How Can High-Income Business Owners Supercharge Their Retirement Savings?

Business owners with significant surplus cash flow often seek ways to maximize their retirement savings while minimizing tax burdens. Traditional retirement plans like 401(k)s and SEP IRAs offer tax deferral, but they come with contribution limits that may not fully utilize the financial potential of high-income earners.

However, there is a solution: Defined Benefit Plans designed specifically for high-earning business owners. In this episode of the Live Life Liberated podcast, Centura Wealth Advisory’s Sean Clark, Wealth Advisor, and Christopher Hyman, Director of Insurance Solutions, discuss how these plans work, their benefits, and key considerations for implementation.

What Are Defined Benefit Plans?

Defined Benefit Plans differ from Defined Contribution Plans (such as 401(k)s) in that they establish a set benefit to be received in the future, rather than limiting contributions based on annual IRS limits. This allows for significantly larger contributions—potentially millions of dollars per year—providing a powerful tax deferral strategy for business owners.

Key Benefits of Defined Benefit Plans

Higher Contribution Limits – Unlike a 401(k) or SEP IRA, Defined Benefit Plans allow business owners to set aside significantly more pre-tax income for retirement.

Tax Efficiency – Contributions reduce taxable income in the current year, providing immediate tax relief while deferring income taxation until retirement.

Customization – Plans can be tailored to suit the needs of business owners and select employees.

Life Insurance Integration – Incorporating life insurance into the plan structure can enhance tax advantages and provide additional security.

Who Benefits Most from Defined Benefit Plans?

These plans are best suited for:

Business owners with annual incomes exceeding $2 million.

Companies with a small, select group of highly compensated employees.

Business owners looking to maximize retirement contributions before an upcoming business sale.

Individuals interested in deferring large sums of income for tax planning purposes.

How Does the Process Work?

1. Plan Design & Setup

The process begins with an actuarial analysis to determine contribution limits based on business financials and employee census data. The plan is then structured to maximize benefits for the owner and selected employees.

2. Maintenance & Ongoing Contributions

Each year, contributions must align with the plan’s funding range, ensuring compliance while optimizing tax benefits. Investment strategies are designed to manage risk and align with plan liabilities.

3. Plan Termination & Rollout

When a business is sold or the owner transitions to retirement, the plan is rolled out to individual IRAs, allowing continued tax-deferred growth. If structured correctly, the plan can avoid excise taxes on overfunding and provide additional financial flexibility.

Why Consider Life Insurance in a Defined Benefit Plan?

Increases Contribution Limits – The IRS permits higher contributions when life insurance is part of the plan.

Provides a Discounted Payout – The policy can often be distributed at a fraction of its actual value, creating additional tax efficiencies.

Offers an Additional Retirement Asset – Policies can be converted into tax-free income sources upon distribution.

Final Thoughts

For high-income business owners, a Defined Benefit Plan offers an opportunity to significantly increase retirement savings, optimize tax planning, and enhance long-term financial security. However, these plans require careful structuring and ongoing management to ensure compliance and maximize benefits.

If you’re a business owner with surplus cash flow and looking for ways to supercharge your retirement savings, reach out to Centura Wealth Advisory to explore how a Defined Benefit Plan might work for you.

Disclaimer

The information covered in this blog represents the views and opinions of the speakers and does not necessarily reflect the views of Centura Wealth Advisory. This content is for informational and educational purposes only and is not intended as financial, tax, or investment advice. Always consult with a qualified financial professional before making any investment decisions.

https://centurawealth.com/wp-content/uploads/2025/03/Ep-92-How-Can-High-Income-Business-Owners-Supercharge-Their-Retirement-Savings.jpg14122122Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2024-03-20 09:00:002025-04-08 16:43:27Ep. 92 How High-Income Business Owners Can Supercharge Their Retirement Savings

Life insurance is often viewed as a way to provide a death benefit. However, for high-net-worth individuals and business owners, life insurance can serve as a strategic financial tool for tax planning, and wealth transfer, and even as an alternative investment.

In this episode of the Live Life Liberated podcast, Centura Wealth Advisory’s Sean Clark, Wealth Advisor, and Christopher Hyman, Director of Insurance Solutions, discuss the broader applications of life insurance.

Key Takeaways

1. Life Insurance as a Wealth Transfer Tool

For high-net-worth individuals, estate taxes can pose a significant burden, often requiring liquidity that may not be readily available. Life insurance provides a tax-free death benefit that can be used to offset estate taxes, preventing the forced liquidation of valuable assets such as real estate or business holdings.

“Wealthy individuals utilize life insurance as a tool to offset tax liability. It provides liquidity at a critical moment, allowing beneficiaries to maintain ownership and control over assets.” – Christopher Hyman

2. Life Insurance as an Alternative Asset Class

Beyond its traditional role, life insurance can serve as a tax-efficient investment vehicle. Certain policies allow for cash accumulation with tax-deferred growth and tax-free withdrawals, making it a compelling option for individuals looking to diversify their portfolio.

“In some cases, we design policies with minimal death benefits to maximize cash accumulation, creating a tax-efficient investment vehicle.” – Sean Clark

3. Business Owners and Life Insurance Planning

Business owners face unique challenges, from succession planning to risk management. Life insurance can be leveraged in several ways:

Key Person Insurance: Protects businesses from financial loss in case of the death of a crucial team member.

Buy-Sell Agreements: Ensures a smooth ownership transition if a business partner passes away.

Defined Benefit Plans: Helps business owners maximize pre-tax retirement savings.

“A buy-sell agreement funded with life insurance ensures that business shares transition smoothly, protecting the company and the remaining owners.” – Christopher Hyman

4. Tax Advantages of Life Insurance

Life insurance offers several tax benefits:

Tax-deferred growth of policy cash value

Tax-free withdrawals up to the basis amount

Policy loans that do not trigger taxable income

Tax-free death benefits for beneficiaries

“There are four key tax advantages to life insurance: tax-deferred growth, tax-free withdrawals, tax-free loans, and a tax-free death benefit. When structured correctly, it’s a powerful tool for wealth preservation.” – Sean Clark

By strategically incorporating life insurance into a financial plan, individuals can optimize tax efficiency while securing financial stability for their heirs.

5. Exit Planning and Life Insurance

For business owners preparing for a sale or transition, life insurance strategies like Private Placement Life Insurance (PPLI) can enhance the efficiency of wealth transfer and minimize tax liability.

“PPLI provides a tax-efficient wrapper for tax-inefficient assets, making it a smart choice for business owners planning an exit.” – Sean Clark

Final Thoughts

While life insurance is often overlooked beyond its traditional death benefit use, it remains a powerful tool in financial and estate planning. By integrating life insurance into a comprehensive wealth strategy, high-net-worth individuals and business owners can mitigate risks, enhance liquidity, and optimize tax outcomes.

The information covered and posted represents the views and opinions of the guest and does not necessarily represent the views or opinions of Centura Wealth Advisory. The content has been made available for informational and educational purposes only. The content is not intended to be a substitute for professional investing advice. Always seek the advice of your financial advisor or other qualified financial service provider with any questions you may have regarding your investment planning.

Centura Wealth Advisory (Centura) is an SEC-registered investment advisor with its principal place of business in San Diego, California. Centura and its representatives are in compliance with the current registration and notice filing requirements imposed on SEC-registered investment advisors in which Centura maintains clients. Centura may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Past performance is no guarantee of future results. Tax relief varies based on client circumstances, and all clients do not achieve the same results.

https://centurawealth.com/wp-content/uploads/2025/03/Ep-91-Effective-Use-Cases-of-Life-Insurance-for-Wealth-Transfer-scaled.jpg17072560Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2024-02-14 20:42:002025-06-29 22:37:05Ep. 91 Effective Use Cases of Life Insurance for Wealth Transfer, Tax Planning, and More

In 2017, the Tax Cuts and Jobs Act (TCJA) introduced major changes to income and estate tax laws, offering tax cuts and adjustments that have shaped financial planning for high-net-worth individuals and business owners. However, these provisions are set to expire on December 31, 2025, which could result in higher tax rates and reduced exemptions.

In this episode of Live Life Liberated, Matt Griffith, CFP®, and Roby Kotcamp, CFP®, discuss what these changes mean and how individuals and businesses can prepare for the transition

Key Takeaways on the TCJA Sunset

1. What Happens When the TCJA Expires?

The expiration of the TCJA means a return to pre-2017 tax laws, leading to higher tax rates and reduced deductions for many taxpayers. Congress has the power to modify or extend certain provisions, but as of now, the law is set to sunset automatically.

“The reality is, if we want to continue spending at the current level, we will need to raise revenue. Higher tax rates are almost inevitable.” – Roby Kotcamp

2. Income Tax Rate Increases

If the TCJA expires as planned, most income tax brackets will increase by an average of 9.4%, affecting high earners the most. Notably:

The top income tax bracket will rise from 37% to 39.6%

The 22% bracket will jump to 25%, and the 24% bracket will increase to 28%

The qualified business income (QBI) deduction—a crucial benefit for pass-through entities—will be eliminated

“High-income earners could see an 8-9% increase in their tax bill. If you’re already paying $2 million in taxes, that’s not small change.” – Matt Griffith

3. Estate and Gift Tax Exemptions Will Be Cut in Half

For those with significant wealth, one of the most impactful changes will be the reduction of the estate and gift tax exemption.

In 2024, the exemption is approximately $27 million for married couples

After the sunset, it will drop to around $13.5 million for couples and $6.75 million for individuals

The estate tax rate will remain at 40%, making proactive planning essential

“If your net worth is between $7 million and $25 million, you may think estate taxes don’t affect you—but in 2026, they will.” – Roby Kotcamp

4. Tax Planning Strategies Before 2026

With just under two years before the changes take effect, now is the time to implement strategies to minimize tax exposure.

Income Tax Planning:

Consider accelerating income before 2026 while rates are lower

Plan for deductions and credits that will be phased out

Optimize qualified business income (QBI) deductions while available

Estate and Gift Tax Strategies:

Use irrevocable trusts, such as spousal lifetime access trusts (SLATs)

Leverage charitable lead trusts (CLTs) and qualified personal residence trusts (QPRTs)

Strategically gift assets now to lock in the current exemption levels

5. Why You Should Act Now

Waiting until 2025 to take action could lead to missed opportunities. By then, estate attorneys and tax professionals will be overwhelmed with last-minute planning requests.

“If you wait until 2025, estate planning attorneys may be fully booked. The best time to act is now.” – Matt Griffith

Final Thoughts

The sunset of the TCJA will bring sweeping tax changes that could significantly impact high-net-worth individuals and business owners. Whether it’s planning for higher income tax rates, estate tax implications, or taking advantage of the current tax code, proactive planning is crucial.

To discuss how these changes affect your financial strategy, contact Matt Griffith at [email protected] or Roby Kotcamp at [email protected].

Disclaimer

The information covered and posted represents the views and opinions of the guest and does not necessarily represent the views or opinions of Centura Wealth Advisory. The content has been made available for informational and educational purposes only. The content is not intended to be a substitute for professional investing advice. Always seek the advice of your financial advisor or other qualified financial service provider with any questions you may have regarding your investment planning.

Centura Wealth Advisory (Centura) is an SEC-registered investment advisor with its principal place of business in San Diego, California. Centura and its representatives are in compliance with the current registration and notice filing requirements imposed on SEC-registered investment advisors in which Centura maintains clients. Centura may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Past performance is no guarantee of future results. Tax relief varies based on client circumstances, and all clients do not achieve the same results.

https://centurawealth.com/wp-content/uploads/2025/03/Ep-90-TCJA.jpg14102127Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2024-01-10 21:20:002025-04-08 16:16:42Ep. 90 Tax Countdown: Planning for the Expiration of the TCJA

With so much uncertainty surrounding the Fed’s monetary policy and the contagious effects their aggressive rate hiking cycle would inflict on the economy, we entered 2023 with great pessimism and uncertainty. Most economists and financial strategists predicted and braced for what they believed was an almost certain recession in the year’s second half. Not only did the U.S. avoid a recession, the first three quarters grew at 2.2%, 2.1%, and 4.9%, respectively, with the Atlanta Fed GDPNow model estimating fourth quarter growth at 2.3%.

Like 2022, the common themes wreaking market havoc in 2023 were linked to the Fed’s monetary policy, resulting market yields, and inflation. While the US economy is showing some signs of softening, the labor market has remained robust. The Fed’s war on inflation appears to have proven successful, as price pressures continue to grind lower towards their 2% target while avoiding a ’hard landing’. Yield volatility resulted in equity market gyrations over the last two years, and in 2023, the equity markets looked past the multiple regional banks collapses, growing geopolitical tensions globally, and several quarters of negative year-over-year earnings growth on their way to recording gains few predicted. Investors were rewarded in 2023 in many ways, including:

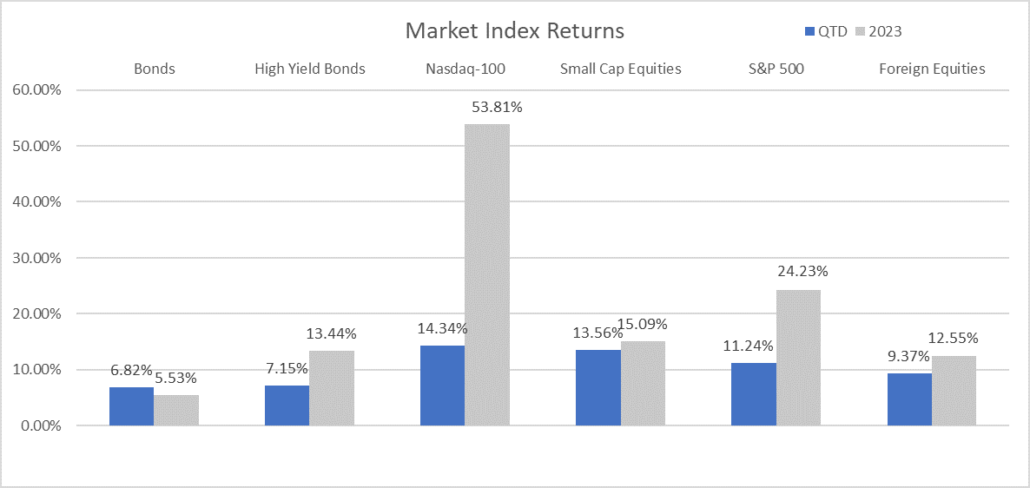

The S&P 500 index surged $8 trillion and closed up 24.23% in 2023, finishing the year on a strong note. Notching nine straight weeks of gains – the longest such streak since 2004, the S&P 500 index closed the year ~0.56% shy of new all-time highs.

The NASDAQ 100 benefitted from the Artificial Intelligence (AI) craze to gain 53.81% for year, the index’s best return since 1999.

The Magnificent Seven, comprised of the seven-largest technology stocks (Apple, Amazon, Alphabet, Microsoft, Meta Platforms, Nvidia, and Tesla), were responsible for approximately 64% of the S&P 500’s 2023 return. Investors flocked to size and profitability and believe the Magnificent 7 companies’ scale and financial flexibility place them in the best position to capitalize on artificial intelligence.

Global stocks, as measured by the MSCI All-Country World Index, struggled to keep pace with their U.S. counterparts, registering gains of 12.59%.

Bloomberg Barclays U.S. Aggregate Bond Index snapped its two-year losing streak. The index advanced 5.53% in 2023, and with yields plummeting over the final two months of the year, global bonds recorded their best two-month surge on record, according to Bloomberg.

Taking the Fed’s rhetoric from December’s meeting and the path of inflation, market participants went all-in, and are now anticipating the Fed is set to pivot in the first quarter of 2024 and cut interest rates significantly over the course of the year. This move would lift asset prices across all major markets, delivering most of the calendar year returns for several indices in November and December. Given the robust rally to close out the year, we keep asking the two primary questions: Have the markets gotten ahead of themselves? And is a recession still on the table for 2024?

Market Recap

Equities – The combination of stronger economic data, U.S. Treasury debt issuance, foreign investor sales of U.S. debt, and Fed uncertainty that plagued equity markets in August and September rolled into the final quarter of 2023, pushing stock and bond returns to correction territory in October. While the index started the quarter declining more than 2% in October, the NASDAQ-100 bounced 16.77% in November and December to produce a fourth-quarter advance of 14.34%. The U.S. Treasury announced their debt issuance would focus on the front end of the yield curve. The labor market showed signs of softening, and the Fed started their dovish posturing. These shifting dynamics forced longer-term bond yields lower from nearly 5% on the 10-Year U.S. Treasury to 3.88%, subsequently igniting the ‘everything rally’ to close out 2023’s final two months. The largest benefactors were those asset classes like small caps and technology, which tend to be the most sensitive to higher interest rates.

Unlike most of the year, the fourth quarter market surge was more broad-based, as evidenced by the average stock, represented by the S&P 500 Equal Weight ETF (RSP), besting the concentrated market-cap weighted S&P 500 with returns of 11.81% and 11.24%, respectively. Lower rates and looser financial conditions boosted the outlook for smaller companies, as the small-cap Russell 2000 index rallied 13.55% amid the fourth quarter collapse in the 10-Year U.S. Treasury yield and nearly produced the entire year’s return for the index in the final two months.

While talk of the most anticipated recession evaporated, and a ‘soft landing’ to ‘no landing’ is all but expected, the market appears to have received the clarity from the Fed they were looking for and have declared the Fed is done raising rates, with rate cuts on deck. Participants continue to react counterintuitively to good news, treating it as bad news, while reacting to bad news as though it is good news. Should core inflation remain sticky and economic data like labor remain strong, we would not be surprised to see volatility ensue as investors start to unwind some of the optimism surrounding a Fed pivot they poured on in late 2023.

Bonds – As yields continued to spike, bonds continued their downward trend, adding to losses accumulated since August 2020. With stronger-than-expected economic data, Fed uncertainty, and robust U.S. debt issuance, the demand for U.S. Treasury securities continued to wane, not absorbing supply and forcing higher yields. The yield on the 10-Year U.S. Treasury started the quarter yielding 4.59% and nearly closed above 5% (4.98%) before plummeting 1.10% to finish the fourth quarter yielding 3.88%. Falling bond yields resulted in strong returns, as the Bloomberg U.S. Aggregate Bond Index increased 6.82% in the quarter, dragging its performance out of negative territory for the year.

Source: YCharts. The Bloomberg US Aggregate Index was used as a proxy for Bonds; the Bloomberg US High Yield 2% Issuer Capped Index was used as a proxy for High Yield Bonds; the Russell 2000 Index was used as a proxy for Small Cap Equities; and the MSCI ACWI Ex USA Index was used as a proxy for Foreign Equities.

With stronger economic data, base case expectations are that the Fed will successfully achieve a ‘soft landing’, avoiding a recession altogether. However, as certain economic data has continued to surprise to the upside, growth metrics are moderating.

Economy: The Consumer is a Rabid Spending Engine

Growing at more than double the pace of the first half of 2023, the final revision to third-quarter GDP growth accelerated to 4.9%, marking the fastest expansion rate since Q4 of 2021. The third quarter GDP reading was characterized by strong consumer spending, exports, and private inventory increases. Consumers are the engine driving us forward, making up roughly two-thirds of the nation’s economic output. Showing signs of abating in Q2, spending only grew 0.8%, with the third quarter witnessing consumers accelerate spending by nearly 4X to 3.1%. While consumer behavior is important to monitor, the acceleration does not appear troublesome to the Fed, as the Atlanta Fed’s GDPNow model for the fourth quarter has been lowered to 2.3%.

Given our nation’s reliance on consumption as a key component of GDP[1], consumer health is important to monitor. Fresh off a strong third quarter spending clip, the consumer has showed little signs of slowing, as indicated by holiday spending. The five-day holiday shopping period encapsulating both Black Friday and Cyber Monday saw record sales of $38 billion, a 7.8% increase over last year. The two retail holidays produced a combined $22.2 billion in sales, representing year-over-year growth of 7.5% and 9.6%, respectively. While strong spending in general is good, how consumers have been spending gives rise for concern.

The post-pandemic, stimulus-infused savings are being exhausted and many consumers are adopting a buy now, pay later (BNPL) mentality and paying on credit. Most credit spending involves floating rates, so while consumers run up their balances, their cost of debt is also rising. Further deterioration in the labor market could spell trouble for the consumer, though for now, falling price pressures and sticky wage growth continue to support the consumers’ appetite for spending.

Inflation & Interest Rates

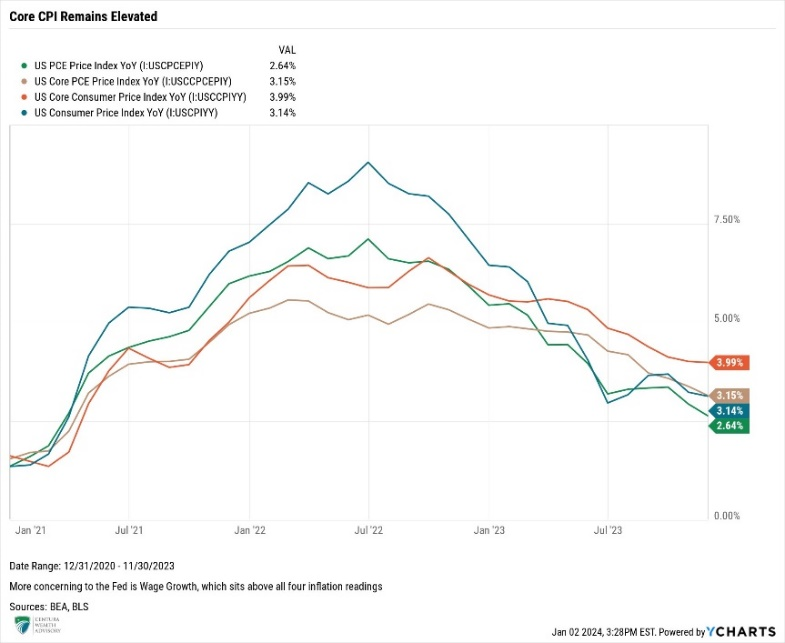

Inflation remains elevated, though the downward trends have been persistent. November’s headline Consumer Price Index (CPI) came in at 3.10%, while core CPI (excluding energy and food) remained stuck at the 4% year-over-year threshold for the second consecutive month. The once-persistent pricing pressure on core services, particularly, shelter, appears to have broken lower.

Shelter represents about 1/3 of CPI, making the variable impactful on the overall inflation gauge, as shelter has accounted for nearly 70% of the total increase in core CPI over the past year, according to the Bureau of Labor Statistics. Slightly declining to 6.5% in November from its 8% cycle peak, registered in March of this year, and rents declining nationally, shelter inflation should continue to move lower in 2024.

Adding to the optimism over inflation is the downward pressure on the Fed’s preferred inflation gauge, the Personal Consumption Expenditures (PCE). Entering the year elevated, with the headline PCE and core PCE registering 5.44% and 4.87%, respectively, the Fed’s war on inflation has proven successful. Both metrics have broken through the 4% threshold, with headline breaking below 3%. Through October, headline PCE was 2.64%, while core PCE fell to 3.15%. While the Fed’s actions appear to have been successful, it’s still too early for their victory lap, as wage growth remains above 4%. Wage growth trending above inflation creates the concern that persistence of this trend could result in a wage price spiral, ultimately leading to a resurgence of inflation. For the Fed to feel comfortable inflation will not reverse course, they will want to see both core CPI and wage growth trend below the 4% threshold for multiple readings.

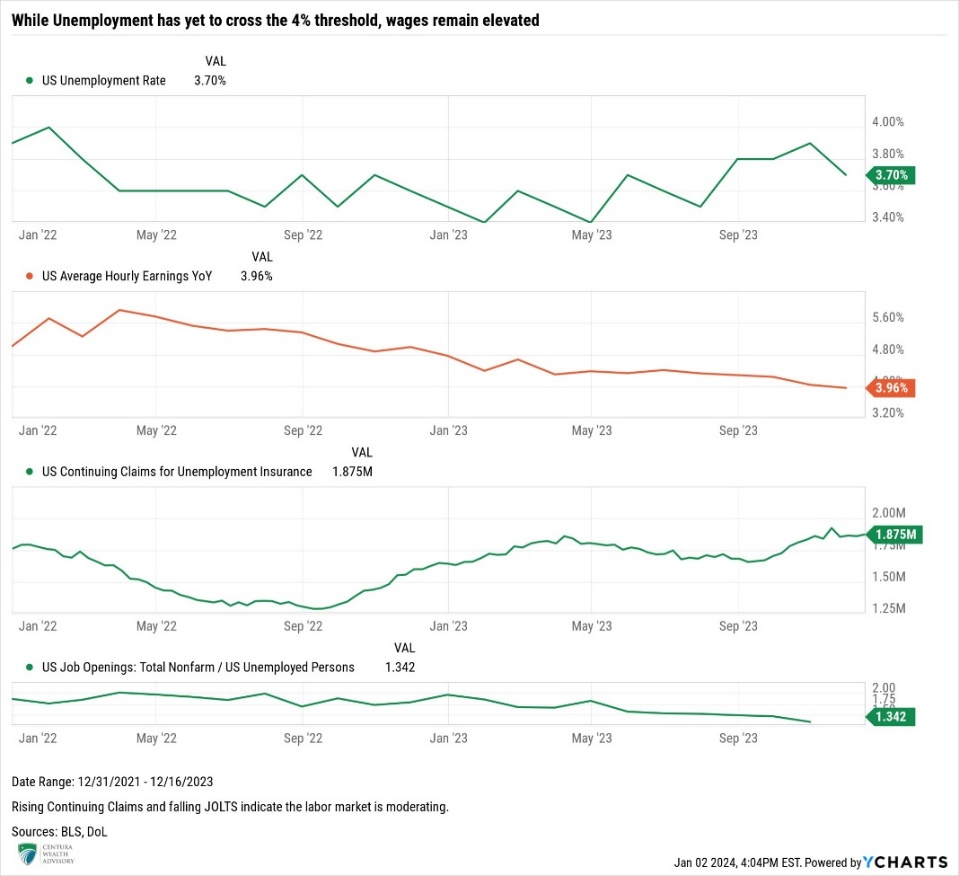

Unemployment

November’s Labor Market Report registered the 35th consecutive month of job gains. Estimates called for 190,000 jobs in November, however the market barely beat to the upside when 199,000 jobs were added and unemployment fell 0.2% to 3.7%. The labor market continues to post strong, albeit moderating, results. Providing comfort was the rebound in the participation rate to 62.8%, matching the post-pandemic high, along with job openings (JOLTs) falling sharply to 8.73 million and bringing the ratio of job openings to those unemployed to 1.34:1. While the ratio of 1.34:1 is still elevated above levels we have historically witnessed, the ratio has fallen significantly from nearly two job openings for every job posting in 2022, indicating that some of the slack is working itself out of the system and the labor market is showing signs of tightening. While unemployment claims are at extraordinarily low levels, the upward trend in Continuing Claims continues to point towards labor softening. The metric reached the highest level since late-2021, indicating out of work Americans are finding it more difficult to secure new employment, which could have a hand in slowing consumer spending.

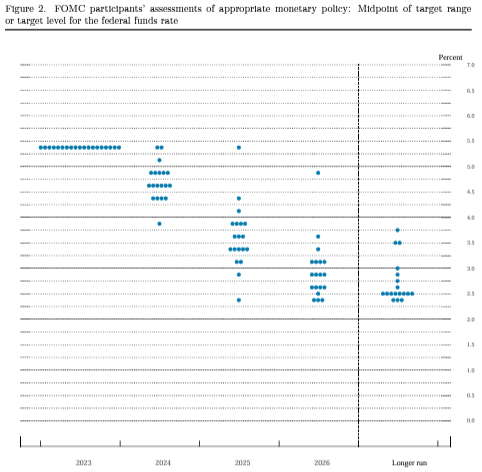

Time to Pivot?

The Fed has remained resolute in bringing inflation back to its long-term target of 2%. Since March 2022, the Fed has raised rates eleven times, bringing the target range for the Fed Funds rate to 5.25% to 5.50%. During this period, Fed Chairman Jerome Powell has also been reducing the Fed balance sheet by ~$95 billion per month, shedding nearly 14%, or approximately $1.25 trillion, since peaking in April 2022 at $8.965 trillion.

As anticipated, the Federal Open Market Committee (FOMC) elected to keep rates unchanged in December for the third consecutive meeting. While the Fed’s decision was largely expected, their dovish commentary surprised investors. With moderating jobs data and promising inflation figures likely supporting their tone, the Fed indicated their efforts to dampen 40-year high inflation are proving successful, stating growth has slowed and “inflation has eased over the past year but remains elevated.”

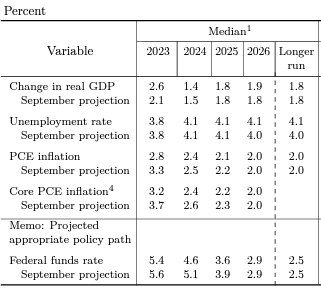

December’s meeting also saw a reversal in the Fed’s future projections. Deviating from their September estimates, the Fed is now projecting 0.75% of rate cuts up from 0.50%, with another 1% of estimated cuts in 2025, which would bring the Fed Funds Target rate to 3.6% by the end of 2025. The FOMC further slashed their inflation estimates from 2.6% to 2.4%. In his post-announcement press conference, Chairman Powell all but declared the Fed is done hiking rates in this tightening cycle,

“We believe that our policy rate is likely at or near its peak for this tightening cycle; the economy has surprised forecasters in many ways since the pandemic.”

While recognizing the lagged effects of monetary policy on the economy, the Fed did leave the door open for additional rate hikes. However, the insertion of the word “any” in the following statement, “any additional policy firming that may be appropriate” to rein in inflation, sent equity markets higher and bond yields lower. In the weeks following the December FOMC meeting, the markets revised their expectations to aggressively price in 1.50% of rate cuts in 2024, beginning as early as March, double what the Fed is currently projecting.

Barring any resurgence of inflation, we believe the Fed has finalized its rate-hiking program. We stop short of saying “tightening cycle” because the Fed is still engaged in Quantitative Tightening (QT) through the reduction of their balance sheet by $95 billion per month, which Goldman Sachs believes has resulted in tightening financial conditions and higher yields. Given the Fed’s steadfast commitment to bringing inflation down, we struggle accepting the market’s expectations that the Fed will cut rates as soon as March, rather believing that without some exogenous event or sharp economic contraction, the Fed will likely keep rates unchanged until at least mid-year. Having extensively studied Volcker’s approach in the 1980s, it is unlikely that Powell wants to repeat those mistakes and cut rates too abruptly, which could cause inflation to reverse course as it did in the Volcker Era. Should our base case prove accurate, we would expect volatility to ensue as yields rise and equities sell off, giving back some of the gains realized to close out 2023.

Centura’s Outlook

The Fed’s goal to slow the economy just enough to lower inflation back to its 2% mandate and avoid recession serves as the base outcome expected by the Fed and most market participants. Should this play out accordingly, we expect 2024 to produce solid returns in both equities and bonds. However, the market currently appears priced to perfection so investors should proceed with caution as monetary policy uncertainty, any reversal in yields, the presidential election, and, to a lesser extent, a looming U.S. Government shutdown could all lead to bouts of market angst and volatility. Nevertheless, there are opportunities across all asset classes moving into 2024 though, equities provide an example of how caution is warranted amidst attractive opportunities.

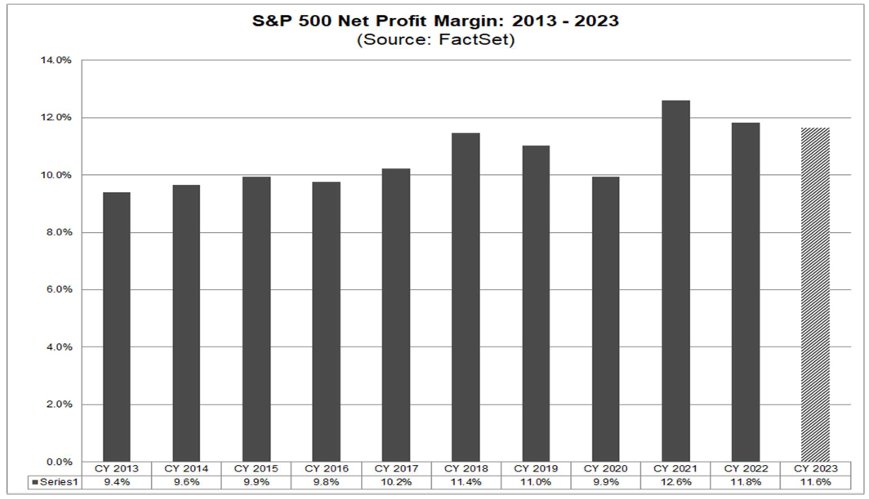

Earnings for the third quarter snapped the three consecutive quarters of negative earnings growth as companies began to experience stronger than expected revenue growth. Revenues grew at 2.4% year-over-year and as earnings advanced 4.9%, according to FactSet. The surprising third quarter results indicated to investors that companies have weathered the Fed’s rate hiking storm better than anticipated. Surprisingly, even in the face of 15-to-20-year high interest rates, companies have been able to maintain solid profit margins through successful cost-cutting measures over the last two years. However, FactSet has witnessed revisions for fourth quarter earnings, dropping from 8.1% on September 30 to 2.4% as of December 15.

Forward 12-month P/E ratios are approximately 19.3x, above both their five-year and ten-year averages of 18.8x and 17.5x, respectively. This shows that equities are slightly overvalued and thus priced to perfection. The fourth quarter saw multiple expansions in price appreciation and meager profits. To limit further multiple expansion, we need to see meaningful earnings growth to make valuations more attractive from their current levels.

The Federal Reserve rhetoric from December’s meeting and waning inflation give us optimism, but we remain cautious. The market remains too dependent on the Fed, which has become reliant on poor economic data, and with worsening conditions, the more likely the Fed is to pivot and cut rates sooner.

Many variables in Q4 surprised to the upside yet continue to moderate. However, as we look forward, the consumer’s health gives us pause, as does the impact of prolonged elevated rates on corporate balance sheets of less than fundamentally sound businesses – both of which could result in increased consumer and business defaults. We continue to believe the two largest immediate risks hinge on a misstep or abrupt change to the expected Fed outcomes and a potential resurgence of inflation, both of which are related.

We enter the year with portfolio allocations aligned with our long-term targets. While higher rates will continue to cause issues for some companies, we expect earnings to grow from 2023 levels in 2024. Additionally, equities generally produce a positive return during election years, so while volatility is likely to increase as we approach the election in the third and fourth quarters, we expect history to repeat itself and deliver gains. According to First Trust, on average, the market was up 11.28% during 19 of the past 23 total elections, or 83% of the time, since the S&P 500 began producing positive results.

Yields should continue to grind lower over the course of the year, presenting attractive opportunities to produce asymmetric returns in bonds. While a strong bounce in the fourth quarter slightly dampened our 2024 return expectations for fixed income securities, we believe portfolios should extend duration. Extending duration should allow investors to clip an attractive yield, while also providing them with the opportunity to experience capital appreciation for a total return exceeding what they will clip sitting in money market funds or short-term Treasury bills.

Elevated interest rates continue to punish private real estate returns, with further slight downward valuation adjustments expected from their previous marks. Real estate is an interest rate-sensitive asset class; as rates continue to move lower, we anticipate a pick-up in activity, and a subsequent reversal of valuations. While we believe we are nearing the light at the end of the tunnel for several real estate sectors like multifamily and industrial, unfortunately, we believe further paper losses are likely in the short term.

Though yields have fallen sharply, private credit is predominantly floating and tied to a base rate such as the Secured Overnight Financing Rate (SOFR), which is closely linked to the Fed Funds overnight rate. Yields on private credit should remain at their current levels until the Fed begins to cut rates. Even as the Fed cuts rates, the floating rate on private loans does not adjust immediately. Rather, there is a delay before the loan terms reset lower, with private loans typically resetting coupons quarterly. Barring a catastrophic event, the Fed is likely to lower rates more methodically than they hiked them, supporting higher yields in private credit. Combining traditional bonds with private credit should produce a balanced and diversified approach toward income production and total return in 2024.

As the door closes on 2023 and we enter 2024, we do so cautiously optimistic, as we believe the market has gotten a little ahead of itself, and there is still a high-level of uncertainty. We will continue to move forward with our constant focus on quality. Thank you for your continued confidence and support. If you have questions or concerns, please contact your Centura Wealth advisor.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on the market and other conditions. These documents may contain certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Centura Wealth Advisory is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Centura Wealth Advisory and its representatives are properly licensed or exempt from licensure. 12255 El Camino Real, St. 125, San Diego, CA 92130.

https://centurawealth.com/wp-content/uploads/2024/01/Market-Report-2023.jpg14142119Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2024-01-02 13:02:002025-07-06 21:34:22Q4 2023 Market Wrap: the US Avoided a Recession in 2023

The Tax Cuts and Jobs Act (TCJA) significantly increased estate and gift tax exemptions, offering relief for high-net-worth families. However, with the law set to sunset on December 31, 2025, the exemption will be cut in half—exposing many more estates to a 40% tax rate on assets above the threshold.

In this episode of Live Life Liberated, Kyle Malmstrom, Managing Director, and Christopher Hyman, Director of Insurance Solutions, break down what’s changing and how to plan ahead to protect your wealth.

The Estate Tax Exemption: What’s Changing?

A Brief History of the Estate Tax

The federal estate tax has been in place since 1916, with 14 major changes to exemption levels and tax rates over time. Under the TCJA:

The individual estate tax exemption doubled from $6 million to over $12 million

For married couples, the exemption rose to $26 million in 2023

If no changes are made, the exemption will drop back to around $6-7 million per person in 2026

“Many families who had no estate tax concerns before will now find themselves facing a massive tax bill.” – Christopher Hyman

The Estate Tax Sunset: Who Will Be Affected?

If you have a net worth above $13 million as a married couple (or $6.75 million individually) in 2026, your estate could be taxed at 40% upon your passing.

“We were just one vote away from a proposal to drop the exemption even further—to $3.5 million per person. This issue is not going away.” – Kyle Malmstrom

Why Liquidity Planning is Critical

Many high-net-worth individuals hold illiquid assets such as:

Businesses

Real estate portfolios

Alternative investments

Collectibles or private equity holdings

The estate tax must be paid within nine months of death. If your wealth is tied up in a business or real estate, your heirs may be forced to sell assets at an inopportune time just to cover the tax bill.

“Imagine needing to sell real estate in 2009 at rock-bottom prices just to pay estate taxes—that’s what we want to avoid.” – Kyle Malmstrom

Three Ways to Transfer Wealth

When planning for estate taxes, assets can go to:

Heirs (family, friends, etc.)

Charity

The government (via estate taxes)

“Most families want their wealth to go to their heirs or a cause they believe in—not the IRS.” – Christopher Hyman

Estate Tax Strategies: What You Can Do Now

1. Squeeze, Freeze, and Burn Strategy

One widely used estate planning approach includes:

Squeeze: Reduce the valuation of assets through discounting techniques

Freeze: Transfer assets to trusts or other structures to cap their taxable value

Burn: Use income tax strategies to further reduce estate size over time

This method helps minimize estate tax liability but requires early and careful structuring.

2. The Role of an Irrevocable Life Insurance Trust (ILIT)

For many high-net-worth families, a properly structured life insurance policy inside an ILIT is one of the most effective tools to:

Create liquidity upon death (tax-free cash to cover estate taxes)

Avoid forced asset sales

Provide flexibility for business owners and real estate investors

“Life insurance provides immediate, tax-free liquidity right when you need it most.” – Christopher Hyman

Why Expert Guidance Matters

Estate planning is complex—especially when navigating trust structures, business ownership, and tax law changes. Working with specialists who understand both estate planning and life insurance is key to building a strategy that:

Preserves control over assets

Minimizes tax exposure

Ensures a seamless wealth transfer

“Our firm specializes in integrating life insurance into estate plans in a way that maximizes flexibility and minimizes costs.” – Kyle Malmstrom

Final Thoughts: Take Action Now

If you wait until late 2025, finding an estate planning attorney who isn’t fully booked will be a challenge. Now is the time to assess your estate tax exposure and explore proven strategies to protect your wealth.

The information covered and posted represents the views and opinions of the guest and does not necessarily represent the views or opinions of Centura Wealth Advisory. The content has been made available for informational and educational purposes only. The content is not intended to be a substitute for professional investing advice. Always seek the advice of your financial advisor or other qualified financial service provider with any questions you may have regarding your investment planning.

Centura Wealth Advisory (Centura) is an SEC-registered investment advisor with its principal place of business in San Diego, California. Centura and its representatives are in compliance with the current registration and notice filing requirements imposed on SEC-registered investment advisors in which Centura maintains clients. Centura may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Past performance is no guarantee of future results. Tax relief varies based on client circumstances, and all clients do not achieve the same results.

https://centurawealth.com/wp-content/uploads/2025/03/Ep-89-Estate-Planning.jpg14142121Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2023-12-27 21:15:002025-04-08 16:16:42Ep. 89 How to Plan for the Looming Estate Tax Issue

The financial services industry has undergone a major transformation, shifting from commission-based models to fee-based Registered Investment Advisors (RIAs). While this change aimed to align client and advisor interests, it also led to the bundling of investment management with financial planning—raising the question:

Are clients actually getting maximum value from bundled services?

In this episode of Live Life Liberated, Derek Myron, CFP®, Managing Director, and Sean Clark, Director of Financial Planning, discuss:

The rise of the fee-based RIA model

Above-the-line vs. below-the-line planning—what truly moves the needle

How high-net-worth individuals can optimize income tax, wealth transfer, and balance sheet management

Steps to take if you feel underserved by your current financial team

The Evolution of Financial Services: From Commissions to RIAs

How Did We Get Here? A Brief History

Financial services have evolved dramatically, from commission-based brokers to fiduciary-focused RIAs:

Pre-1980s: Trust and estate planning was primarily for Rockefeller-level wealth

1980s-1990s: Stockbrokers dominated the market, earning commissions on trades

1990s-2000s: Discount brokers and online trading changed the game, leading to fee-based models

2000s-Present: RIAs grew significantly, emphasizing fee transparency and fiduciary responsibility

“The RIA industry didn’t really take hold until the 2000s, when access to information and online trading made commissions obsolete.” – Derek Myron

What Does It Mean to Be a Fiduciary?

Unlike brokers who follow a suitability standard (recommending acceptable products), RIAs must adhere to a fiduciary standard—meaning they are legally obligated to act in the best interest of the client.

“Being a fiduciary means finding the best-in-class solutions—not just the products our firm endorses.” – Sean Clark

However, as RIAs expanded, many firms began bundling services, raising concerns about whether clients were receiving tailored, high-value financial planning or simply a one-size-fits-all approach.

Above-the-Line vs. Below-the-Line Planning: Where’s the Value?

At Centura Wealth Advisory, planning is categorized into two levels:

Below-the-Line Planning: Necessary but Incremental

These services support investment management but don’t necessarily drive exponential financial outcomes:

“Below-the-line planning is helpful, but it’s not what transforms a client’s financial future.” – Derek Myron

Above-the-Line Planning: Where the Real Impact Happens

For high-net-worth individuals, true financial impact comes from above-the-line services:

❏ Income tax planning – Forward-looking strategies to reduce lifetime tax burden ❏ Wealth transfer planning – Structuring assets to maximize intergenerational wealth ❏ Balance sheet optimization – Managing debt, asset structuring, and liquidity events

“Income tax planning isn’t just about this year—it’s about the next 5, 10, or even 20 years.” – Sean Clark

While most financial firms offer planning, it’s often bundled with investment management, making it difficult for clients to measure true value.

The Problem with Bundled Financial Services

Why Do Firms Bundle?

Many firms bundle planning with investment management to:

Increase client retention by adding perceived value

Differentiate themselves in a competitive investment management space

Create a “sticky” client relationship where it’s harder to separate services

But for high-income earners and ultra-high-net-worth families, bundled services often result in surface-level planning that lacks depth and customization.

“Bundled planning often does just enough to justify an AUM fee, but not enough to deliver transformative results.” – Derek Myron

The Case for Unbundling: Paying for What You Need

Why Separating Services Matters

Unbundling financial services provides greater transparency and accountability. Clients can:

❏ Clearly define what they are paying for in investment management vs. financial planning ❏ Measure value by comparing services and outcomes ❏ Ensure planning is proactive, not reactive

“A clear, delineated value proposition ensures that clients know exactly what they’re paying for and what results they should expect.” – Sean Clark

Who Benefits Most from Unbundling?

For individuals with $20M+ in net worth and $2M+ in annual income, specialized tax and wealth transfer planning can yield significant financial advantages.

“When you reach a certain level of wealth, incremental planning isn’t enough—you need strategic, proactive financial guidance.” – Derek Myron

How to Assess Your Financial Team: Are You Getting Maximum Value?

If you’re unsure whether you’re getting the best financial advice, consider these steps:

Step 1: Self-Assessment

❏ Am I paying for bundled services without understanding their value? ❏ Do I have income tax pain and need forward-looking strategies? ❏ Is my estate structured for efficient wealth transfer?

Step 2: Ask Your Professionals the Right Questions

✔ CPA: Do you provide forward-looking tax consulting, or just compliance? ✔ Estate Attorney: Are you considering my entire financial picture, or just drafting documents? ✔ Financial Advisor: What is your process for proactive income tax and balance sheet optimization?

“If your financial team can’t articulate their process, it’s a red flag.” – Sean Clark

Step 3: Consider a Second Opinion

If you suspect you’re underserved, it’s worth consulting with a fiduciary advisor who offers specialized planning and a clear fee structure.

Final Thoughts: Is It Time to Unbundle?

For many high-net-worth individuals and business owners, unbundling financial services leads to:

❏ Greater clarity on where fees are going ❏ Higher-quality financial planning tailored to complex needs ❏ More control over wealth, taxes, and long-term strategy

If you’re ready to explore an unbundled, results-driven approach to financial planning, connect with Derek Myron at [email protected] or Sean Clark at [email protected].

Disclaimer

The information covered and posted represents the views and opinions of the guest and does not necessarily represent the views or opinions of Centura Wealth Advisory. The content has been made available for informational and educational purposes only. The content is not intended to be a substitute for professional investing advice. Always seek the advice of your financial advisor or other qualified financial service provider with any questions you may have regarding your investment planning.

Centura Wealth Advisory (Centura) is an SEC-registered investment advisor with its principal place of business in San Diego, California. Centura and its representatives are in compliance with the current registration and notice filing requirements imposed on SEC-registered investment advisors in which Centura maintains clients. Centura may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Past performance is no guarantee of future results. Tax relief varies based on client circumstances, and all clients do not achieve the same results.

https://centurawealth.com/wp-content/uploads/2025/03/Ep-88-Unbundling-Financial-Services.jpg12992309Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2023-12-13 09:00:002025-04-08 16:16:42Ep. 88 Unbundling Financial Services and Maximizing Value for High-Net-Worth Individuals

With the 2024 U.S. presidential election approaching, investors are facing increased market uncertainty. Geopolitical tensions, potential tax law changes, and congressional instability—including the ousting of the Speaker of the House and the risk of a government shutdown—are all adding to the complexity.

In this episode of Live Life Liberated, Matt Griffith, CFP®, Senior Wealth Advisor, and Chris Osmond, CFA, CAIA®, CFP®, Chief Investment Officer, speak with Michael Townsend, Managing Director of Legislative and Regulatory Affairs at Charles Schwab & Company, about what investors can expect in the months ahead.

Key Topics Covered:

The current political landscape and market uncertainty

The speculation around Biden or Trump dropping out

The potential impact of a split Congress on tax and financial policy

How markets historically perform before and after elections

Why long-term investment strategies matter more than short-term political shifts

The 2024 Election: Political and Market Implications

What Investors Need to Know About the Political Landscape

Washington is experiencing one of its most volatile political cycles in decades. Speaker of the House Kevin McCarthy’s removal in October 2023 created legislative gridlock, and a looming government shutdown threatens further uncertainty. Meanwhile, foreign policy concerns, including Ukraine, Israel, and China-Taiwan tensions, add another layer of unpredictability.

“October 2023 was the nuttiest month I’ve seen in Washington in my 30 years here.” – Michael Townsend

With inflation, interest rates, and economic growth in flux, investors must navigate the election cycle carefully.

Will Biden or Trump Drop Out?

Speculation continues about whether President Biden or former President Trump will ultimately be on the 2024 ballot. Concerns about Biden’s age and health persist, while Trump faces multiple legal challenges.

“My operating assumption is we will have a Biden-Trump rematch. But there are a lot of voters who are unenthusiastic about this potential matchup.” – Michael Townsend

Despite these uncertainties, investors should focus on policy outcomes rather than political drama.

A Divided Government: What It Means for Tax and Economic Policy

What’s at Stake in Congress?

Republicans need two Senate seats to regain control.

Democrats are poised to retake the House, potentially flipping both chambers.

If Congress is split, expect continued gridlock and delayed policymaking.

“We have never had an election where the House and Senate flipped in opposite directions—it would be unprecedented.” – Michael Townsend

A divided Congress could mean prolonged inaction on key financial policies, particularly tax reform.

The 2025 Tax Cliff: What Investors Should Prepare For

One of the biggest post-election issues will be the expiration of the 2017 Tax Cuts and Jobs Act (TCJA). Key provisions set to sunset in January 2026 include:

✔ Higher marginal tax rates (top rate returning to 39.6%) ✔ Estate tax exemption cut in half (from ~$26M per couple to ~$13M) ✔ Changes to deductions and pass-through business tax rules

“The estate tax is one of the least partisan tax issues in Washington—many Democrats support maintaining higher exemptions due to its impact on family-owned businesses.” – Michael Townsend

While some provisions may be extended, expect heated debates over revenue needs and deficit reduction.

Market Performance and Investment Strategies During Election Years

How Do Markets Historically Perform in Election Years?

Historically, election years have been strong for the markets. Since 1928, the S&P 500 has averaged a 7.5% return in presidential election years.

“Markets tend to perform well during an election year—uncertainty creates volatility, but history suggests solid returns.” – Michael Townsend

However, policy implementation takes time, meaning major shifts often don’t happen immediately post-election.

Does Political Party Impact Market Performance?

While many assume one party is better for the markets than the other, historical data suggests otherwise:

✔ The market has performed better under Democratic presidents (5–6% higher annual returns) ✔ The best configuration for market stability? A Democratic president with a Republican-controlled Congress ✔ Unified governments—regardless of party—show similar market performance

“There is almost no difference in market performance under a unified Republican or Democratic government—investors should focus on broader economic trends.” – Michael Townsend

How Investors Should Approach Election-Year Volatility

What to Avoid: Emotional Decision-Making

Election years often trigger fear-driven investment moves. Many investors:

❌ Delay investments until after the election ❌ Sell assets prematurely due to uncertainty ❌ Overreact to political rhetoric

“Elections are emotional events, but investors should focus on long-term goals, not short-term politics.” – Michael Townsend

How to Stay on Track

✔ Maintain a diversified portfolio – Election cycles introduce short-term volatility, but diversification helps mitigate risk. ✔ Monitor tax policy changes – High-net-worth individuals should work with advisors to optimize tax strategies ahead of potential shifts. ✔ Ignore the headlines – Most campaign promises never translate into real policy. Focus on long-term investment fundamentals.

“No policy in Washington is ever guaranteed—investors should be wary of pundits claiming otherwise.” – Michael Townsend

Final Thoughts: Cutting Through the Noise

With political uncertainty, tax policy changes, and market volatility, staying disciplined is key. Instead of reacting to headlines, investors should:

✅ Assess their long-term financial goals ✅ Prepare for potential tax changes in 2025 ✅ Consult with advisors to optimize their investment strategy

If you need guidance navigating the 2024 election’s impact on your portfolio, contact Centura Wealth Advisory at (858) 771-9500 or visit centurawealth.com.

For ongoing insights, listen to Michael Townsend’s podcast, WashingtonWise, available on Apple Podcasts and Spotify.

Disclaimer

The information covered and posted represents the views and opinions of the guest and does not necessarily represent the views or opinions of Centura Wealth Advisory. The content has been made available for informational and educational purposes only. The content is not intended to be a substitute for professional investing advice. Always seek the advice of your financial advisor or other qualified financial service provider with any questions you may have regarding your investment planning.

Centura Wealth Advisory (Centura) is an SEC-registered investment advisor with its principal place of business in San Diego, California. Centura and its representatives are in compliance with the current registration and notice filing requirements imposed on SEC-registered investment advisors in which Centura maintains clients. Centura may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Past performance is no guarantee of future results. Tax relief varies based on client circumstances, and all clients do not achieve the same results.

https://centurawealth.com/wp-content/uploads/2025/03/Ep-87-election-uncertainty.jpg14142121Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2023-11-22 09:00:002025-04-08 16:16:42Ep. 87 Investing Amidst Uncertainty: A 2024 Election Discussion with Michael Townsend

Fostering a Thriving Corporate Culture in a Hybrid World

With hybrid work environments becoming the norm, many companies struggle to maintain a strong culture, attract top talent, and build cohesive, high-performing teams. At Centura Wealth Advisory, we have implemented innovative strategies to create an engaging, supportive, and productive workplace—whether employees are in San Diego or working remotely across the country.

In this episode of Live Life Liberated, Derek Myron, Founder and CEO and Jonathan Freeman, COO, discuss the principles behind Centura’s workplace culture, including leadership practices, team-building traditions, and the importance of communication and trust.

The Challenges of Expanding a Team Across the Country

Centura has grown rapidly, expanding from a primarily San Diego-based firm to a national presence with remote employees across the U.S. This shift has presented challenges, including:

Maintaining cohesion among in-office and remote employees

Ensuring new team members align with Centura’s high standards of excellence

Developing an engaging and supportive culture that encourages long-term retention

“Not everyone is walking the same halls or in the same meetings, so leadership must be intentional about creating cohesion and camaraderie,” says Freeman.

Building Culture Through Intentional Practices

A strong culture doesn’t happen by accident—it requires deliberate actions from leadership. At Centura, several practices help reinforce team unity and engagement:

Waffle Wednesdays – A weekly tradition where Centura’s leaders serve breakfast to the team, fostering an open and collaborative environment.

The 48-Hour Rule – Employees are encouraged to directly address workplace concerns within 48 hours to prevent unresolved issues from festering.

FreshBiz Thinking – A problem-solving mindset that encourages collaboration across departments to tackle challenges efficiently.

Business Coaching with Mitch Simon – Monthly leadership development sessions that enhance team dynamics and communication.

“Culture isn’t just one aspect of the game—it is the game. If you don’t foster it daily, it can quickly degrade,” says Freeman.

The Power of Communication & Trust in High-Performing Teams

At Centura, clear communication is the foundation of team success. A few key principles help maintain alignment across the organization:

Managing Promises: Employees follow a structured approach to commitments—either agreeing, declining, promising to promise, or renegotiating.

Condition of Satisfaction (COS): Before making a commitment, employees clarify expectations to ensure alignment.

No Daylight in the Say-Do Gap: Team members are expected to follow through on commitments, fostering accountability and reliability.

By instilling these habits, Centura ensures that every team member is empowered to take ownership of their work while maintaining trust across all levels of the organization.

Final Thoughts: Creating a Rockstar Team

Building a high-performance team requires intentional leadership, clear communication, and a commitment to continuous improvement. Whether through leadership coaching, structured team-building exercises, or fostering a culture of accountability, Centura’s approach demonstrates that a strong corporate culture leads to better client outcomes and employee satisfaction.

“An organization is only as strong as its weakest link. If we invest in our people, develop their skills, and foster a culture of collaboration, we create an environment where everyone thrives,” says Myron.

To learn more about Centura Wealth Advisory and its unique approach to leadership and culture, listen to the full episode now.

Disclaimer

The information covered and posted represents the views and opinions of the guest and does not necessarily represent the views or opinions of Centura Wealth Advisory. The content has been made available for informational and educational purposes only. The content is not intended to be a substitute for professional investing advice. Always seek the advice of your financial advisor or other qualified financial service provider with any questions you may have regarding your investment planning.

Centura Wealth Advisory (Centura) is an SEC-registered investment advisor with its principal place of business in San Diego, California. Centura and its representatives are in compliance with the current registration and notice filing requirements imposed on SEC-registered investment advisors in which Centura maintains clients. Centura may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Past performance is no guarantee of future results. Tax relief varies based on client circumstances, and all clients do not achieve the same results.

https://centurawealth.com/wp-content/uploads/2025/03/Ep-86-Keys-to-Building-an-Amazing-Corporate-Culture.jpg14142121Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2023-11-08 09:00:002025-04-08 16:16:42Ep. 86 Keys to Building an Amazing Corporate Culture and a Rockstar Team

As wealth increases, financial planning needs become more complex. Centura Wealth Advisory (Centura) specializes in serving high-net-worth and ultra-high-net-worth individuals, helping them optimize taxes, protect assets, and structure their wealth efficiently.

In this episode of the Live Life Liberated podcast, Kyle Malmstrom and Sean Clark, MBA, share insights into Centura’s Liberated Wealth® process and discuss advanced planning strategies that help clients retain and grow their wealth.

Why Centura Stands Apart

Many wealth management firms offer broad financial planning, but Centura focuses on above-the-line planning, meaning income tax, wealth transfer, and balance sheet optimization. These elements help clients reduce tax liabilities and optimize their overall financial picture.

“Being able to save people money on income taxes is unique. Wealth transfer is another area, but really income tax planning is where we move the needle.” — Sean Clark

Unlike traditional firms that focus on marginal tax bracket adjustments or standard wealth management, Centura dives deep into the tax code to find advanced strategies tailored to individual client needs.

The Importance of Early Planning

Timing is critical when it comes to tax and wealth transfer planning. Centura categorizes planning windows into three phases:

Gold Period: Before receiving an LOI (Letter of Intent) for a business sale, when the most impactful planning can occur.

Silver Period: Between receiving an LOI and the end of the tax year, when meaningful strategies can still be implemented.

Bronze Period: After the tax year closes, where options become limited.

“The worst conversation is, ‘I just signed my LOI yesterday. What can I do?’ Well, you could have talked to us six months ago.” — Kyle Malmstrom

The best outcomes happen when planning starts 12 to 36 months before a major liquidity event. However, even last-minute strategies can still create value when executed properly.

Centura’s Due Diligence Process

With over 50 advanced planning strategies, Centura ensures every recommendation is thoroughly vetted. The firm employs a rigorous due diligence process that includes:

Analyzing tax and legal risks to ensure compliance.

Assessing economic viability to confirm financial benefits.

Evaluating custodians and sponsors to select the best partners for implementation.

“These aren’t garage-band strategies. If you get it wrong, you’re going to face issues. You need people who have done this dozens of times and know the nuances.” — Kyle Malmstrom

This level of scrutiny prevents clients from falling into risky or unproven tax strategies and ensures they receive proven, reliable solutions.

Who Benefits Most from Centura’s Planning?

Centura’s services provide the most value to individuals who:

Earn $2 million+ in income or have a net worth of $20 million+.

Have complex tax issues that persist over multiple years.

Are experiencing a money-in-motion event, such as the sale of a business or real estate.

Need customized tax and wealth strategies beyond traditional financial planning.

For these individuals, Centura aims to deliver at least 5x ROI on tax savings relative to its fees.

Optimize Your Wealth with Centura

If you’re looking for sophisticated tax and wealth strategies tailored to your unique financial landscape, Centura Wealth Advisory can help.

The information covered and posted represents the views and opinions of the guest and does not necessarily represent the views or opinions of Centura Wealth Advisory. The content has been made available for informational and educational purposes only. The content is not intended to be a substitute for professional investing advice. Always seek the advice of your financial advisor or other qualified financial service provider with any questions you may have regarding your investment planning.

Centura Wealth Advisory (Centura) is an SEC-registered investment advisor with its principal place of business in San Diego, California. Centura and its representatives are in compliance with the current registration and notice filing requirements imposed on SEC-registered investment advisors in which Centura maintains clients. Centura may only transact business in those states in which it is notice filed or qualifies for an exemption or exclusion from notice filing requirements. Past performance is no guarantee of future results. Tax relief varies based on client circumstances, and all clients do not achieve the same results.

https://centurawealth.com/wp-content/uploads/2025/03/How-Centura-Creates-Value-for-High-Net-Worth-Individuals-Ep.-85.jpg8361253Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2023-10-25 09:00:002025-04-08 16:16:42Ep. 85 How Centura Creates Value for High-Net-Worth Individuals

Preserving and transferring wealth across generations is a significant concern for affluent families. The desire to pass down as much of one’s hard-earned assets as possible while minimizing tax burdens is a universal goal. Achieving this goal, however, requires strategic guidance, expert knowledge, and a comprehensive overview of all assets and goals.

In this blog, we’ll explore the key strategies and considerations involved in reducing estate and gift taxes for affluent families.

Understanding the Complexity of Affluent Estates

Affluent families are characterized by their substantial and multifaceted estates. These estates encompass a diverse array of assets, ranging from valuable financial investments and real estate properties to ownership stakes in businesses and more. The complexity of these estates requires a nuanced approach to estate planning that goes beyond the basic considerations.

The Importance of Meticulous Estate Planning

Given the intricate nature of their holdings, affluent families must engage in meticulous estate planning to facilitate a seamless transition of their wealth to the next generation. Estate planning is not just about the distribution of assets; it encompasses a comprehensive strategy to ensure the family’s financial well-being while minimizing potential tax liabilities. This process involves a detailed evaluation of the family’s financial landscape, aspirations, and the desired legacy.

Now let’s take a closer look at mistakes affluent families often make when estate planning and how to prevent these mistakes.

Mistake 1: Procrastinating

One of the most prevalent mistakes among wealthy families is waiting to handle their estate planning. The belief that estate planning is something to be dealt with in the distant future can lead to rushed decisions or even a lack of a comprehensive plan altogether. By delaying the process, families miss out on valuable opportunities to minimize tax liabilities, establish effective wealth transfer strategies, and ensure that their intentions are carried out.

Mistake 2: Failing to Create a Comprehensive Plan

Estate planning is not a one-size-fits-all endeavor. Creating a comprehensive plan involves a meticulous evaluation of an individual’s or family’s financial landscape, goals, and unique assets. Failing to account for all relevant aspects of an estate can result in assets being overlooked or not distributed according to the intended wishes. Each piece of the estate puzzle, from financial investments to real estate holdings and business interests, should be carefully considered.

Mistake 3: Overlooking Tax Implications

Tax implications play a significant role in estate planning, particularly for wealthy families. Failing to understand and account for potential tax liabilities can lead to significant erosion of the estate’s value. Effective estate planning involves using strategies like trusts, gifting, and tax-efficient investment vehicles to minimize the tax burden on heirs and beneficiaries.

Mistake 4: Neglecting Changes in Family Dynamics

Family dynamics are constantly evolving, and failing to account for these changes in an estate plan can lead to disputes, misunderstandings, and unintended outcomes. Marriages, divorces, births, and deaths can all impact the distribution of assets and the intentions of the estate owner. Regularly reviewing and updating the estate plan to reflect these changes is essential to ensuring its relevance and effectiveness.

Mistake 5: Choosing the Wrong Executor or Trustee

The role of an executor or trustee is crucial in executing the wishes outlined in the estate plan. Selecting an executor without considering their financial acumen, interpersonal skills, and alignment with the family’s values can lead to mismanagement and conflicts. Choosing a trustworthy and capable executor who understands the family’s goals is paramount to a successful estate transfer.

Mistake 6: Underestimating the Importance of Communication

Transparent communication is key to avoiding misunderstandings and potential conflicts among family members. Failing to discuss the estate plan with heirs and beneficiaries can lead to surprises and resentment down the line. By openly discussing intentions, addressing concerns, and managing expectations, families can foster understanding and unity during what can be a sensitive process.

Mistake 7: Disregarding the Need for Professional Guidance

Estate planning for wealthy families is a complex and multifaceted task that requires expert knowledge in legal, financial, and tax matters. Relying solely on personal judgment without seeking professional guidance can lead to missed opportunities and costly errors. Collaborating with attorneys, financial advisors, and tax experts ensures that the estate plan is comprehensive, legally sound, and aligned with the family’s goals.

As you’ve discovered, estate planning is more than just a financial exercise; it’s a holistic approach to preserving your wealth, values, and legacy for generations to come. By exploring the potential mistakes that can arise and the strategies to avoid them, you’re already taking crucial steps toward securing a lasting legacy.

Connect With Centura

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients with fully transparent reporting and tools to make informed decisions around their wealth plan.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/Top-Mistakes-Wealthy-Families-Make-in-Estate-Planning.jpg14142120Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2023-10-06 08:05:002025-04-08 16:16:42Top Mistakes Wealthy Families Make in Estate Planning