to believe the earliest the Fed will cut rates is September, which now aligns with current market expectations. However, any prolonged stickiness or resurgence of inflation would likely push our expectations for rate cuts into the fourth quarter this year.

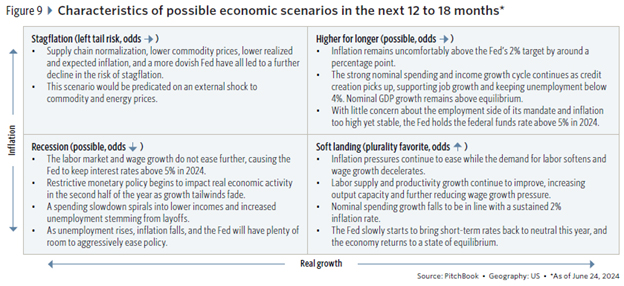

Centura’s Outlook

The Fed’s goal to lower inflation to its 2% mandate and avoid recession is now the base outcome expected by the Fed and most market participants. However, given the slowdown in consumer spending, the Fed will need to monitor the state of the labor market deterioration closely if they are to fully avoid an economic contraction. Successfully delivering lower inflation and monetary policy normalization should bode well for equities and bonds. However, there are several potential risks looming and investors should proceed carefully.

In the chart below, Pitchbook outlines four likely paths forward: scenarios of stagflation, higher for longer, recession, or a soft landing. While any of the four scenarios could occur and the risk of recession has fallen, this risk remains above average due to the restrictive level of interest rates. Ultimately, our expectations fall into the lower right-hand corner: the soft-landing camp. We believe inflationary pressures will continue to ease while labor demand and wage growth will soften, resulting in the Fed slowly beginning to bring short-term rates down.

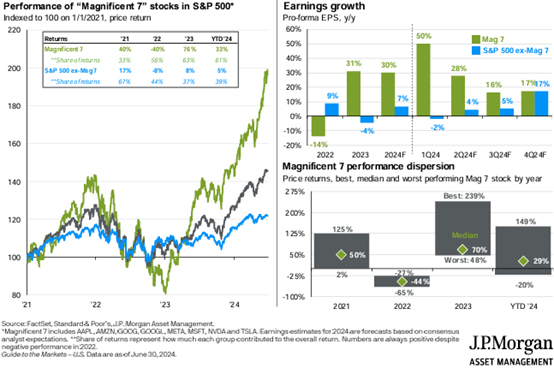

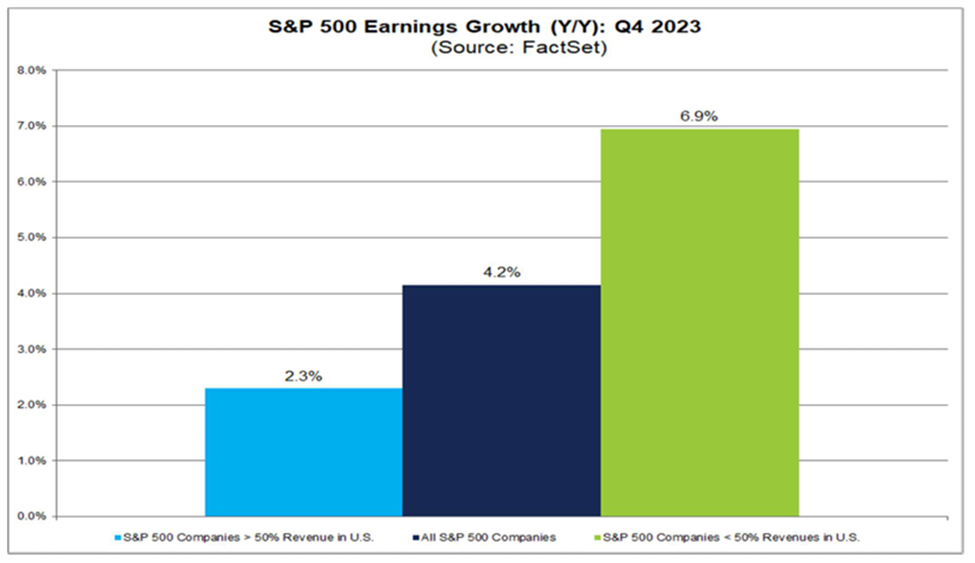

In the face of higher borrowing costs, corporate profits have remained surprisingly resilient, illustrated by the S&P 500 posting positive earnings growth for the third consecutive quarter in the first quarter of 2024, rising 5.9%. As of June 21, FactSet estimates second-quarter earnings to accelerate and grow at 8.8% year-over-year. Last year, the Magnificent Seven were responsible for most of the market’s earnings growth, increasing 31%, versus the -4% contraction of the remaining 493 companies’ earnings in the S&P 500. While this trend is expected to hold in 2024, with gains of 30% and 7%, respectively, we are encouraged that JPMorgan is expecting the remaining companies outside the Magnificent Seven to catch up and accelerate earnings over the remainder of the year. Both groups are expected to experience year-over-year earnings growth of 17% in the fourth quarter. A broadening of earnings growth should bode well for increased market breadth and carve a path for higher broad-based returns on equities.

The market remains too dependent on the Fed, which has become dependent on poor economic data. Following worsening conditions, the Fed is more likely to pivot and cut rates sooner. We believe economic activity will continue to surprise moderately, putting the Fed on pace to start lowering rates in either September or November, yet any resurgence of inflation will likely spur bouts of volatility in both stocks and bonds.

Persistent, elevated rates will continue to cause issues for some companies, like small caps, though earnings are expected to grow broadly in 2024 and 2025. While equities generally produce positive returns during election years, we expect volatility is likely to increase as we approach the election in the third and fourth quarters. The recent political turmoil in France and India, the first U.S. Presidential Debate, and the ensuing market volatility remind us how sensitive the markets are to political uncertainty. While we anticipate increased volatility as November nears, we do not believe this volatility source is sustainable. Outside of a resurgence of inflation or Fed policy misstep, we believe geopolitical risks pose a major threat and are more fearful of those potential exogenous events that are harder to predict.

While the path may be bumpy, we believe yields should continue to grind lower over the course of the year, presenting attractive opportunities to produce asymmetric returns in bonds. Extending duration within portfolios should allow investors to clip an attractive yield, while also providing them with the opportunity to experience capital appreciation for a total return exceeding what they might clip sitting in money market funds or short-term Treasury bills, particularly in municipal bonds on an after-tax basis.

Elevated interest rates continue to punish private real estate returns, with further slight downward valuation adjustments expected from their previous marks. Real estate serves as an interest rate-sensitive asset class; as rates move lower, we anticipate a pick-up in activity and a subsequent reversal of valuations over the next several years. While we believe we are nearing the light at the end of the tunnel for several real estate sectors like multifamily and industrial, unfortunately, we believe more pain will be experienced, particularly with the underlying debt that real estate operators hold. We anticipate a pickup in defaults across several real estate sectors, likely resulting in further pain across both public and private markets. For the foreseeable future, we remain extremely cautious and selective, focusing on select submarkets and attractive risk-adjusted returns.

Private equity, particularly lower middle market buyouts, appears to have stabilized, potentially presenting attractive investment opportunities relative to public market alternatives. Current yield levels present challenges for private equity valuations, though according to Pitchbook, elevated and expanding public equity market valuations position new buyout investments favorably when compared to their public market counterparts. Generally, when public market valuations are well above historical norms, buyout strategies launched during these periods tend to outperform, particularly smaller and emerging managers, which aligns with our natural preference. With limited private equity exit opportunities today, we also align with Pitchbook’s stance that secondary investments should also create attractive opportunities for investors in this environment.

Given that private credit is predominantly floating and tied to a base rate such as the Secured Overnight Financing Rate (SOFR), closely linked to the Fed Funds overnight rate, we believe the asset class remains attractive. Yields on private credit should remain similar to current levels until the Fed begins to cut rates. Even as the Fed cuts rates, the floating rate on private loans does not adjust immediately. Rather, there is a delay before the loan terms reset lower. Barring a catastrophic event, the Fed is likely to lower rates slowly, supporting higher yields for longer in private credit. According to commentary shared with us from Cliffwater, companies appear to be navigating the higher financing costs well, as interest coverage in their pipeline has increased from 1.75x to 1.93x.

Like markets and the Fed, we are digesting data points as they print, but we remain laser-focused on long-term objectives and minimizing volatility in the short-term amidst this data dependent backdrop.

Thank you for your continued confidence and support. If you have questions or concerns, please contact your Centura Wealth advisor.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on the market and other conditions. These documents may contain certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Centura Wealth Advisory is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Centura Wealth Advisory and its representatives are properly licensed or exempt from licensure. 12255 El Camino Real, St. 125, San Diego, CA 92130.

Charlie Neer, Chief Revenue Officer (US) at MiQ, has navigated a transformative financial journey over the past two years as a client of Centura Wealth Advisory. In a candid conversation with Centura’s Managing Director, Derek Myron, Charlie shares his experiences, lessons learned, and how his financial strategy is now more aligned with his long-term goals.

Why Seek Professional Wealth Advisory?

Coming from a humble background and experiencing financial uncertainty early in life, Charlie reached a point where he realized he needed structured guidance.

“I’ve always been a ‘stuff money under the couch cushions’ guy,” he admits. “I had investments scattered across different apps, and it was disorganized. I was losing buying power, missing tax advantages, and not optimizing my wealth.”

The Centura Process: A Holistic Approach

Centura’s Liberated Wealth® process provided Charlie with a structured and strategic approach to wealth management, including investments, estate planning, and tax strategies.

Key phases of the process include:

Uncover: Understanding the client’s personal and financial goals, entity structures, and balance sheets.

Unlock: Identifying tax planning and investment strategies to optimize wealth.

Implement & Monitor: Ensuring execution aligns with long-term objectives.

“The depth of discovery blew me away,” Charlie says. “Centura took the time to understand my family’s goals, including my desire to retire in Mallorca, Spain, and built a plan around that.”

Trust and Transparency in Wealth Management

One of Charlie’s initial hesitations was trust.

“I don’t trust easily,” he admits. “I was waiting for the moment where the background falls down, and I realize I’m sending my money to people in The Bahamas. But Centura earned my trust by being transparent at every step.”

He appreciated Centura’s ability to provide expert coordination across different financial disciplines. “I’ve never had to chase third parties. Every lawyer, tax advisor, or estate planner they introduced me to was already prepped and aligned with my needs.”

The Value of Learning and Mastery

Beyond just financial management, Charlie found tremendous value in the educational aspect of working with Centura. “I enjoy learning, and Centura has helped me understand things I never knew—tax planning, entity structures, estate strategies. Now, I can have informed conversations with my peers about financial decisions.”

Final Thoughts: A Relationship Built on Alignment

Charlie highlights three key factors that have made his experience with Centura invaluable:

Autonomy: “I always have the final say. Centura advises, but I make the decisions.”

Purpose: “They don’t just manage wealth; they align it with my goals.”

Mastery: “I’ve learned so much, and I know I’m in the hands of true experts.”

For those hesitant to take the next step in financial planning, Charlie offers this advice:

“It took me a year and a half to commit. My biggest hurdle was my own ego. But once I realized I wasn’t the expert in this field, I was able to embrace Centura’s guidance and truly optimize my wealth.”

Connect With Centura

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients with fully transparent reporting and tools to make informed decisions around their wealth plan.

Connect with our team today to learn how we can help you navigate complex financial decisions and secure your financial future with confidence.

Disclosures

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2025/02/Ep-97-Working-with-Centura-Charlie-Neer-scaled.jpg10752560Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2024-06-26 12:47:002025-04-08 16:16:43Ep. 97 Working With Centura: Candid Feedback From Our Client Charlie Neer

Many business owners assume they are five years away from selling their company. The problem? That five-year window often remains constant, year after year. Without proper planning, the timeline for exit can keep getting pushed back until it’s too late to maximize value and ensure a smooth transition.

In a recent episode of the Live Life Liberated podcast, Centura Wealth Advisory’s Zoe Singh sat down with Andrea Steinbrenner, CEO of Exit Consulting Group (ECG), to discuss what it truly takes to prepare for an effective business exit. Listen to the full episode here:

The Three Stages of Exit Readiness

Exit Consulting Group has developed a structured approach to exit readiness that evaluates a business across three core areas:

Business Readiness: Can the company operate smoothly without the owner? If the business owner stepped away tomorrow, who would run sales, finance, vendor relationships, and daily operations? “Is the business ready to operate without that owner or leader?” – Andrea Steinbrenner

Market Readiness: Does the business have market value? What are similar companies selling for? What financing conditions will potential buyers face? “We run a valuation on the firm and we say, okay, here’s where we think the fair market value is laying up. Are there buyers out there who will pay this for your company?” – Andrea Steinbrenner

Owner Readiness: Is the business owner mentally prepared to transition? What will they do once they step away from their company? “A lot of people will tell us, ‘Oh, we’ll go golfing, we’ll go fishing.’ Well, I guarantee there’s only so many days you can do that before you need to do something else.” – Andrea Steinbrenner

Understanding the Exit Timeline and Sales Process

Selling a business is not an overnight decision—it requires strategic planning and execution. Andrea outlined the key steps in the process:

Business Valuation & Market Research: Determining a fair market price based on industry trends and financial performance.

Confidential Information Memorandum (CIM): Creating a detailed marketing document to attract potential buyers.

Buyer Vetting & Indications of Interest (IOIs): Screening potential buyers and negotiating initial terms.

Letter of Intent (LOI): Once a preferred buyer is identified, an LOI is signed to enter an exclusive negotiation period.

Due Diligence: The buyer reviews financial records, legal agreements, and operational details.

Final Negotiations & Closing: Legal documents are finalized, funds are transferred, and ownership transitions.

“Most companies get a minimum of a hundred NDAs, but you can get hundreds of them. From there, we collect what’s called IOIs—Indications of Interest—so we can begin narrowing down the right buyer.” – Andrea Steinbrenner

Internal vs. External Business Sales

Business owners often sell to either an external buyer (such as a private equity firm or strategic buyer) or an internal buyer (such as a family member, key employee, or business partner). Each approach has distinct challenges and benefits.

For internal transitions, emotions and expectations must be carefully managed. Employees or family members may not fully grasp the complexities of ownership.

“First, we have to bring them up to speed… These are now people who have access to information that before they didn’t.” – Andrea Steinbrenner

Meanwhile, external sales involve finding the right buyer, structuring the deal properly, and optimizing the tax implications of the sale.

The Role of Tax Planning in Business Exits

Centura Wealth Advisory emphasizes that the best time to start tax planning is before signing an LOI. According to Zoe Singh, business owners fall into three categories:

Gold Period: Before signing an LOI—this is when the most tax strategies are available.

Silver Period: After signing an LOI but before December 31 of the tax year—some strategies are still possible.

Bronze Period: After the tax year of sale—minimal tax strategies remain, and most tax liabilities are locked in.

“The best time to start tax planning is two to three years before an exit. That gives business owners the flexibility to optimize their tax strategy and ensure their wealth is preserved.” – Zoe Singh

The Bottom Line: Start Preparing Early

Business exits are complex, but the earlier you start preparing, the smoother the transition will be. Whether you’re planning to sell in one year or five, taking proactive steps today can maximize your business’s value and secure your financial future.

For business owners considering an exit, working with experienced professionals—like Centura Wealth Advisory for tax planning and Exit Consulting Group for transaction guidance—can make all the difference.

“The worst outcome is splitting up partnerships and families. Our goal is to find a path that everybody can agree with.” – Andrea Steinbrenner

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients with fully transparent reporting and tools to make informed decisions around their wealth plan.

Connect with our team today to learn how we can help you navigate complex financial decisions and secure your financial future with confidence.

Disclosures

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2025/02/Ep-96-Exit-Readiness.jpg14142121Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2024-06-12 01:01:002025-04-08 16:16:43Ep. 96 Exit Readiness: How to Prepare Your Business for Sale

NIMCRUTs, or Net Income with Makeup Charitable Remainder Unitrusts, are advanced charitable giving strategies designed specifically for high-net-worth individuals. These trusts allow donors to make significant charitable contributions while also providing a stream of income for themselves or their beneficiaries. NIMCRUTs offer a number of benefits, including tax advantages, potential for increased income, and the ability to support favorite causes while also meeting financial goals.

In this blog, we will explain what NIMCRUTs are, how they have evolved over time, and how high-net-worth individuals (HNWIs) can use them as part of their financial planning.

What are NIMCRUTs?

A Net Income Makeup Charitable Remainder Unitrust (NIMCRUT) is a charitable trust that allows an individual(s) to make a donation while receiving an income from the trust for a specified number of years or for the lifetime of the individual(s).

The income received by the individual(s) is based on the net income generated by the trust, usually from investments in a diverse portfolio of assets. At the end of the trust term, the remaining assets are distributed to the charities determined by the donor. We’ll get more into the benefits of NIMCRUTs in a second, but let’s first look at how Charitable Trusts came to be.

A Historical Legislative Landscape for Charitable Giving

Knowing how Charitable Trusts have been shaped by legislation over the years will give you a better understanding of NIMCRUTs and how to receive the best tax benefits.

Tax Reform Act of 1969: The first national policy on charitable planned giving is created.

Revenue Rule 77374 (1977): The probability test for charitable remainder annuity trusts is established. There now has to be less than a 5% probability that you’re going to exhaust the initial capital contribution.

Tax Relief Act of 1997: A maximum payout rate of 50% is established, as well as a 10% minimum remainder requirement.

Tax Relief Healthcare Act of 2006: A Charitable Remainder Trust (CRT) will no longer lose its tax-exempt status for having an unrelated business taxable income (UBTI) in the trust. However, there is now a 100% excise tax on the UBTI in the trust.

Knowing the rules that have been established over the years for Charitable Trusts will allow you to get the most out of their benefits while also being aware of potential pitfalls.

How High-Net-Worth-Individuals Can Utilize NIMCRUTs To Save Money

One of the most valuable features of a Net Income with Makeup Charitable Remainder Unitrust (NIMCRUT) is its ability to facilitate tax-free growth of funds over a set period or lifetime. This characteristic sets NIMCRUTs apart from simple Charitable Remainder Unitrusts (CRUTs), and may make them particularly attractive to certain individuals due to the added benefit of a “makeup” feature.

What is the NIM-CRUT Makeup Feature?

With a NIMCRUT, if the trust produces more income than it’s supposed to pay out, the excess money will go back into the trust’s principal. Likewise, if the trust produces less income than it’s supposed to pay out, the beneficiaries may receive less money that year but will have it “made up” to them from an excess year. This feature can lead to the same amount of income over time but without ever attacking the principal. With a CRUT, no matter what kind of year the trust has financially, you’re getting the same amount which can lead to the trust’s principal decreasing gradually.

Donating assets to a Net Income with Makeup Charitable Remainder Unitrust (NIMCRUT) can be a beneficial way to reduce taxable income and avoid capital gains tax. By contributing assets to the trust, an individual is able to diversify their holdings while also mitigating the risk associated with certain types of assets, such as stocks or real estate. This approach to charitable giving allows individuals to make significant donations while also receiving favorable tax treatment and potentially enhancing their financial situation. It is important to note that the specific tax implications of donating to a NIMCRUT will vary based on individual circumstances and the laws governing charitable giving in the donor’s jurisdiction.

It’s important to consult with trusted and professional financial planners when setting up a NIMCRUT as there are potential benefits and drawbacks that should be evaluated with expertise before making a decision.

Connect With Centura

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients with fully transparent reporting and tools to make informed decisions around their wealth plan.

Read on to learn more about our 5-Step Liberated Wealth Process and how Centura can help you liberate your wealth.

Disclosures

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

Alternative investments offer significant opportunities for superior risk-adjusted returns and portfolio diversification. Yet, many high-net-worth investors find their portfolios under-allocated to these assets. In Episode 95 of the Live Life Liberated podcast, Chris Osmond, CFA, CAIA®, CFP®, Chief Investment Officer at Centura Wealth Advisory, shares insights on the role of alternative investments and how Centura approaches them.

What Are Alternative Investments?

“If you just look at the standard textbook definition, it would say any investment that is non-traditional like stocks, bonds, or cash. But I would extend that to emphasize the public versus private market distinction—one of the largest differentiating factors between traditional and alternative investments.”

Alternative investments include asset classes such as private equity, private credit, hedge funds, venture capital, and real estate, among others. Unlike publicly traded stocks and bonds, these investments are often illiquid and require extensive due diligence but can offer significant upside and risk mitigation when used effectively.

Why Alternative Investments Matter for High-Net-Worth Investors

While institutional investors, such as pensions and endowments, have leveraged alternative investments for decades, individual high-net-worth investors remain under-allocated in these assets.

“The average high-net-worth investor has only about a 5% allocation to alternative investments. Compare that to institutional investors like endowments and pensions, and you see a significant gap that presents a tremendous opportunity.”

For qualified investors, alternative investments can enhance returns, reduce volatility, and improve overall portfolio efficiency. By incorporating private market investments, investors can achieve superior after-tax, risk-adjusted returns.

Centura’s Investment Philosophy: A Four-Pillar Approach

Centura Wealth Advisory adheres to a structured approach based on four time-tested investment principles:

Portfolio Optimization – Minimizing drawdowns and maximizing return through strategic diversification.

Institutional Asset Allocation – Implementing an endowment-style approach to increase alternative investment exposure.

Tax Efficiency & Asset Location Optimization – Structuring investments for the best after-tax outcomes.

Market Efficiency Optimization – Leveraging active management in inefficient markets while utilizing passive strategies for efficient markets.

The Role of Alternative Investments in a Diversified Portfolio

“Alternatives tend to have little to no—or even negative—correlation to traditional stocks and bonds. This can generate significant alpha while lowering overall portfolio risk.”

Centura employs a core-satellite strategy when incorporating alternatives.

Core: Stable, lower-risk assets like leveraged buyouts (LBOs) and core-plus real estate.

Satellite: Higher-risk, higher-return strategies like venture capital, CLOs (collateralized loan obligations), and niche private credit opportunities.

This structure allows investors to capture upside while mitigating risk through diversification and strategic allocation.

Overcoming the Challenges of Alternative Investments

Despite the advantages, alternative investments come with unique risks, such as illiquidity and lack of transparency.

“At Centura, we conduct an institutional-level due diligence process to uncover and mitigate risks. Our goal is to ensure we select the best opportunities for our clients.”

Centura’s five-stage due diligence process includes:

Identifying the Right Investment Criteria – Refining search parameters to narrow down viable opportunities.

Sourcing – Utilizing proprietary research, industry contacts, and platforms like PitchBook.

Initial Investment Screening – Conducting manager interviews, reviewing strategy alignment, and ensuring interests are aligned.

Full Due Diligence – Performing deep dives into fund structure, financials, legal contracts, reference checks, and operational risks.

Ongoing Monitoring – Engaging in regular manager meetings and performance reviews to ensure continued alignment with investment goals.

Where Centura Adds Value

Centura differentiates itself from large RIAs, wirehouses, and private banks by offering access to boutique, high-quality asset managers. Many large financial institutions are limited to well-known firms like Blackstone or KKR due to scale requirements. Centura’s independent approach allows access to both industry giants and smaller, high-performing niche managers.

Additionally, Centura actively negotiates favorable economic terms on behalf of its clients, including:

Lower management fees and carried interest

Elimination of performance “catch-up” provisions

Minimum investment reductions for accessibility

Most Favored Nations clauses ensuring clients receive the best available terms

“When we negotiate, it’s not just about reducing fees—it’s about optimizing return structures and securing the best possible terms for our clients. That’s where we add significant value.”

Final Thoughts

Alternative investments are powerful tools for wealth optimization, but they require careful selection and expert oversight. Through rigorous due diligence, strategic portfolio construction, and a focus on tax efficiency, Centura Wealth Advisory helps investors unlock the full potential of alternative investments.

For more information on alternative investments and how they can enhance your portfolio, contact Chris Osmond, CFA, CAIA®, CFP®, at Centura Wealth Advisory.

The information covered and posted represents the views and opinions of the guest and does not necessarily represent the views or opinions of Centura Wealth Advisory. The content has been made available for informational and educational purposes only. The content is not intended to be a substitute for professional investing advice. Always seek the advice of your financial advisor or other qualified financial service provider with any questions you may have regarding your investment planning.

Centura Wealth Advisory is an SEC-registered Investment Advisor with its principal place of business in San Diego, California. Centura and its representatives are in compliance with the current registration and notice filing requirements imposed on SEC-registered investment advisors in which Centura maintains clients. Centura may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Past performance is no guarantee of future results. Tax relief varies based on clients’ circumstances, and all clients do not achieve the same results.

https://centurawealth.com/wp-content/uploads/2025/02/Ep-95-Understanding-Alternative-Investments.jpg13922155Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2024-05-01 01:06:002025-07-06 21:37:17Ep. 95 Understanding Alternative Investments: Why You Should Look Beyond Stocks and Bonds

For high-net-worth individuals, founder-led business owners, and C-level executives, managing capital gains taxes is a crucial component of wealth preservation. In this episode of Live Life Liberated, Centura Wealth Advisory’s Managing Director, Derek Myron, speaks with Adam Buchwalter, Partner at Wilson Elser, about the intricacies of state-level capital gains taxes and strategies to mitigate them. Listen to the full episode here:

The Challenge: High State Capital Gains Taxes

Some states, like California, New York, and New Jersey, impose significant capital gains taxes—reaching up to 14.4% in California. Meanwhile, there are eight states with zero capital gains tax, including Alaska, Florida, Nevada, South Dakota, Texas, and Wyoming.

“For state tax to be imposed, there has to be nexus to the state. That’s where tax planning becomes an opportunity.” — Adam Buchwalter

So how can individuals in high-tax states legally reduce or eliminate their capital gains taxes? Adam and Derek dive into key strategies.

Strategy 1: Setting Up a Non-Grantor Trust

One of the most effective ways to mitigate state capital gains taxes is by setting up a non-grantor trust in a tax-friendly jurisdiction.

A non-grantor trust is its own tax-paying entity, domiciled in a state with no capital gains tax.

The trust, rather than the individual, sells the asset, eliminating state-level taxation.

Popular states for these trusts include Nevada, South Dakota, and Delaware.

“Conceptually, if a trust is set up in Nevada and sells the asset, there simply should be no state income tax.” — Adam Buchwalter

Strategy 2: ING Trusts—And Why They No Longer Work in Some States

Incomplete Non-Grantor (ING) Trusts, including NINGs (Nevada) and DINGs (Delaware), were once a go-to strategy. However, in 2014, New York eliminated ING trust benefits by taxing them as grantor trusts. In 2023, California followed suit with SB 131, making them ineffective for California residents.

“Governor Newsom decided to follow New York’s lead, and as of 2023, California residents can no longer use INGs to avoid state capital gains taxes.” — Adam Buchwalter

For individuals already holding assets in ING trusts in these states, options include:

Converting the trust into a completed gift non-grantor trust.

Using the assets to fund private placement life insurance (PPLI).

Relocating to a tax-friendly state before liquidation.

Strategy 3: The QTIP Trust Approach

For married couples, a Qualified Terminable Interest Property (QTIP) Trust presents another viable option. This structure allows one spouse to transfer assets into a trust that benefits the other spouse, effectively shielding capital gains from state taxation.

The trust must be structured as a non-grantor trust.

Capital gains allocated to principal remain untaxed at the state level.

The income generated must be distributed to the spouse, subject to state tax.

“With a QTIP trust, the capital gains portion stays in the trust and remains state tax-free, while income is distributed to the spouse.” — Adam Buchwalter

Key Considerations for Capital Gains Planning

While these strategies offer significant tax-saving potential, they require careful execution.

Trustee Selection Matters: The trustee must reside in a tax-friendly state.

Opinion Letters for Protection: A legal tax opinion can help defend against state audits and eliminate penalties in case of disputes.

“Having an opinion letter from a top law firm can provide protection against penalties in the event of an audit.” — Derek Myron

Final Thoughts: Act Before the Exit

The best tax planning happens before a liquidity event. Business owners planning a sale or individuals with highly appreciated assets should explore options early.

“Anyone with a business, a stock portfolio, or other highly appreciated assets in high-tax states should consider these strategies before their exit.” — Adam Buchwalter

Contact Information

Adam Buchwalter – Partner, Wilson Elser 📞 (973) 735-5784 | ✉️ [email protected]

The information covered and posted represents the views and opinions of the guest and does not necessarily represent the views or opinions of Centura Wealth Advisory. The content has been made available for informational and educational purposes only and is not intended to be a substitute for professional investing advice. Always seek the advice of your financial advisor or other qualified financial service provider with any questions regarding your investment planning.

Centura Wealth Advisory (Centura) is an SEC-registered Investment Advisor with its principal place of business in San Diego, California. Centura and its representatives comply with current registration and notice filing requirements imposed on SEC-registered investment advisors in states where Centura maintains clients. Centura may only transact business in states where it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Past performance is no guarantee of future results. Tax relief varies based on clients’ circumstances, and all clients do not achieve the same results.

https://centurawealth.com/wp-content/uploads/2025/03/Ep-94-How-to-Lower-Your-Capital-Gains-Taxes.jpg14991999Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2024-04-17 02:19:002025-07-06 21:36:51Ep. 94 How to Lower Your Capital Gains Taxes with Adam Buchwalter

After experiencing zero in 2023, the S&P 500 took more than two years before making a new all-time high. Fast forward to the end of the first quarter, witnessing the S&P 500 march its way to 22 new all-time high levels, on pace for the most ever. While much uncertainty surrounding monetary policy still exists, the equity markets brushed off the noise, experiencing minimal volatility. The quarter’s maximum S&P 500 drawdown of -1.7% would mark the smallest drawdown in history if the year ended as of March 31. Even gold and Japan’s stock market joined the all-time highs party, with the latter doing so for the first time since 1989.

Unlike recent quarters, chinks in the armor of the Magnificent 7 appeared to form, as three of the seven constituents (Apple, Alphabet, and Tesla) failed to outpace the broad index return of 10.8%. Ten of the eleven S&P sectors turned in a positive return. On the other hand, Nvidia continued its AI-fueled meteoric ride on way to a Q1 return of more than 82%, and we witnessed a reawakening of the meme stock mania as traders poured into the Reddit Inc., Trump Media, and Technology IPOs.

A year removed from the collapse of Silicon Valley Bank, we were reminded of the stress that higher rates have applied to the balance sheets of small and regional banks. New York Community Bank reported surprise losses on their multifamily commercial real estate loan portfolio, reminding investors that there could still be another shoe to drop. Regional banks tend to have a very large percentage of commercial real estate loans on their books, with many experiencing a high number of defaults, though the market quickly shrugged off the news and risks.

Highlighted last quarter, we felt the bond market got ahead of itself and overpriced the timing and magnitude of Fed rate cuts. Entering 2024, the market anticipated the U.S. central bank would cut six times, resulting in a projected 1.50% (150 basis points) in rate reductions, starting as early as March. As the market reassessed the Fed’s rhetoric and repriced their expectations, market yields for longer dated bonds rose sharply by 0.46% before the 10-Year U.S. Treasury rate settled and ultimately ended the quarter at 4.20%.

Market Recap

Equities – 2023 witnessed a positive correlation between yields on longer dated bonds and equity prices, which resulted in higher equity levels as yields fell and downward pressure as yields rose. This was particularly highlighted over the final two months of 2023, when the yield on the 10-Year U.S. Treasury fell from nearly 5% to 3.88% and ignited the ‘everything rally.’ The largest benefactors were asset classes like small caps and technology, which tend to be the most sensitive to higher interest rates. In contrast to last year, 2024 has seen a significant decoupling of the relationship between equities and bond yields. Fueled by AI-driven enthusiasm, expectations of Fed cuts, and unexpectedly robust earnings, the S&P 500 surged 10.8% for the quarter. This performance marks the best first quarter for the U.S. large-cap index since 2019, delivering consecutive quarters of double-digit returns.

Conversely, higher yields continue to plague smaller companies with today’s higher cost of debt marring their outlook. As the market reassessed monetary policy and rates rose in the first quarter, the small-cap Russell 2000 index experienced turbulence to start the year, but ultimately eked out a 5.18% YTD return.

With a ‘soft landing’ to ‘no landing’ all but expected, the market appears to have accepted the Fed’s latest projections and are closely observing economic data for signals the Fed has the green light to lower rates. As important indicators surrounding inflation, jobs, and overall economic health flood the market, we expect the market to continue reacting counterintuitively to good news, treating it as bad news, while reacting to bad news as though it is good news. Should core inflation remain sticky and economic data remain strong, we would not be surprised to see volatility return as investors start to extend expectations surrounding a June Fed pivot.

Bonds – As yields reversed course, bonds kicked off 2024 adding to their multi-year downward trend. With stronger-than-expected economic data and Fed uncertainty, the market repriced Fed expectations and the yield on the 10-Year U.S. Treasury shot from 3.88% to as high as 4.34% in mid-March. While the market has appeared to reprice monetary policy changes, robust U.S. debt issuance and the demand for U.S. Treasury securities continues to wane, failing to absorb supply and applying upward pressure on yields, exemplified by the Bloomberg U.S. Aggregate Bond Index falling 0.78% over the quarter.

Source: YCharts. The Bloomberg US Aggregate Index was used as a proxy for Bonds; the Bloomberg US High Yield 2% Issuer Capped Index was used as a proxy for High Yield Bonds; the Russell 2000 Index was used as a proxy for Small Cap Equities; and the MSCI ACWI Ex USA Index was used as a proxy for Foreign Equities.

With stronger economic data, base case expectations call for the Fed successfully achieving a ‘soft landing’ and avoiding recession. However, as data has continued to surprise to the upside, many growth metrics continue moderating.

Economy: The Consumer starts slowing

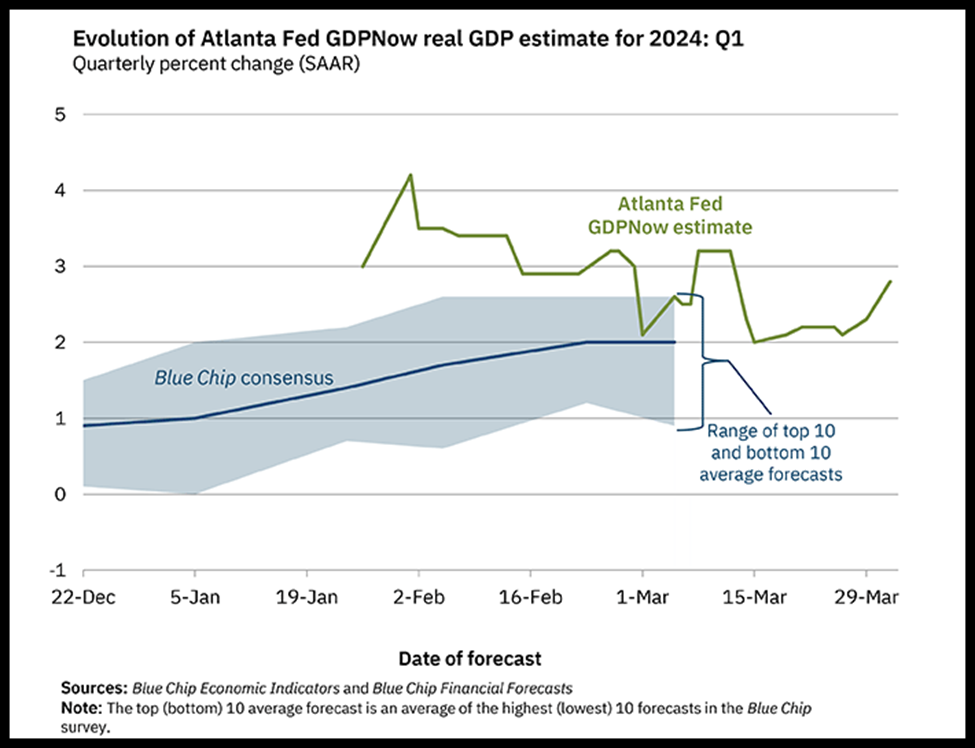

After avoiding the widely anticipated recession of 2023, and growing approximately 2.5%, the U.S. economy continues to grind higher at a moderate pace. As of March 29, 2024, the Atlanta ‘Fed’s GDPNow model for the first quarter is projecting growth of 2.3%, with the largest contribution expected to come from consumer spending, once again, and net exports expected to detract from growth.

Despite higher borrowing costs, the U.S. continues to outperform its global peers, largely due to a stable labor market that has consistently produced wage increases outpacing inflation for 10 consecutive months, through February. March’s labor report is due Friday, April 5 and wages are expected to continue to outpace pricing pressures for an 11th straight month, further supporting consumers’ ability to spend.

Unemployment

February’s Labor Market Report registered the 38th consecutive month of job gains. Estimates called for 198,000 jobs in February, and the market surprised to the upside with the addition of 275,000 jobs, though unemployment jumped 0.2% to 3.9%.

February’s unemployment rate also marked the 27th consecutive month unemployment has held below 4%, which is the longest streak since the 1960s. The labor market continues to post robust results. While trending lower since peaking in 2022, job openings (JOLTs) have been a mixed bag from month-to-month, and still remain elevated at 8.86 million. This brings the ratio of job openings to those unemployed to 1.371. While the ratio of 1.37:1 is still considered elevated above levels historically witnessed, the ratio has fallen significantly from nearly two job openings for every job posting in 2022. This indicates slack is working itself out of the system and the labor market is showing signs of tightening. The number of open jobs has fallen, while the number of unemployed job seekers has trended higher, as evidenced by the additional 334,000 unemployed persons from January to February.

For now, the strength and resiliency of the labor market has given the Fed the confidence to keep rates higher for longer. However, sticky wage growth continues to give the Fed anxiety, as this metric has been effectively stuck around 4.3% since October 2023. While persistent and elevated wage growth brings fears of an inflation resurgence, any break below the 4% threshold would temper those fears and be well received by the Fed.

Inflation

The Fed appears to be winning their battle against inflation, as pricing pressures look to be tamed and headed towards the Fed’s 2% target – though it is still too early for the Fed to declare their victory lap. On the surface, all major inflation readings reside below 4%, with both PCE readings printing below 3% over the last year, through February.

Shelter and gasoline represented approximately 60% of the monthly gain in Headline CPI in February, with additional pricing pressure from used cars, apparel, motor vehicle insurance, and airfares at the highest levels since May 2022. Boeing woes are forcing airlines to cut their flight capacity and we expect further pricing pressure on air travel over the next several months. Additionally, we anticipate continued upward pressure on energy prices, leading to volatility on the headline CPI numbers as we progress through the summer months.

Just as elevated wage growth remains troublesome to the Fed, the stickiness of core services, particularly shelter costs, supports their decision to exercise patience before cutting rates. The rolling three-month core CPI is running at an annualized rate of 4.2%, which is the highest since June 2023.

Too Soon to Pivot

Defying market expectations of a March rate cut, the Fed met twice in the first quarter and left rates unchanged, illustrating their unflagging commitment to bring inflation back to its long-term target of 2%. Since initiating rate increases in March 2022, the Fed raised rates eleven times, bringing the target range for the Fed Funds rate to the current range of 5.25% to 5.50%. During this period, Fed Chair Jerome Powell has also been reducing the Fed’s balance sheet by $95 billion per month, resulting in a decrease in assets of nearly 16.5%, or approximately $1.48 trillion, since its peak in April 2022.

The Federal Open Market Committee (FOMC) elected to keep rates unchanged in March for the fifth consecutive meeting. While the Fed’s decision was largely expected, the big news was the Fed’s changes, or lack thereof, to their Summary of Economic Projections. Of particular interest was their median projection for rate cuts, which policymakers held unchanged at three cuts in 2024. Only two Fed officials projected no cuts in 2024, while two anticipated only two cuts. Only one member voted in favor of more than three rate cuts in 2024, signifying a stark contrast to the Fed’s December 2023 projections where five members anticipated more than three cuts in 2024. We also saw the Fed lift economic projections, like GDP, for 2024, while also increasing their 2024 inflation expectations and revising their 2025 path of rate normalization.

Powell recognized that inflation has been stickier than anticipated the last couple of months, though the latest data “haven’t really changed the overall story, which is that of inflation moving down gradually on a sometimes-bumpy road towards 2%.” He further reiterated “we’re not going to overact…to these two months of data, nor are we going to ignore them.”

Barring any resurgence of inflation, we believe the Fed has finished its rate-hiking campaign and are nearing their first rate cut. Given the Fed’s steadfast commitment to bringing inflation down, our base case assumptions from the last several quarters have not changed. We continue to believe the earliest the Fed will cut rates is June, which now aligns with current market expectations. However, any prolonged stickiness or resurgence of inflation would likely push our expectations for rate cuts into the third quarter of this year.

Centura’s Outlook

The Fed’s goal to lower inflation back to its 2% mandate and avoid recession is now the base outcome expected by the Fed and most market participants. The successful delivery of lower inflation and Fed policy normalization should bode well for both equities and bonds. However, we continue to believe the market appears priced to perfection, and investors should proceed with caution as any resurgence or sustained stickiness of inflation could result in monetary policy uncertainty and lead to bouts of market angst or volatility.

In the face of higher borrowing costs, corporate profits have remained surprisingly resilient as the S&P 500 posted positive earnings growth for the second consecutive quarter in the fourth quarter of 2023, rising 4.2%. Interestingly, those companies with more than 50% of their revenue generated outside of the U.S., generated better profits than companies generating most of their profits domestically. As margins continue to face pressure, FactSet has witnessed revisions for first quarter earnings, dropping from 5.8% on December 31 to 3.6% as of March 28.

Forward 12-month P/E ratios are approximately 20.9x, above both their five-year and ten-year averages of 19.1x and 17.7x, respectively. This indicates that equities are slightly overvalued and thus priced to perfection. For further confirmation, the earnings yield relative to the yield on the 10-Year U.S. Treasury also indicates that equities are relatively valued today, as the S&P 500 earnings yield (Earnings/Price) is 4.30%, compared to the yield of on the 10-Year U.S. Treasury of 4.33% as of April 1.

The market remains too dependent on the Fed, which has become dependent on poor economic data; with worsening conditions, the more likely the Fed is to pivot and cut rates sooner. However, we believe economic activity will continue to surprise to the upside, realistically extending the timing of the widely anticipated rate cut. Should expectations shift from June to later in the year, we would expect markets to react negatively, and volatility would ensue.

We entered the year with our allocations aligned with our long-term targets. While higher rates will continue to cause issues for some companies, earnings are expected to grow from 2023 levels in 2024. While equities generally produce a positive return during election years, we expect volatility will likely increase as we approach the election in the third and fourth quarters. However, the improving market breadth, as evidenced by the roughly 70% of S&P 500 companies trading above their 200-day moving averages, gives us optimism that markets should continue to grind higher. Outside of Fed policy-related market volatility, we are more fearful of potential exogenous events that are harder to predict.

As expected, yields rose to start the year as the market repriced its expectations surrounding Fed rate cuts. When yields reversed higher, we took the opportunity to further extend the duration of our fixed income allocations. While the path may be bumpy, ultimately, we believe yields should continue to grind lower over the course of the year, presenting attractive opportunities to produce asymmetric returns in bonds. Extending duration should allow investors to clip an attractive yield, while also providing them with the opportunity to experience capital appreciation for a total return exceeding what they will clip sitting in money market funds or short-term Treasury bills.

Elevated interest rates continue to punish private real estate returns, with further slight downward valuation adjustments expected from their previous marks. Real estate is an interest rate-sensitive asset class, meaning as rates move lower, we anticipate a pick-up in activity, and a subsequent reversal of valuations over the next several years. While we believe we are nearing the light at the end of the tunnel for several real estate sectors like multifamily and industrial, unfortunately, we believe more pain will be experienced, particularly with the underlying debt that real estate operators hold. There is a reason S&P Global just downgraded five regional banks based on their commercial real estate loan exposure. Like S&P Global, we anticipate a pickup in defaults across several real estate sectors, which will likely result in further pain across both public and private markets.

Private credit presents an opportunity to earn attractive returns, given private credit is predominantly floating and tied to a base rate such as the Secured Overnight Financing Rate (SOFR), closely linked to the Fed Funds overnight rate. Yields on private credit should remain at their current levels until the Fed begins to cut rates. Even as the Fed cuts rates, the floating rate on private loans does not adjust immediately. Rather, there is a delay before the loan terms reset lower, typically every three months. Barring a catastrophic event, the Fed is likely to lower rates more methodically than they hiked them, supporting higher yields in private credit. Fortunately, private companies have weathered the elevated rate storm better than anticipated. As Cliffwater recently shared with us, borrowers demonstrated strong performance, as evidenced by the 15% year-over-year revenue growth and 13% EBITDA growth. Lower rates should support improved health of borrowers and support attractive returns, relative to traditional fixed income going forward. Combining traditional bonds with private credit should produce a balanced and diversified approach toward income production and total return in 2024.

Thank you for your continued confidence and support. If you have questions or concerns, please contact your Centura Wealth advisor.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on the market and other conditions. These documents may contain certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information, and it should not be relied on as such.

Centura Wealth Advisory is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Centura Wealth Advisory and its representatives are properly licensed or exempt from licensure. 12255 El Camino Real, St. 125, San Diego, CA 92130.

https://centurawealth.com/wp-content/uploads/2024/07/Market-wrap-2024-q2-scaled.jpg9872560Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2024-04-04 07:58:002025-04-08 16:27:35Q1 2024 Market Wrap: Equities Keep the Good Times Rolling

Unlocking Exponential Results with Centura Wealth Advisory

Navigating wealth management as an ultra-high-net-worth individual requires a sophisticated, proactive approach that delivers exponential financial results. Centura Wealth Advisory’s Liberated Wealth® Process is a five-step, structured journey designed to help founder-led business owners, C-level executives, and other high-net-worth individuals optimize their financial strategies while preserving and growing their wealth.

In this episode of Live Life Liberated, Sean Clark sits down with Derek Myron, founder, CEO, and managing director of Centura, to discuss how this proprietary process provides clarity, efficiency, and exponential value for clients.

The Five-Step Liberated Wealth® Process

1. Uncover: Discovery Phase

The journey begins with an in-depth discovery process that gathers facts, assumptions, and client goals. The focus is on understanding a client’s financial landscape, objectives, and pain points to build a customized strategy.

“People can see very early in the process—month 2, 3, or 4—that this will yield fantastic results for them and their family.” — Derek Myron

2. Unlock: Identifying Strategic Opportunities

Once the discovery phase is complete, Centura identifies key planning solutions categorized into four areas:

Identified Strategies – Ranked in priority order

Work in Progress – Strategies under consideration

Completed Strategies – Implemented solutions

Disqualified Strategies – Solutions that do not apply

At this stage, clients are introduced to a collaborative team of CPAs, estate planning attorneys, and other professionals to refine and validate these strategies.

3. Design: Blueprint for Financial Success

The third step involves modeling out the identified strategies and integrating them into a cohesive plan. Each strategy is evaluated for:

Potential tax savings

Cost of implementation

Long-term financial impact

Associated risks

With a clear blueprint in place, Centura coordinates with professionals to ensure alignment before moving forward.

“The planning now dictates the investments.” — Derek Myron

4. Liberate: Implementing the Plan

With a strategy finalized, Centura facilitates the execution of tax, estate, and investment strategies. This phase ensures seamless implementation and eliminates inefficiencies, allowing clients to experience white-glove service at every step.

5. Stewardship: Ongoing Review and Optimization

The process doesn’t end with implementation. Centura provides ongoing stewardship, including:

Annual report cards tracking financial benefits

Adjustments based on tax law changes

Coordination with legal and financial teams for continued optimization

“Clients get a structured report card showing the exponential value created, ensuring transparency and accountability.” — Sean Clark

Who Benefits from the Liberated Wealth® Process?

The process is tailored for:

Founder-led business owners with $20M+ equity anticipating a liquidity event

C-level executives with $2M+ annual income and $20M+ net worth

Individuals seeking immediate solutions to complex financial challenges

Collaboration with Elite Advisors

Centura’s Elite Advisor Collaboration Program (EACP) ensures top-tier financial professionals work together to deliver holistic wealth management solutions. Unlike traditional models where advisors work in silos, Centura fosters a transparent, highly coordinated approach that benefits both clients and advisors.