Taxpayers, especially high-net-worth individuals, commonly experience the issues of high-income taxes and wealth transfer taxes in their financial planning.

Charitable lead annuity trusts, or CLATs, help taxpayers tackle these issues through advantages including tax deductions and wealth transfer planning.

Below, we’ll discuss:

How charitable lead annuity trusts (CLATs) work, and

How taxpayers can implement a grantor charitable lead annuity trust (G-CLAT) to experience both long and short-term tax benefits

What is a Charitable Lead Annuity Trust?

A charitable lead annuity trust (CLAT) is a charitable trust in which a charity, donor-advised fund, or a foundation that the grantor selects, receives annual payments. These payments may be set for a term of years or for the grantor’s lifetime.

At the end of this period, the remaining CLAT assets are distributed amongst the trust’s non-charitable beneficiaries. These beneficiaries are typically the grantor’s descendants or trusts for the descendants’ benefit.

What is a Grantor Charitable Lead Annuity Trust?

In a grantor charitable lead annuity trust (G-CLAT), the trust corpus remaining at the end of the term is given back to the donor instead of the donor’s descendants.

Does a Taxpayer Need Donative Intent to Implement a G-CLAT?

A taxpayer does not need donative intent to implement a G-CLAT.

In fact, taxpayers can utilize these trusts for a variety of purposes. Let’s review how G-CLATs work and their advantages.

How Does a G-CLAT Work?

Let’s take a look at G-CLAT mechanics. We like to break it down like this:

1. Grantors fund CLAT with a one-time deposit

2. The taxpayer implements a pre-determined annual charitable payment schedule

3. Grantor(s) receive income tax dedication to be used up to six years – likely at 99% or more of the deposit

4. All taxable events flow back to the grantor(s)

5. Invest in Limited Partners real estate

6. If structured properly, the remainder interest transfers to the remainder beneficiary, free of estate tax

What Are the Benefits of G-CLATs?

The advantages of implementing a grantor charitable lead annuity trust include, but are not limited to:

Income tax planning

Wealth transfer planning

Charitable planning

Let’s speak about each of these in a bit more detail.

Income Tax Planning

Taxpayers will experience the benefits of both immediate and long-term tax benefits once they’ve successfully implemented a G-CLAT. The trust, for example, will result in an immediate income tax dedication for the taxpayer, which is a present value benefit.

This immediate income tax reduction is:

Subject to 20 to 30% of adjusted gross income (AGI) limitation

Able to be utilized over six tax years

Ideally consumed at the highest marginal income tax rates

Wealth Transfer Planning

In addition to the immediate benefits of G-CLATs, these trusts also include wealth transfer tax savings. Through these savings, the taxpayer can experience the benefits of a G-CLAT for years.

Charitable Planning

While the taxpayer does not need to have donative intent, charitable planning benefits G-CLATs if the taxpayer decides to participate.

For instance, as a future benefit, G-CLATs provide satisfying charitable annuity payments with appreciated assets, avoiding recognition of gain on these distributions to 501(c)3s.

How to Get Started

At Centura Wealth Advisory, we know the minute details of how to optimize a grantor charitable lead annuity trust or a charitable lead annuity trust. In fact, our team has successfully implemented over 280 CLAT transactions.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1032388356.jpg13782176Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2022-08-28 20:04:002024-08-23 20:06:20What is a Charitable Lead Annuity Trust (CLAT)?

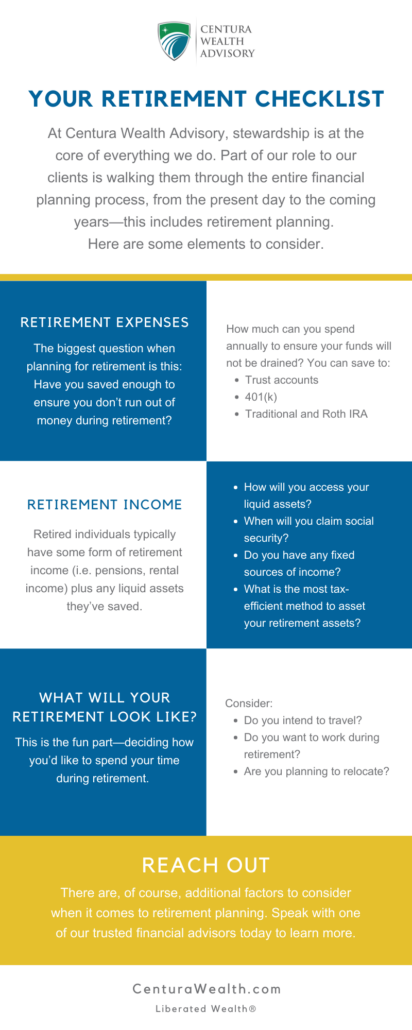

At Centura Wealth Advisory, stewardship is at the core of everything we do. We believe in partnering with our clients to liberate their wealth management process. Part of our role as stewards is walking our clients through the entire financial planning process, from the present day to the coming years.

One of the main areas we address with our clients is their retirement plans. After a long career, many people dream of retirement. Whether it be spending your free time volunteering, making memories with your grandchildren, or sipping a piña colada on a tropical beach, one thing you don’t want to have to worry about is money.

In order to relieve this stressor, a lot of financial planning and coordination has to occur. Today, we’ve outlined your retirement checklist, and while it is not your one-stop shop for all of your retirement planning (we’d recommend reaching out to a trusted financial advisor for that), it does include the various elements to consider prior to leaving your career.

Your Retirement Expenses: Questions to Consider

There are many questions an individual, along with their trusted financial planner, can review in order to fine-tune the logistics of their retirement. The biggest question when planning for retirement is this: Have you saved enough to ensure you don’t run out of money during retirement?

In order to answer this question, you need to identify how much you can spend annually to ensure your funds will not be drained. Luckily, throughout one’s life, there are a variety of different retirement accounts you can save to trust accounts, 401(k), traditional and Roth IRA accounts, and so on.

Once you retire, certain expenses will be reduced, eliminated, and/or added. To further carve out your budget, ask yourself if:

You’ll be expected to financially support any family members

You anticipate going on any big family vacations or need a medical procedure

You might have any large one-off payments (for example, a wedding or car)

Your mortgage will be paid off

You will have to pay expenses that are currently being paid by your employer (i.e. medical and/or dental insurance, utilities, automobiles)

Consider all of these elements to help plan your expenses during this time.

Retired individuals typically have some form of retirement income (i.e. pensions, rental income) plus any liquid assets they’ve saved.

Tax Planning

Retirement tax planning, however, is a whole different story. You want to ensure that you can access your assets as tax-efficiently as possible.

Below are some questions to consider when identifying your retirement income.

How will you access your liquid assets?

When will you claim social security?

Do you have any fixed sources of income? (i.e. rental income, pensions, annuities, etc.)

Are there opportunities (Roth IRA) for creating tax-free income that you can access down the road?

What is the most tax-efficient method to asset your retirement assets?

What Will Your Retirement Look Like?

This is the fun part—deciding how you’d like to spend your time. As previously mentioned, there are many ways to spend your retirement: volunteering, spending time with grandchildren, sipping down piña coladas on a tropical beach, and the list goes on.

Many people, however, fail to recognize just how much time comes with retirement. For most, they gain 40 or more hours a week (when you factor in commuting) to do whatever they please.

Having some sort of structure for the weeks and days can be helpful—especially for those who felt their career was a large part of their identity. Consider the following questions when deciding what your retirement might look like:

Do you intend to travel? With family, friends, a partner, or alone? International or local?

Do you want to work? On what level? Will you volunteer or work a part-time job?

Are you planning to relocate? If so, in or out of state? Out of the country even? It’s important to consider how expenses and taxes in a different location than where you are currently might size up.

A Final Word

There are, of course, various additional factors and considerations when it comes to retirement planning; for example, asset allocation, loss of bonuses, your stock portfolio, and more. This article is just a jumping-off point.

There’s no article that could detail all these elements as precisely as speaking face to face with a trusted financial advisor like those at Centura Wealth Advisory.

https://centurawealth.com/wp-content/uploads/2024/08/RetirementPlanning-scaled.jpg10972560Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2022-05-13 16:29:002024-08-27 16:32:23Your Retirement Checklist: Elements to Consider

The general lifecycle of a business typically follows a few different stages. These stages include start-up, development and establishment, and finally maturity. As a business owner, once you’ve reached the maturity stage of your business, you are likely considering what the future of your company holds.

What will happen to your company when you retire? While planning to exit your business can be an emotional decision, it is also essential to the greater success of your business. What we have found, is that most business owners prefer to procrastinate on putting together a proper exit plan, which could end up being the reason your company does not succeed beyond your leadership.

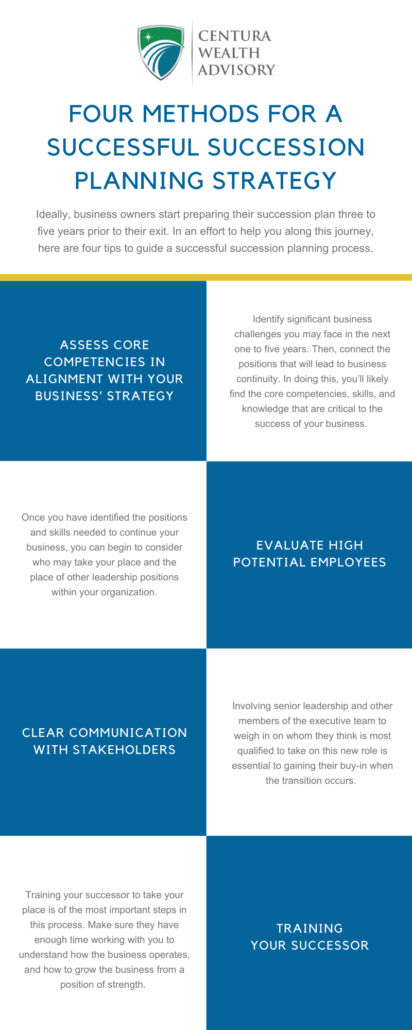

Ideally, business owners start preparing their succession plan three to five years prior to their exit. This plan is in place to protect the company when the executive team is no longer available to serve their duties. When succession planning is rushed, hiring mistakes are more likely to occur, and the future of your business could be at stake.

In an effort to help you along this planning journey, here are a few tips to guide a successful succession planning process.

Assess Core Competencies in Alignment with your Business’ Strategy

First, take a look at your organization and work to identify the significant business challenges you may face in the next one to five years. Then, you can connect the positions that will lead to business continuity in the long run. In doing this, you’ll likely find the core competencies, skills, and knowledge that are critical to the success of your business.

Evaluate High Potential Employees

Once you have identified the positions and skills needed to continue your business, you can begin to consider who may take your place and the place of other leadership positions within your organization.

During this process, it’s important to account for your overall business strategy. Is the person you’re considering the right person to execute that strategy? What skills does this person need to drive this strategy forward?

Clear Communication with Stakeholders

As you go through the process of finding your successor, it’s important to include other key stakeholders within the business. Involving senior leadership and other members of the executive team to weigh in on whom they think is most qualified to take on this new role is essential to gaining their buy-in when the transition occurs.

Training Your Successor

Now, it’s time to communicate with your successor. Training your successor to take your place is of the most important steps in this process. Make sure they have enough time working with you to understand how the business operates, and how to grow the business from a position of strength.

Be sure to spend time with them during this entire process. Help them make decisions with your guidance, show them alternatives that they might not think of due to experience, and help them understand the risks associated with their decisions.

To go a step further, before you decide to leave your business, craft a strategic plan with one another. This helps ensure your successor is prepared and bought into creating a successful future for your business.

Potential Obstacles

Lastly, there are a few potential obstacles that you may run into during this process. These obstacles typically include timing, resistance to change, and lack of company support.

Timing

The entire succession planning process can be a time-consuming one. The time it takes to assess, evaluate, and develop your successor is not something to lose sight of. This is why it is typically recommended to start your succession planning at least three to five years in advance.

Not taking the time to develop this process can be detrimental to your company’s success. As we mentioned above, it usually leads to hiring mistakes, but it also has a large impact on your organization as a whole. If your successor is unprepared to take on this new role, your business will not be able to reach its full potential.

Resistance to Change

One of the reasons it is recommended to take three to five years to a succession plan is the impact it has on your people. Many people are resistant to change, especially as it relates to their careers.

Preparing your successor over time, allows the rest of your organization to familiarize themselves with the new leadership style they will be experiencing. Which leads to greater buy-in, and an easier transition overall.

Lack of Support

Similar to the point above, during any business transition, you will likely have naysayers, skeptics, and resistance. Most of these issues stem from the emotions that arise when people are concerned that their job is at risk. A simple way to mitigate this issue is to communicate as frequently and transparently as possible.

Aside from succession planning, there are other factors that go into exiting your business. For you, that may mean selling your business. How can you begin to prepare to sell your business a few years down the line? Take a look at one of our recent articles to get you started.

https://centurawealth.com/wp-content/uploads/2024/08/SuccessionPlanning.jpg13102289Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2022-05-02 16:34:002024-08-27 16:35:57Four Methods for a Successful Succession Planning Strategy

At Centura Wealth Advisory one of our core values is stewardship. We believe in partnering with our clients to liberate their wealth management process.

Part of our role as stewards to our clients is walking them through the entire financial planning process, from present-day to the coming years. One of the main areas we address with our clients is optimizing their retirement plans.

Listen to the Live Life Liberated Podcast for a detailed perspective from Derek Myron and Kyle Malmstrom, as they discuss how the potential estate tax changes may affect your retirement plan distributions.

One question we often ask our clients is, “Are you ready to overcome the complexities and burdens that come with your success?” Learning how to optimize their retirement plans is one of the foundational steps in overcoming the complexities that come with wealth management.

The two also share effective strategies to help transfer your accumulated wealth to your desired beneficiaries in a tax-efficient manner. Here are a few of the topics covered in the podcast linked above.

A brief overview of the proposed Build Back Better Act

Different ways to take your money out of Individual Retirement Accounts (IRAs)

“Live-on” assets versus “leave-on” assets — what is better for you?

Reasons to start planning your wealth transfer as early as possible

And more

*It should be noted that the information about proposals is subject to change from the time this article is published.

Employee Retirement Income Security Act

Prior to 1974, employees who worked at one or two companies their entire life would generally be given a pension. A pension is a defined benefit plan.

Some of the factors that would define an employee’s pension plan include:

Years of contribution

How much they made

These factors would determine how much money the employee would receive in the event of retirement, death, or become disabled or unable to work.

The main difference between ERISA and IRA is that ERISA plans are defined benefit plans. The IRA, on the other hand, was a defined contribution plan. This means that the employee can make investments that they control: stocks, bonds, and mutual funds.

Roth IRA

Since then, the rise in popularity of contribution plans has introduced other factors like a Roth IRA, which as far as optimizing your retirement plan, is a great starting point.

A Roth IRA is a retirement account that grows tax-free and can have tax-free distributions (as long as you hold it for five years and are above the age of 59).

There are two ways to optimize your retirement plan with a Roth IRA. The two ways are to contribute on an annual basis or to convert Converting your Roth IRA is taking your existing, non-Roth IRA asset and converting it into a Roth IRA in order to reap the tax benefits.

A Common Challenge

The challenge, however, is getting wealth from a traditional IRA into the Roth IRA. If an individual is in a low-income tax bracket, it’s not a terribly painful process. However, if you’re in a high-income tax bracket, it can present more of a challenge.

Due to the tax benefits that a Roth IRA provides, a large portion of people used this benefit. Because of this, the government did not predict the substantial amount of money put into these accounts. This brings us to the Build Back Better Plan.

Build Back Better Plan

The Build Back Better Plan was proposed by Congress in 2021. It aims to place further restrictions regarding Roth IRA contributions on wealthier individuals.

As stated by CNBC, “Wealthy individuals with more than $10 million in retirement savings would have to draw down their accounts each year, in a new type of required minimum distribution, or RMD. Lawmakers would also close “backdoor Roth” tax loopholes, used largely by the rich, and prohibit further individual retirement account contributions once those accounts exceed $10 million.”

One primary example of the reasoning behind the Build Back Better plan is the Paypal founder, Peter Thiel. Thiel has been able to amass $5 billion in his Roth IRA. Many people are upset and wondering, “How is this fair?”

How the Build Back Better Act Impacts Our Clients

Since 2019, Congress has been looking for loopholes to limit a plan owner’s options for optimization. In this case, “plan owners” include those who have a million dollars or more in their retirement plans and have an estate. Oftentimes, at this level of retirement planning, wealth transfer issues arise.

Plan owners are worried about how to optimize their distributions from their retirement plans because they know that Congress is looking to change the rules.

What Now?

There are many ways to continue to optimize your retirement plan while you’re alive.

You Can Make a Distribution

One option is to do a Roth conversion (depending on your facts and circumstances and the timing of income). You could then distribute from the Roth with the tax advantage. There’s also a way to do an in-kind distribution of different assets out of an IRA that may be tax efficient.

Another option is a qualified charitable distribution. This method eliminates tax liability and the funds are sent to a charity of your choice.

Set Future Goals

We believe your plan is not a one, two, or three-year plan.

Instead, we focus on a 10 or 15-year plan. The goal is to figure out how you’re intending to manipulate your cash flow and income tax, then to distribute your assets. This could mean distributing them to your spouse or even future generations.

In light of the potential changes coming from Congress, it’s important to start preparing for what’s to come. We encourage you to get in touch with your advisor and figure out a plan of action for your financial future.

As mentioned above, charitable giving is a great wait to improve your bottom-line, while also giving back to the community. Learn more about how charitable giving can improve your bottom line on our blog.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1264328274.jpg14142120Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2022-01-08 16:55:002024-08-27 16:56:52How to Optimize Your Retirement Plan

A commonly asked question that Centura Wealth Advisory receives is, “What is the difference between ESOPs and a sale of my company?”

The advantages of choosing to implement Employee Stock Ownership (ESOP) as a part of your exit plan, vs. selling your company to an outside entity depends on your specific situation.

ESOPs are available to C Corps and S Corps as a tax mitigation strategy to offset capital gains taxes. For those business owners who want to sell a part of their stake in a company, or in the case of one partner wanting to exit and the other(s) wanting to remain in control of the business when those remaining partners lack the desire to buy out the departing partner, ESOPs are a viable option.

Structuring your ESOPs sale is complex and outside the scope of this article, however, as a high-level overview of the choice between a straight third party sale to a competitor or venture capital/private equity sale let’s review the benefits of each type of exit.

What is an ESOP?

The National Center for Employee Ownership (NCEO) states that an ESOP provides “A variety of significant tax benefits for companies and their owners. ESOP rules are designed to assure the plans benefit employees fairly and broadly.”

ESOPs are Employee Stock Ownership Plans, as the name suggests, selling stock in your company to those employees who are already part of the organization. As a business owner, you may wonder how you can protect loyal employees after an exit. Certainly, a third-party sale leaves those who may have helped build your company alongside you vulnerable to termination or worse, the dissolution of their leadership role or disintegration of the company culture they helped build.

An ESOP not only protects loyal employees from termination but also gives them ownership of up to 100% of the company. From a tax perspective, ESOPs are valuable in that your seller notes earn on average 13% – 20% in contrast to the 6% average rate of return for stock market assets. When a business owner or owners sell to their employees, the transaction is tax-free. Here is an example of the structure of a cash sale vs ESOPS from The Menke Group:

“Let’s assume that the value of your company is $10 million and you decide to sell it to a third party for all cash. After paying a combined federal and state capital gains tax of say 30% (assuming a zero basis), you would be left with net proceeds of $7 million, which you could reinvest in […] public stocks that historically earn 6% on the average over the long term.

In comparison, if you are a C corp. […] you could sell your stock to an ESOP and receive $10 million in seller notes, tax-free, and your seller notes could earn an all-in rate of return ranging from 13% to 20% or more. Similarly, if you are a S corp. or switch to S corp. status, you could sell your stock to an ESOP in exchange for $10 million in seller notes, pay the capital gains tax on the installment sale basis and earn an all-in rate of return on your seller notes ranging from 13% to 20% or more.”

NCEO states that “ESOPS are most commonly used to provide a market for the shares of departing owners of successful closely-held companies, to motivate and reward employees, or to take advantage of incentives to borrow money for acquiring new assets in pretax dollars.”

Selling your business to a Third Party

For larger businesses (above $10 million in sale price) selling to a third party may be your best option. Larger sales often require the deep pockets of Private Equity PE) funds. Typically, larger companies have less concern for the future of their key employees. This may be because the owners have stepped away from the careful management of running of the business or because the hierarchy has become so stable that a purchasing entity would not touch the existing structure for fear of damaging the profitability of the acquired company.

The typical PE sale will give the seller a large portion of cash that they can allocate to whatever they wish. For example, they can give it to their family, buy a property, or invest as they wish without the long-term funds that accompany an ESOP. Being acquired by PE almost always means the owner stays on to ease the transition with a decreasing amount of influence over the subsequent 1-3 years.

Selling to a competitor can mean a lower sale price but likely the retention of your service offerings and potentially the merging of your company culture into the new entity.

From a tax perspective, selling to a third party means you will have to pay capital gains taxes on the full sale price of your company. For some sellers, this is a necessary evil and there are ways to offset those capital gains taxes such as:

An Installment Sales Agreement. An Installment sales agreement allows a buyer to pay a part of the sale price annually allowing them to adjust their annual income to maximize tax savings.

An Asset Sale keeps the company’s ownership in the hands of the seller to earn on the various components of the business as opposed to the entire business. In an asset sale, the seller may be able to write off the purchase more effectively though it leaves vulnerabilities for the seller.

“To buy the shares of a departing owner. Owners of privately held companies can use an ESOP to create a ready market for their shares. Under this approach, the company can make tax-deductible cash contributions to the ESOP to buy out an owner’s shares, or it can have the ESOP borrow money to buy the shares.

To borrow money at a lower after-tax cost. ESOPs are unique among benefit plans in their ability to borrow money.

To create an additional employee benefit. A company can simply issue new or treasury shares to an ESOP, deducting their value (for up to 25% of covered pay) from taxable income.

Major tax benefits. Some of these tax benefits include: contributions of stock are tax-deductible, cash contributions are tax-deductible, contributions used to repay a loan the ESOP takes out to buy company shares are tax-deductible, and sellers in a C corporation can get a tax deferral.”

Cons

The potential downside of ESOPs from NCEO include:

The law does not allow ESOPs to be used in partnerships or in most professional corporations.

ESOPs can be used in S corporations, but do not qualify for rollover treatment.

Private companies must repurchase shares of departing employees, which can become a major expense.

The cost of setting up an ESOP is substantial—$40,000 for the simplest plans.

Any time new shares are issued, the stock of existing owners is diluted.

Which is best for you?

ESOPS are complex structures as are sales of businesses to third-party buyers. While we can’t tell you which is right for you, the important aspect of a well-planned exit is a holistic view of the company, the owners’ wishes, and the timetable. As you plan for your company exit, please reach out to one of our trusted advisors to learn more about structuring an exit at 5 years, 3 years, and into the final 6 months before your sale.

As you look to plan for the future of both your personal finances and business finances, it’s important to understand what kind of financial assistance you may need. Understand the difference between a wealth manager and a financial advisor and which role is right for you in this blog.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1130829500.jpg14142121Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2021-11-28 17:16:002024-08-27 17:18:29ESOPs vs. Third Party Sale – What’s the difference?

The Los Angeles Times reported that “about $36 trillion will flow from one generation to another over the next 30 years.” This large amount of inheritance moving from one generation to another means more conversations surrounding money management. While this conversation may feel morbid and uncomfortable, it is essential to making sure your wealth remains after multiple generations.

How can you make this conversation about financial planning healthy and productive?

Timing

Environmental and personal factors can heavily influence how a conversation will go. Ideally, you will have prepared them that the conversation about wealth and inheritance is coming.

Bringing up the topic out of the blue may overwhelm your family members. Slowly starting to mention smaller financial topics while easing into the larger inheritance conversation can be extremely beneficial. Understanding when your family members are prepared to hear this conversation, and really understand the wealth that may be coming their way is essential.

It may be beneficial to introduce them to your wealth manager, so they can start having conversations with them about how to manage their inheritance.

Be Direct

Sometimes sugar coating a topic feels like it will help ease what might feel uncomfortable, however, being direct will actually help both you and your family in the long run. It’s important to make sure that you understand exactly what may be coming your way in terms of inheritance. Do they have a property in Wyoming that you don’t know about? It’s important that you don’t have any surprises coming your way during such an emotional time.

Understanding exactly what is included in your inheritance will also allow them to start planning on ways to continue to grow and build that wealth–– with the help of your family members. This introduction to your inheritance will help guide more conversations surrounding wealth management, investment strategies, and financial planning.

Succession Planning

For some families, inheritance means passing on a business.

The element of succession planning that rarely gets addressed is the emotional ties that the founder has to the organization. Letting go of the authority and importance of owning a business can be complicated.

Some of the key factors of planning for the transfer of power often require adding a third-party coach to the mix. In addition, planning for what the founder will do with their time after the transfer is often complicated. Some of the questions that might come up are:

What role will they have?

What influence will they have over decisions?

Who has veto power?

What retirement planning will be implemented for the founder?

How will company culture change?

One option is implementing an incremental transfer of power, meaning there is a plan in place to gradually decrease the founder’s involvement in the company over a period of time. Not only will this allow the founder to still feel connected to the company during the transfer, it will also allow the successor to learn from the founder’s experiences.

Ask for Advice

With age comes wisdom. It can be helpful to acknowledge that you respect and understand that you can learn from your aging family members.

Ask for advice on how they’ve managed their wealth and what plans they had in place for their financials in the future. This demonstrates that you want what’s best for their life earnings and family.

At Centura, we believe one of the key elements of liberating your wealth is planning in a way that unpacks your family’s values and dreams–– following an overall purpose. As you dive into your family’s finances, it’s important to understand what that purpose is, so you can carry on the tradition.

We Can Help!

At Centura, our process caters to your unique needs, therefore is well-adjusted to serve our audience. Just as important is our passion for finding and solving complex problems. Inherited wealth can be complex. Read more about how to understand the complexities that come with inherited wealth in this blog post.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1254013331.jpg14142121Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2021-10-16 17:44:002024-08-27 17:47:31How to Speak with Aging Family Members About Wealth and Inheritance

Professionals have compared structured notes to the innovative mindset behind mutual funds—with the main draw being zero interest rates. In the past, structured notes were a high-risk, high-return investment that only very wealthy investors could get involved in. Recently, however, the transition to using more technology for investing has opened the door for more individuals and families to invest using structured notes.

Centura Wealth Advisory works with clients to build a diversified portfolio when financial planning, and considering structured notes is a step toward having a more diverse portfolio.

Listen to the recent Live Life Liberated podcast, “Structured Notes Simplified with Robert Sowinski,” for a professional perspective.

What Are Structured Notes?

There are different types of structured notes that can be helpful to understand before investing.

There are a few categories to know for understanding structural notes:

Maturity

Underlying Asset

Protection Amount

Return/Payoff

Structured notes can be compared to a “hybrid security.” They combine the features of various financial products into one. Structured notes combine bonds and additional investments to offer the features of both debt assets and investment assets.

Structured notes aren’t direct investments, but derivatives. They track the value of another product. The amount on a structured note will depend on the issuer repaying the premium and underlying bond.

How do they work?

The basic ways structured notes can be ‘structured’ are the following:

Provide downside market protection

Provide upside (or enhanced) participation

Provide regular payments/income in the form of coupons if certain market conditions are met

Provide a payout/return at maturity if certain market conditions are met

The U.S. Securities and Exchange Commission (SEC) provides more detailed information on structured notes: “Structured notes have a fixed majority and include two components—a bond component and an embedded derivative.”

Financial institutions, as a result, are generally responsible for designing and issuing structured notes, so then the Broker/Dealer can sell them to individual investors.

Potential Risks

It’s important to understand that structured investments will not be a perfect match for all investors based on their risk profile and current portfolio. They are risky as your investments can sit idly without growth

The SEC lists the risks that come with investing in structured notes:

Market Risk

Insurance Price and Note Value

Liquidity

Payoff Structure (which is affected by participation rates, capped maximum returns, and knock-in feature)

Credit Risk

Call Risk

Tax Considerations

Talk to us!

If you’re interested in structured notes and diversifying your portfolio, speak to one of our trusted financial advisors today.

https://centurawealth.com/wp-content/uploads/2024/08/Should-You-Consider-Adding-Structured-Notes-to-Your-Portfolio.jpg14092128Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2021-09-05 17:57:002024-08-27 17:59:25Should You Consider Adding Structured Notes to Your Portfolio?

So… you want to sell your business. You’re not alone in the crazy market right now.

While there are many risks to owning a business, there are many reasons why you might be considering selling. Whether you are retiring, moving, or seeking new opportunities, here are some steps you can take to make this process as easy as possible.

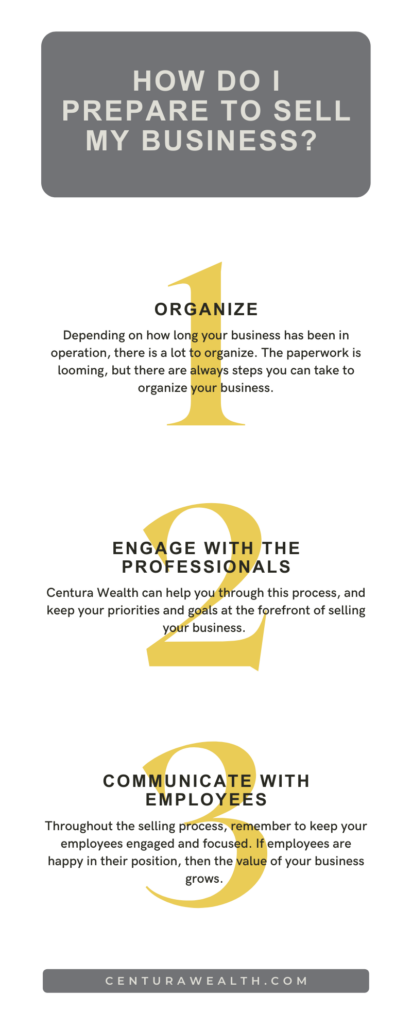

Organize

Depending on how long your business has been in operation, there is a lot to organize. The paperwork is looming, but there are always steps you can take to organize. In general, financial planning is always a great goal to have as a business owner.

Some documents to gather and organize include:

Tax returns

Three years worth of profit and loss (P&L) statements and balance sheets

Copy of current lease

An updated list of everything that will be sold from business

Contact and clients list

Sales transactions

A summary of monthly sales

After organizing these financial documents, the next step is to review them with your accountant.

Engage with the Professionals

Centura Wealth can help you through this process, and keep your priorities and goals at the forefront of selling your business. Mark Morris speaks to the importance of On the “Live Life Liberated” podcast by the Centura Wealth team. The podcast follows the one idea of minimizing your taxes — through the ING trust. Mark Morris highlights the following subjects for anyone looking to sell their business:

The major hurdles that the ING strategy helps you overcome

What the new California legislative proposal entails — and its implications, if it’s successfully passed

Why Mark strongly recommends that the sale of the business happens this year for optimal results, but options if it doesn’t

How to take advantage of the ING trust even if you don’t yet have a buyer for your business

Click here to learn more about the ING trust from a professional’s point of view!

Benefits

Besides making sure your business looks the best it can, there are various strategies you can follow to make smart decisions, including defined Benefit Plans (DB) and Defined Contribution Plans (DC).

Defined Benefit Plan

A Defined Benefit Plan (DB) is an “employer-sponsored retirement plan where employee benefits are computed using a formula that considers several factors,” according to Investopedia. These factors can include the length of employment and salary history.

With a DB plan, the general rule of thumb is that an employee cannot take out funds from their 401(k) plan.

Defined Contribution Plans

A Defined Contribution Plan (DC) on the other hand is, “a retirement plan that is typically tax-deferred like a 401(k) or a 403(b), in which employees contribute a fixed amount or a percentage of their paychecks to an account that is intended to fund their retirements,” according to Investopedia.

With a DC plan, participation by employees is voluntary.

Find a Trustworthy Buyer

Finding a buyer can be a lengthy process, but it’s worth waiting for the right fit for multiple reasons. Here are a couple of tips to be aware of when looking for a buyer:

Have multiple options as deals fall through all the time

Allow cushion room for negotiation

Keep your values top of mind—does this buyer follow them?

Keep potential buyers updated to help build trusty relationships

It never hurts to network

Communicate with Employees

Throughout the selling process, remember to keep your employees engaged and focused. If employees are happy in their positions, the value of your business grows.

Consider their perspective as an employee throughout the selling process. Telling them too early could cause confusion. Telling them too late can be offensive to the work they are doing. Timing is everything.

One of the key elements of liberating your wealth is planning in a way that unpacks your family’s values and dreams, following an overall purpose. This is a great perspective to have going forward after having a conversation with your parents.

For those who are interested in liberating their own wealth, please contact us at Centura Wealth Advisory today to see how we might partner!

Our process does not discriminate between uniqueness versus common and therefore is well-adjusted to serve our audience. Just as important is our passion for finding and solving complex problems.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/How-Do-I-Prepare-to-Sell-My-Business.jpg13382239Magdi Cookhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngMagdi Cook2021-07-31 18:05:002024-08-27 18:08:23How Do I Prepare to Sell My Business?

Opportunity Zones (O-Zones) are a unique product of the 2017 Tax Cuts and Jobs Act (TCJA). Since being introduced, opportunity zone investments (OZs) have been a hot topic for potential tax planning. So much so, it’s been reported that Qualified Opportunity Funds have raised over $6.7 billion thru December 2019, a number that grew at a rapid pace at the end of 2019 as taxpayers looked for ways to defer capital gains.

When it comes to O-Zone, tax breaks are the headliner, but the actual underlying investment within the Opportunity Zone shouldn’t be overlooked. Questions investors should ask include:

Where am I investing my money?

Are there enough good investment opportunities in this space?

Will the tax benefits be significant enough to outweigh an under-performing investment?

Would the investor be better off just paying the tax and re-investing in an investment of their choosing?

In this blog post, we’re going to dive into Opportunity Zones, which can be a hybrid tax planning and investment solution for those that have recognized a large capital gain. We’ll define the basics of the Opportunity Zones, discuss the tax benefits, compare O-Zones to other types of investments, and explore the characteristics of an investor that might consider an investment in a Qualified Opportunity Zone.

What is an Opportunity Zone?

The Tax Cuts and Jobs Act of 2017 brought about a new type of investment offering, Opportunity Zones, which provide a unique way of mitigating capital gains tax. The Opportunity Zones were created to incentivize investment of capital gains into low income or economically distressed communities. By investing in these communities, taxpayers may be allowed to defer capital gains when investing funds into a Qualified Opportunity Fund (QOF) and meeting other requirements.

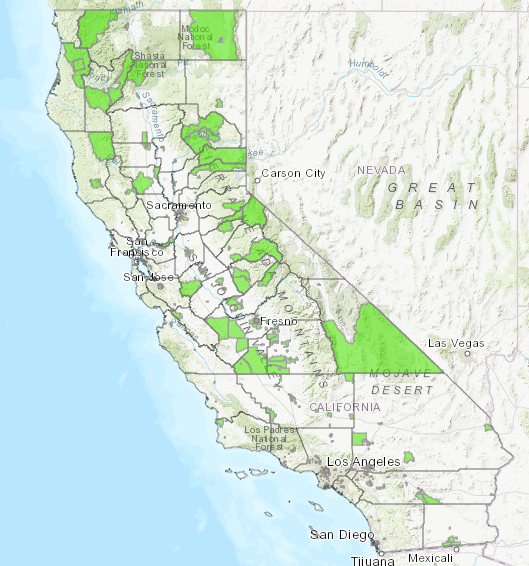

Check out the California Opportunity Zone map here.

What is a Qualified Opportunity Fund (QOF)?

A Qualified Opportunity Fund is an investment vehicle that files either a partnership (Form 1065) or corporation (Form 1120/1120S) federal income tax return and is organized for the purpose of investing in Qualified Opportunity Zone property.

What are the tax benefits of investing in a QOF?

There are three main categories for the tax benefits:

Deferral of a Capital Gain

Step-up in Basis of the deferred gain amount

Tax free gain on new Qualified Opportunity Fund growth

Deferral of Capital Gain

When a capital gain is recognized on the sale of an asset, you have the option to take any part of the capital gain and re-invest the proceeds into a Qualified Opportunity Fund (QOF). If the capital gain proceeds are re-invested into a QOF within 180 days of the gain being recognized, the dollar amount invested will be eligible for deferring the capital gain until the earlier of:

The tax year when the QOF interest is sold

Or December 31, 2026

At that time, the capital gain amount that was initially deferred when proceeds were invested into the QOF, would be recognized (less any step up in basis, see below) and taxes will be paid. The capital gain tax rate will be based on the tax rate applicable during the year the gain is eventually recognized.

Step-Up in Basis

If the investment in the QOF is held for at least 5 years, there is a 10% step-up in the basis of the deferred capital gain. If the QOF investment is held for 7 years, there is an additional 5% step-up in basis of the deferred capital gain (for a total of 15%). For those investing in 2020 and beyond, there will not be a 5% step up since it will be impossible to reach the 7-year holding period by 2026.

Tax free growth

If the interest in a QOF is held for 10 years or more, the post-acquisition gains in the QOF will be excluded on the sale of the QOF interest, thereby completely avoiding capital gains tax on this portion of the gain. There are several tax incentives that could be a big win for the long-term investor. However, taxes alone should never drive an investment decision, so let’s review a few of the primary risks associated with investing in a Qualified Opportunity Fund.

Risks Abound

The TCJA just put Opportunity Zones on the map in 2017, and as recent as December of 2019, the IRS published its final regulations on Opportunity Zones. The Qualified Opportunity Funds are new vehicles and due diligence is paramount. Investors will be facing questions of operator risk, investment risk, and illiquidity risk to name a few.

Operator risk– There won’t be an extended track record for any of the funds or operators. Are they putting the money to work in good opportunities that will net investors a positive return? Are they operating in compliance to meet the requirements of a Qualified Opportunity Fund?

Investment risk– While the Opportunity Zone rules do encourage more than just real estate development, it is likely that a lot of early projects will be in real estate development. Any real estate development project carries its own risks, not to mention that the developments will be located in Opportunity Zones, which by design are designated as an economically distressed area. As such, investing in these areas could carry additional risk(s) and expectation of returns should be scrutinized closely. Depending on the QOF, there could be single property risk if the fund has only invested in one project versus others that plan to invest in multiple projects.

Illiquidity – depending on the fund, the investment could be illiquid. To capture the tax benefits and defer the gain the maximum number of years, you would need liquidity elsewhere. This will be a 10-year investment if you want to hit the tax trifecta (deferred gains, step-up in basis, and future tax-free growth). If holding the QOF investment for ten years, the investor would also need to set aside cash to pay the initial capital gain tax that was deferred and recognized in 2026, so plan accordingly.

Is an Opportunity Zone Investment Worth Consideration?

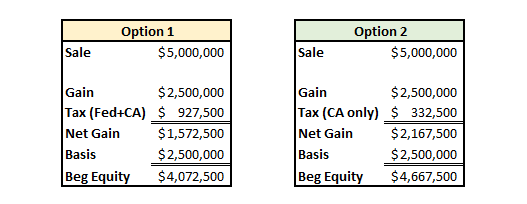

For comparison, we ran a hypothetical scenario to help evaluate the break-even return required by an investor that has captured a tax benefit from the Opportunity Zone (OZ) investment:

Option 1: Recognize capital gains on an investment, pay tax on those gains for Federal and California (assuming a California tax payer), and reinvest all the net proceeds (gain and basis) into a new investment

Option 2: Recognize capital gains on an investment, pay tax on those gains for California only, and reinvest the net gains in a Qualified Opportunity Fund while putting the basis in a new investment

It’s clear the Opportunity Zone investor has the beginning advantage with more capital to invest in year 1 (Option 2). A larger starting investment can compound at lower rates of return and still arrive at the same future dollar amount over 10 years. But, how much lower can the return be for the tax advantaged investor before the lackluster investment performance wipes out the tax advantages?

The goal here was to find the break-even return required from an Opportunity Zone fund to put the investor on par with just paying the tax and re-investing.

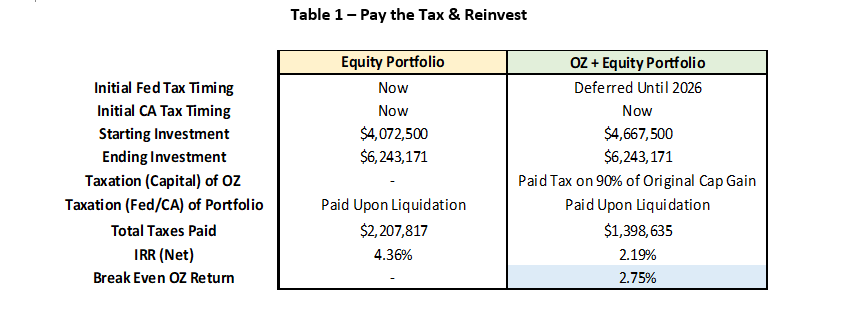

For the first scenario (Table 1), we assumed the investor paid the tax and re-invested the remaining proceeds into an equity portfolio with an expected return of 6.33% (see Capital Market Assumptions Blog). The Opportunity Zone investor invested the gain portion into a QOF and the basis in an equity portfolio. Assumptions are that all investments are liquidated at the end of ten years. The numbers are as follows:

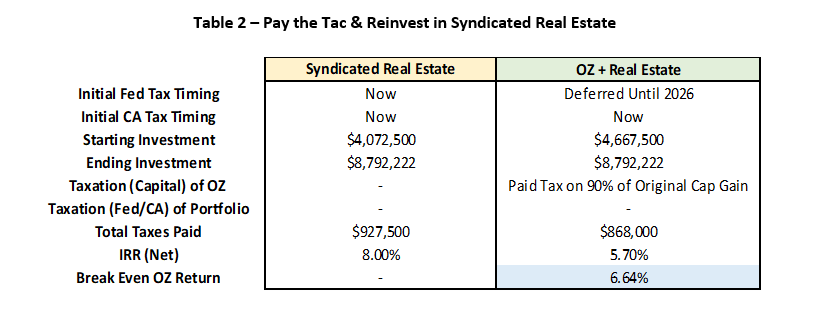

For the second scenario (Table 2), we assumed the investor paid the tax and re-invested the net proceeds into syndicated real estate that is expected to return 8%. The real estate investment has additional tax deferral options at the end of the ten-year holding period. It is still assumed that both options are liquidated at the end of ten years. The breakdown comparison of the options are shown below:

The QOF has merit when compared to paying the taxes and investing in an all equity portfolio. The break-even return required in the QOF of 2.75% (see Table 1) gives the investor a nice cushion provided by the tax savings. However, for accredited investors with the options to place funds within more sophisticated investment vehicles, the results become more convoluted. The QOF investor would require a break-even rate of return at 6.64% which is a much higher hurdle for an Opportunity Zone investment that carries many additional risks outlined earlier.

Conclusion

Let’s summarize where the Opportunity Zone seems to be an optimal solution.

At minimum, it’s an investor that has recognized or will be recognizing a significant capital gain. If the investor:

Has liquidity elsewhere to allow for a 10-year investment horizon in a QOF and liquid assets to pay the deferred tax due in year 2026

Would like to diversify a portion of their portfolio to real estate

Desires to invest money within economically disadvantaged areas for community/social benefits

Based on the comparison we modeled, if the motivation is strictly financial, an accredited investor in California (zero state tax benefits) with access to private syndicated real estate investment opportunities might just consider paying the tax and investing in a lower risk real estate investment. Instead of investing money in projects requiring development, existing properties with current cash flows may be a lower risk option.

Of the tax incentives, the ‘tax free’ growth on a new investment in an Opportunity Zone sounds appealing. However, real estate investments already allow for significant tax efficiency. Real estate investors can defer unrealized gains in future 1031 (IRC Section 1031) exchanges and heirs of real estate property receive a step up in cost basis at death.

In addition, certain types of real estate investments also allow investors to utilize depreciation to shield income from taxation; until exhausted or exchanged into a new property via 1031 exchange.

Given the existing tax efficiency and opportunity to invest outside of economically disadvantaged areas, private syndicated real estate has the potential to outperform a higher risk Opportunity Zone investment in the long run.

If you’ve incurred or will be incurring a significant capital gain and need help evaluating your options, contact Centura Wealth Advisory for a consultation.

Centura Wealth Advisory (“Centura”) is an SEC registered investment adviser located in San Diego, California. This brochure is limited to the dissemination of general information pertaining to Centura’s investment advisory services. Investing involves risk, including risk of loss.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/AdobeStock_75443283-scaled.jpeg14492560Christian Duranhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngChristian Duran2020-02-07 17:36:002024-08-20 17:43:41O-Zones (Opportunity Zones): Is the Juice Worth the Squeeze?

Given an ever-shifting market, it’s important to stay abreast of asset class expectations and how changes in market levels over time can help drive asset allocation decisions in an investment portfolio. In our first blog series on capital markets, we presented our forward-looking risk and return estimates. In this blog we will check current markets relative to our projections and illustrate how we use risk premiums to garner insights necessary for optimal portfolio recommendations. Keep reading to learn more about risk premiums, what they might mean for your portfolio and why now is a prudent time to take inventory of your asset allocation across your entire balance sheet.

Introduction

Both stock and bond markets are at or near all-time highs but historically these markets have not been correlated like they are today. In fact, the S&P 500 Beta for the Barclays US Aggregate Bond Index is -0.03 which indicates virtually no relationship between the change in price between stocks and bonds and suggests that price correlations will likely diverge at some point in the future. Thus, the question is not whether stocks or bonds will go up or down but whether stocks are cheap relative to bonds; and other assets like real estate. In order to solve this riddle, we can utilize risk premiums in different markets to evaluate which may be over/under valued. This blog post will examine current risk premiums in the stock and bond market(s) to assess relative valuations between the two and garner investment insights.

Risk Premiums – What are they?

Risk premiums represent the price of risk in different markets and investors can use them as a gauge of relative risk. They also reflect fundamental judgement about how much risk we see in an economy/market and what price we attach to that risk. The price of risk influences our asset allocation decisions as well as security selection within each asset class. The following are some (not all) factors that influence risk premiums:

Risk Aversion

Consumption Preferences

Economic Risk

Information

Liquidity and Fund Flows

Catastrophic Risk

Government Policy

Monetary Policy

Behavior

As seen in the list above, risk premiums are complex, and embedded in them is a significant amount of information. Fortunately, risk premiums can be extracted from market data which infers that the considerations above are baked in to prices. Utilizing market data allows investor’s to assess risk premiums relative to their own forward looking views and relative to other markets.

Investment implications

Before diving into the different risk premiums, it is important to lay the foundation for why looking at risk premiums matters. By comparing risk premiums, investors and practitioners can evaluate risk and returns on a relative basis and make investment decisions accordingly. The table below provides an overview of the relationship between different assessments of risk and the related market interpretation and investment action.

Table 1 – Risk Premium Assessments

Too High

Accurate

Too Low

Market Interpretation

Under Valued

Fairly Valued

Over Valued

Investment Action

Buy

Hold

Sell

Equity Risk Premium

The equity risk premium (ERP) represents the price of risk in equity markets and can be inferred as the expected excess return over the risk-free rate. For example, if the risk-free rate is 2% and equity markets are expected to earn 7% then the ERP is 5%. This risk premium is interpreted as the opportunity cost for investing in a market as well as the expectation of what that market will return, on average. Both considerations can be adjusted by volatility (standard deviation) to provide a risk adjusted comparison as well.

In our blog series on capital market projections, we forecasted US Large Cap Equity market returns of 6.33% over 10 years with volatility of 15.58%. If we utilize our current 10-year treasury yield of 1.64% we would derive an estimated ERP of 4.69%. However, in practice there are a variety of methods for utilizing market prices and other data to model and estimate the ERP. At Centura, we calculate the current ERP to be 5.65% which would imply that relative to our 10-year outlook, stocks are currently undervalued at today’s low interest rates and may represent an attractive long-term investment. With the ERP explained, we turn to the RP of debt (bond) markets, also known as Credit Risk Premium.

Credit Risk Premium

When it comes to evaluating the bond market, we typically look to the default spread between a bond and the risk-free alternative (e.g., Corporate bonds vs US treasuries) to estimate the credit risk premium (CRP). Default spreads are the market’s interpretation of credit risk premiums at different maturities, and the tighter spreads get the more overvalued the market becomes (see Table 1). Fortunately, the US Federal Reserve provides default spreads, and for Aaa and Baa corporate bonds relative to 10-year constant maturity treasuries (i.e., risk free rate) the current (as of September 2019) spreads are:

Aaa Corporate Bond Yield vs 10 yr treasury (constant maturity): 1.30%

Baa Corporate Bond Yield vs 10 yr treasury (constant maturity): 2.20%

At Centura, our capital markets projection for US Fixed Income is 3.49%, which versus the current 10-yr treasury yield of 1.64% represents a 10-year projected CRP of 1.85%. This implies that fixed income is priced efficiently with our long-term credit market forecasts.

Stocks vs Bonds

On a relative basis, at a blended CRP of 1.85% vs an ERP of 5.65%, bonds look expensive versus stocks. That said, at Centura we prefer to look at risk adjusted returns when comparing what it takes to earn that extra risk premium. For example, fixed income standard deviation is estimated to be 3.45% which when paired with a blended CRP of 1.85% begets a Sharpe Ratio of 0.54. Equity Market standard deviation is estimated to be 15.58% which when paired with an ERP of 5.65% equals a Sharpe Ratio of 0.36. Thus, on a risk adjusted basis bonds are more attractive than equities. So, what does all this mean?

Conclusion

In summary, at current market levels the equity risk premium (ERP) implies that equities are cheap relative to bonds. The ERP also implies that equities are cheap relative to our forward-looking capital market projections; whereas bonds look more efficiently priced based on our forward estimates. Thus, we are bullish on equities for the long term (i.e., 10+ years). While we are neutral on bonds, we recognize that they provide enhanced risk adjusted returns and can serve a vital role in portfolio management as they help steady returns. Additionally, they allow us to target specific risk/reward mandates.

At Centura, we construct portfolios of stocks, bonds and other alternative assets utilizing risk premiums to assess relative value between asset classes and intra asset class as well. Given the long bull run in risk assets over the past 10+ years, we at Centura feel that this is a prudent time to take inventory of holdings across your entire balance sheet to ensure your asset allocation is in line with your risk tolerance and portfolio objectives. If you self-direct your own portfolio, or are interested in a second opinion on your managed portfolio, contact Centura Wealth Advisory for a complimentary portfolio review.

Disclosures

Centura Wealth Advisory (“Centura”) is an SEC registered investment adviser located in San Diego, California. This brochure is limited to the dissemination of general information pertaining to Centura’s investment advisory services. Investing involves risk, including risk of loss.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure web site (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/AdobeStock_139544481-scaled.jpeg12582560Christian Duranhttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-Grey.pngChristian Duran2019-09-26 17:30:002024-08-20 17:34:32Risk Premiums and What They Mean for Your Portfolio