When it comes to estate planning, one of the key considerations for many individuals is how to retain control over their assets while minimizing the burden of income and estate taxes. ING Trusts offer a compelling solution that allows you to achieve both objectives.

In this blog post, we will explore the concept of ING Trusts, their benefits, and how they can help you preserve your wealth and secure your legacy.

Understanding ING Trusts

An ING Trust, also known as an Incomplete (Gift) Non-Grantor Trust, is a specialized type of irrevocable trust that offers unique advantages in terms of asset control as well as income and estate tax planning. Unlike traditional grantor trusts, where the grantor retains control over the assets and is responsible for the income taxes, ING Trusts shift both control and income tax responsibility to the trust itself.

Benefits of ING Trusts

Control over Assets:

By utilizing an ING Trust, you can maintain a significant level of control over your assets. You can guide the terms of the trust, such as how the assets are managed and distributed, while still enjoying the income tax benefits associated with transferring ownership to the trust.

Estate Tax Reduction:

One of the primary objectives of an ING Trust is to minimize gift and estate taxes. By removing assets from your taxable estate, while not utilizing any of your lifetime gift exemption, you can potentially reduce the estate tax liability upon your passing. This strategy can help ensure that more of your hard-earned wealth goes to your intended beneficiaries rather than to taxes.

Income Tax Reduction:

If structured correctly, assets transferred to the trust can be sold without paying the income tax that would otherwise be due in the settlor’s state of residence. In addition, ongoing earnings inside the trust can escape state income taxation. This can materially add to your long-term wealth.

Creditor Protection:

Another advantage of an ING Trust is the added layer of protection it provides against creditors. Assets held within the trust are shielded from potential claims, providing an extra level of security for your wealth.

Generation-Skipping Transfer Tax Planning:

ING Trusts can be particularly advantageous for individuals who wish to transfer wealth to future generations while minimizing the impact of the generation-skipping transfer tax. By structuring the trust appropriately, you can establish a lasting legacy for your family, ensuring that your assets are preserved for future heirs.

Before establishing an ING Trust, it is important to carefully consider the following factors:

Important Considerations with ING Trusts

Irrevocability:

One of the fundamental aspects of an ING Trust is its irrevocable nature. Once assets are transferred into the trust, they generally cannot be retrieved. This means that you need to thoroughly plan and ensure that the trust aligns with your long-term objectives. Take the time to evaluate your goals, preferences, and financial circumstances to ensure that an ING Trust is the right fit for your estate planning strategy. Understanding the permanent nature of the trust and its impact on asset control is essential for making informed decisions.

Professional Guidance:

Given the complex nature of estate planning and tax laws, seeking professional guidance is highly advisable when establishing an ING Trust. Consulting with an experienced estate planning attorney or financial advisor who specializes in ING Trusts can provide invaluable assistance throughout the process. These professionals have extensive knowledge of the legal and tax implications associated with such trusts and can offer personalized guidance based on your specific situation. They can help you navigate the intricate rules and regulations, ensuring that the trust is tailored to your unique circumstances. By working with experts, you can gain a comprehensive understanding of the benefits, risks, and alternatives, allowing you to make well-informed decisions that align with your goals.

Funding the Trust:

To fully leverage the benefits of an ING Trust, it is essential to properly fund it. Adequate assets need to be transferred into the trust to maximize tax efficiency and achieve your intended goals. This involves identifying and transferring assets such as business interests (primarily equity interest), investments, or other highly appreciated assetsd into the trust. Working closely with your estate planning attorney or financial advisor is crucial during this stage. They can help you determine which assets are suitable for the trust, considering factors such as asset valuations, potential tax consequences, and any restrictions or limitations associated with specific types of assets. By ensuring proper funding, you can maximize the tax advantages and ensure that your assets are effectively protected and distributed according to your wishes.

Impact of California Senate Bill 131 for CA Taxpayers

The State of California passed Senate Bill 131 (SB131) in July 2023 which was intended to foreclose the benefits of ING trusts to California taxpayers by making ING trusts “grantor” trusts. While this likely will mean that new ING trusts are not established in California, there is good news – for transactions that are already in motion, or for taxpayers that would like similar benefits, we can creatively deploy strategies such as an inter vivos qualified terminable interest property (QTIP) trust to accomplish many of the same objectives. This strategy is also available in states such as New York and Washington where similar restrictions exist or are being considered. While that is beyond the scope of this post, we would be happy to discuss the opportunities with you if you are in any of the “ING restricted” states.

Final Notes

ING Trusts offer a powerful tool for individuals seeking to retain control over their assets while minimizing income and estate taxes. By understanding the benefits and considerations associated with these trusts, you can make informed decisions to preserve your wealth and leave a lasting legacy for future generations. With professional guidance and careful planning, an ING Trust can become a cornerstone of your comprehensive estate plan, providing peace of mind and financial security for you and your loved ones.

Connect With Centura

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients with fully transparent reporting and tools to make informed decisions around their wealth plan.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1434132794.jpg12362426Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2023-07-30 18:44:002025-06-29 22:28:05ING Trusts: Control Your Assets and Minimize Income and Estate Taxes

Move over, FAANG! The Magnificent Seven have taken over the markets. Representing the seven largest companies in the S&P 500, Alphabet, Apple, Meta, Microsoft, Amazon, Tesla, and Nvidia have been anointed by investors as leading the market and tech rally.

The first half of 2023 was powered by mega-tech stocks, with the rest of the companies in the S&P 500 contributing an incremental amount to the indices’ return. The NASDAQ Composite registered its strongest first-half performance in 40 years, with Apple stock paving the way for an all-time high closing price on June 30, 2023 of $193.97, becoming the world’s first $3 trillion company.

Like the dot-com euphoria, artificial intelligence (AI) has offered tailwinds for the tech industry. AI has sparked big investments by companies and investors wanting to capitalize on the Generative AI race. Meanwhile, the June 1st debt ceiling ‘deadline’ was practically a non-event. The final agreement passed by the House and Senate suspended the debt limit until after the next presidential election and restricted government spending through 2025. However, that hasn’t stopped them from increasing the deficit. As the markets look past signs of economic cooling, indices push higher in the year’s second quarter.

Market Recap

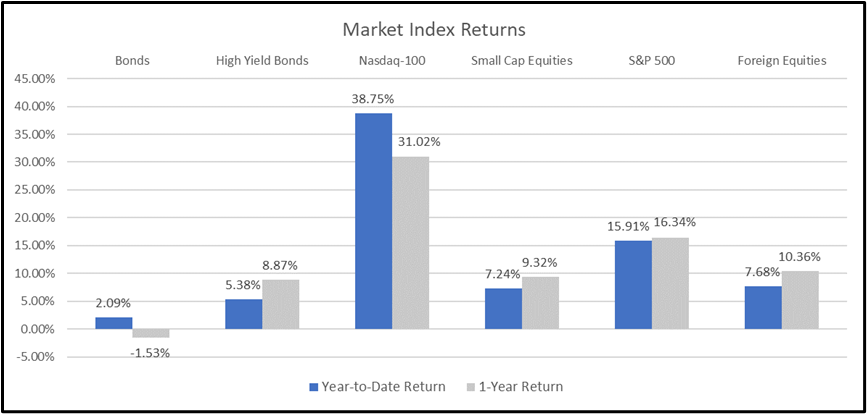

Equities – The Fed has remained steadfast in its fight against inflation, and the prospects of higher interest rates for longer have been unable to derail the tech-heavy NASDAQ 100 momentum, on its way to a second quarter return of 15.16%, bringing the index’s 2023 return to 38.75%.

Driven primarily by the returns of the index’s largest constituents, the S&P 500 has rebounded more than 20% since bottoming in late 2022, joining the bull market rally with the NASDAQ 100. Higher rates coupled with tighter financial conditions and more stringent lending standards have dampened the outlook for smaller companies. The small-cap Russell 2000 index has only gained 7.24% for the year, more than half of that occurring in the last week of the quarter.

While market participants expect the Fed to continue lifting rates and no longer anticipate a pivot this year, recent economic data and stronger earnings have given bulls optimism that a recession might be avoided. For now, with an eye on the future, it appears the market is discounting the lagged impact of monetary policy; gravitating to AI-centric companies; pushing interest-rate-sensitive equities higher; and creating a larger gap between market technicals and economic fundamentals.

Bonds – Bonds, on the other hand, have been sending conflicting signals. Driven by fears of a US government default and potential Fed-induced recession, bond volatility continued in the year’s second quarter, posting a -0.84% return; bringing the overall return on bonds to 2.09% in 2023. The current climate reminds us that while investing in ‘safe-haven’ Treasury securities removes credit risk, investors are still very much exposed to interest rate risk and ensuing volatility from changes in yields. Experiencing swings ranging from as high as 4.10% to as low as 3.37%, the yield on the 10-Year U.S. Treasury Note sits at 3.81%, or a mere 0.07% below where it started the year.

Source: YCharts. The Bloomberg US Aggregate Index was used as a proxy for Bonds; the Bloomberg US High Yield 2% Issuer Capped Index was used as a proxy for High Yield Bonds; the Russell 2000 Index was used as a proxy for Small Cap Equities; and the MSCI ACWI Ex USA Index was used as a proxy for Foreign Equities.

Despite declines in economic growth and activity, the economy has remained resilient as economists contend whether we are currently in or headed towards a recession.

Economy: What recession?

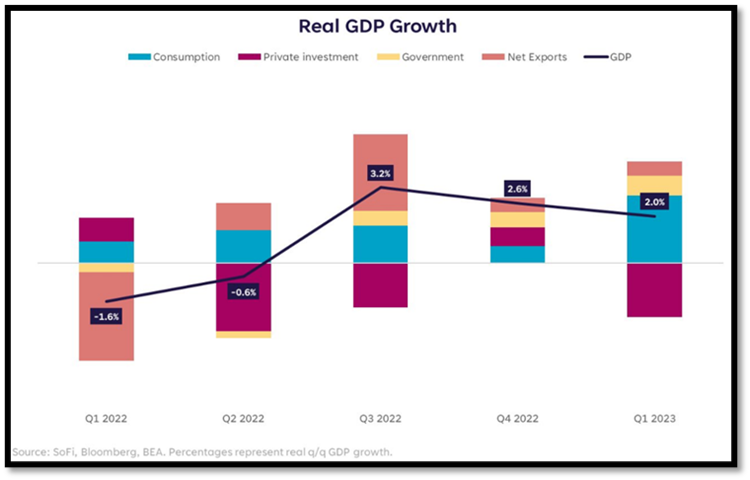

The economy continues to defy expectations and march higher in an environment with one of the most anticipated recessions in history. The last week of June delivered the final revisions to first-quarter GDP growth from 1.3% to 2%. Major gains came from robust consumer spending and surging exports, likely supported by the nearly 9% cost-of-living adjustment for Social Security participants. The 4.2% rise in consumer spending, as measured by personal consumption expenditures, was the fastest pace since the second quarter of 2021, and exports rebounded sharply, up 7.8%.

While Real GDP may be growing at a decent pace, several indicators point towards further contraction or possible recession.

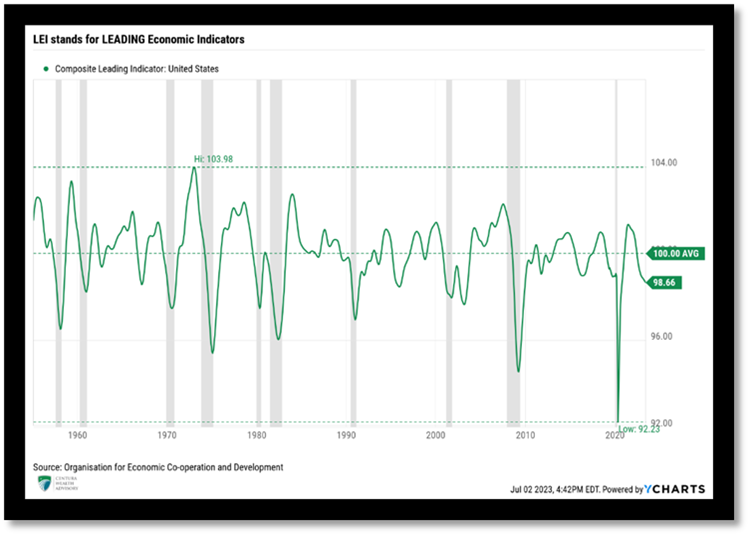

May marks the 14th consecutive month that the Conference Board’s Leading Economic Index (LEI) contracted, an early indication that a recession is all but certain. Senior Manager of Business Cycle Indicators at The Conference Board Justyna Zabinska-La Monica said:

“The US Leading Index has declined in each of the last fourteen months and continues to point to weaker economic activity ahead. Rising interest rates paired with persistent inflation will continue to further dampen economic activity. While we revised our Q2 GDP forecast from negative to slight growth, we project that the US economy will contract over the Q3 2023 to Q1 2024 period. The recession likely will be due to continued tightness in monetary policy and lower government spending.”

While Treasury Secretary Janet Yellen, President Joe Biden, and the Fed all believe a recession will be avoided, the question is not whether we will enter a recession but, rather, when and how deep the recession will be.

Inflation & Interest Rates

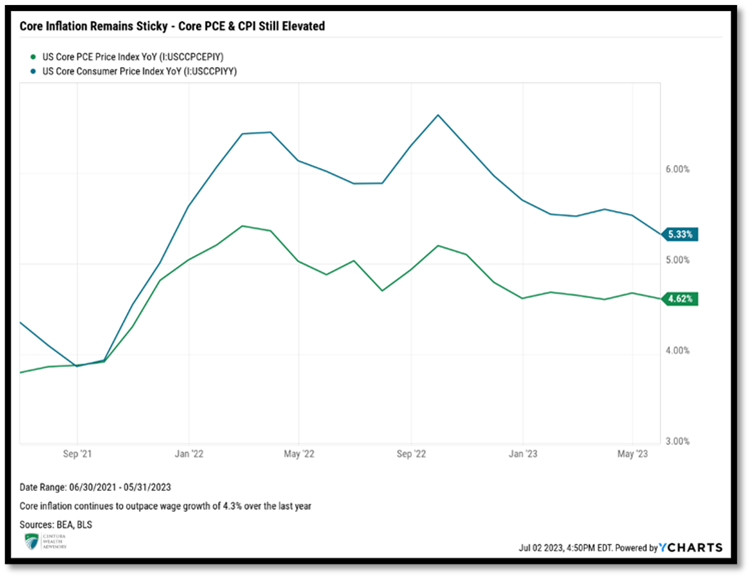

April and May’s headline Consumer Price Index (CPI) came in at 4.93% and 4.05%, respectively, while core CPI (excluding energy and food) registered 5.54% and 5.33% year-over-year readings over those same periods. The persistence of pricing pressure on core services, particularly shelter, has proven problematic. Shelter represents about 1/3 of CPI and has remained elevated, increasing 8% over the last year. Although the Fed’s restrictive monetary policy appears effective in bringing year-over-year inflation off its June 2022 peak of 9.06%, price pressures have proven painstakingly resilient and remain elevated more than the Fed prefers.

On a positive note, rents are coming down and home prices are off their June 2022 peak, indicating lower inflation readings ahead. While the downward trend in CPI is reason for optimism, we are more concerned with the Fed’s preferred inflation gauge, the Personal Consumption Expenditures (PCE), which has remained relatively flat at 4.62%, the same level reported in December 2022.

As highlighted in the previous quarterly market overview, uncertainty regarding the Fed’s inability to dampen inflation while avoiding an economic contraction has led to an almost certain harbinger of a recession: an inverted yield curve. Inverted yield curves occur when yields on longer-dated bonds are lower than yields on short-term notes and have proven to be solid predictors of recessions.

Debt ceiling negotiations, or lack thereof, consumed headlines through June. While the negotiations were essentially a non-event, one of the most meaningful outcomes has been the US government’s subsequent issuance of new debt since June 5th, which received little recognition in the media.

It was anticipated that a whopping $1 trillion of new Treasury securities would be issued by the end of the third quarter. Surprisingly, those estimates were off. The U.S. Treasury has already issued approximately $800 billion of new debt in less than a month, pushing the nation’s deficit beyond $32 trillion. Issuance of new securities serves as additional quantitative tightening to support higher yields and may lead to an equity pullback and widening of credit spreads according to both Citigroup and JPMorgan.

Don’t Expect a Pivot

True to their word, the Fed is committed to doing whatever is necessary to bring inflation back to its long-term target of 2%. In March 2022, the Fed embarked on its current Quantitative Tightening (QT) cycle, resulting in ten consecutive rate hikes over fifteen months and a federal funds rate of effectively 0% to 5%. During this period, Federal Reserve Chairman Jerome Powell additionally led the $95 billion per month balance sheet reduction, shedding approximately $625 billion since assets peaked in April 2022.

June’s Federal Open Market Committee (FOMC) meeting marked the first time since March last year that the FOMC voted not to hike rates further. The decision was telegraphed and highly anticipated. The Fed also conveyed that they are likely not finished raising rates, further tightening is likely required to lower inflation, and their June decision should be considered nothing more than a pause.

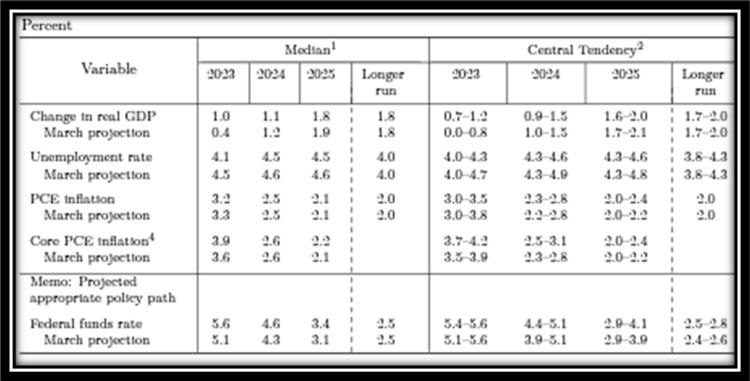

June’s FOMC release and updated economic projections showed a target peak Fed Funds rate of 5.6%, indicating another 0.50% of increases in 2023. Following the Fed’s June decision and updated Dot Plot, the market finally accepted our base case and what the Fed has been saying all along: rates will remain elevated to ensure inflation is under control. Barring a catastrophic event, no Fed pivot is expected in 2023. The first rate cut is now expected in early 2024.

One of the Fed’s primary concerns is wage growth. Although wage inflation has been trending lower, it remains elevated at 4.3%, which worries the Fed. Strong wage inflation increases the risk of a wage-price spiral that could prolong elevated inflation. While May’s CPI print showed headline CPI back below wage growth, core inflation measures remain higher, indicating that earnings are not keeping pace with cost-of-living increases.

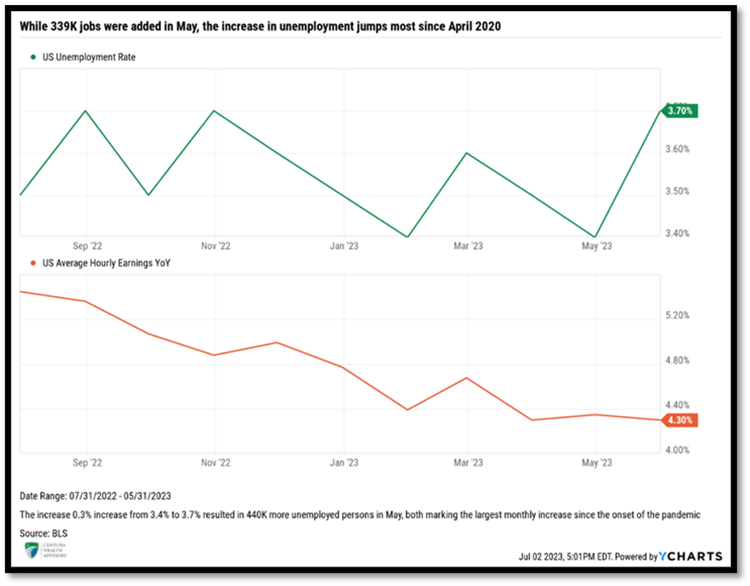

The labor market remains robust, despite some conflicting signals. May’s Labor Market Report registered the 29th consecutive month of job gains, though it showed signs of tightening. Estimates called for 195,000 jobs added in May and the market surprised to the upside with 339,000 jobs. Unemployment jumped 0.3% to 3.7%, marking the largest monthly bounce since April 2020. More than 440,000 people entered the unemployment market in May, also matching the largest monthly loss since the onset of the pandemic.

Surprisingly, as measured by the JOLTS, job openings unexpectedly reversed course and surged back over 10 million. Due to the higher number of unemployed, the ratio of job openings to those unemployed remained relatively flat at 1.65:1.

Centura’s Outlook

The Fed remains resolute in combatting 40-year high inflation, despite ‘pausing’ for a break, not letting concerns of a potential recession derail its tightening efforts. Interest rates remain at levels not seen since the Great Financial Crisis and will likely move higher over the next couple of months. The Fed’s goal to tighten financial conditions and slow the economy just enough to lower inflation back to their 2% mandate is a move that will likely force a recession.

Earnings for the first quarter were stronger than expected, leading many to believe higher rates and inflation aren’t wreaking as much havoc as initially feared. However, higher rates for longer periods spells lingering bank liquidity concerns and potential economic recession have prompted analysts to revise earnings forecasts lower.

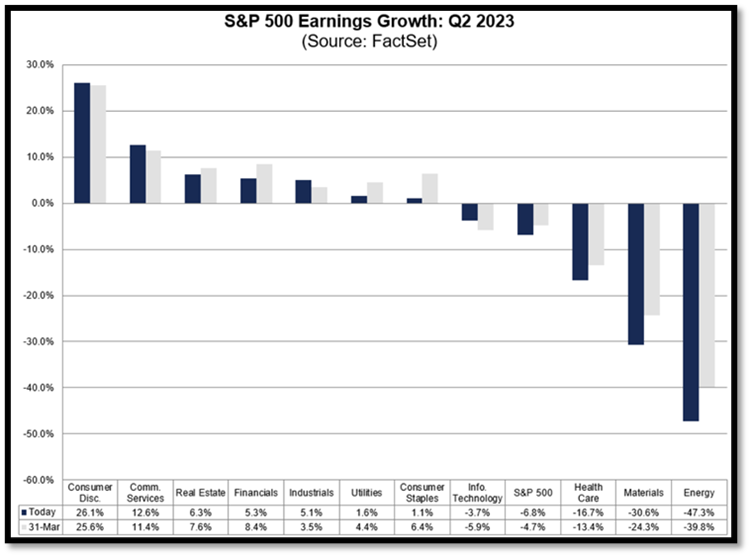

According to FactSet, the estimated earnings growth for the S&P 500 in the second quarter has been revised lower from the expected -4.7% in March to -6.8%. If accurate, this would represent the largest decline the index delivered since the second quarter of 2020 of -31.60%. These negative revisions highlight companies’ challenges in 2023 to produce profits. Given that higher rates are likely to persist, additional pressure may be applied over the coming quarters.

A company’s ability to service debt is negatively impacted by elevated rates. The road ahead will likely remain a challenge given the increased cost of labor and companies’ struggle to pass increased cost of goods onto consumers.

Forward 12-month P/E ratios have risen to approximately 18.9, slightly above their five-year average of 18.5. This indicates that equities are slightly overvalued and additional drawdowns may be in store before equities become attractive from a valuation standpoint. When banks kick off earnings season in mid-July, executive managements’ comments on the health of their companies’ and consumers’ balance sheets should prove insightful, particularly as it pertains to banks’ revisions to loan loss reserves. This should provide an indication of the direction and magnitude of companies’ future expected defaults, which we expect to increase.

Until inflation breaks lower, we remain cautious and anticipate that equities could experience turbulence in the second half of the year, particularly if inflation remains elevated or resurges. We also believe the market is discounting the impact of the Fed’s aggressive monetary tightening actions. Bankruptcies are quietly rising, and defaults are starting to tick up. As rates go higher, we expect further stress on companies and consumers.

Conversely, we also recognize that the market is forward-looking, often pricing in future economic recoveries before they occur and that investors are irrationally exuberant. While we do not subscribe to, or make investment decisions based on FOMO (Fear of Missing Out), it exists and can often be the catalyst a market needs to continue to push higher. Through our experience, we have found when a large disconnect between economic fundamentals and market technicals exists, we should consider shifting allocations towards our neutral strategic allocations.

Like many institutional investors, our cautious outlook has guided our allocations and we remain underweight to respective equity targets in client portfolios. [MT3] [CO4] Our quality bias, which served investors well in the angst of 2022, has served as a headwind in the first half of the year. Given the strength of the equity market recovery since late last year, we began bringing some of our equity positioning back toward our long-term target allocations. We intend to exercise caution while also monitoring opportunities to capitalize on any future market dislocations.

Our fixed-income allocation has seen a reduction in non-traditional fixed-income investments that served portfolios well, as interest rates rose sharply. With end-of-rate increases in sight, over the last several months, we have been extending duration and increasing the quality of underlying bonds, emphasizing U.S. Treasury and investment grade fixed income securities. At this stage in the cycle, we believe this positioning should provide long-term benefits to portfolios and be benefactors of a ‘flight to quality’ that may ensue with any equity market volatility.

We continue to succeed in improving returns and reducing risk by incorporating many private and liquid alternative investments into our allocations. Spiking interest rates have impacted private real estate, and we expect additional downward valuation adjustments across many sectors and markets. Our focus on real estate industries possessing a largely favorable supply/demand imbalance, like multifamily real estate, should help mitigate losses relative to other real estate sectors not possessing similar disparities. Despite the expected challenges in the real estate market, we maintain our dedication to exercising patience and selectivity in our decision-making process. For example, we are finding great opportunities in private credit. Most private credit is floating rate, possessing short durations and experiencing lower price sensitivity to spiking interest rates than similar public credit while also delivering a high-level of income production. We are beginning to observe defaults increase in the market, though they remain well below historical averages. With higher rates expected, additional pressure on borrowers’ ability to service debt will be applied. As such, our focus is on partnering with high-quality managers who have a proven track record of reducing loss. While we face significant uncertainties, we remain anchored by our core principles. Thank you for your continued confidence and support. If you have questions or concerns, please contact your Centura Wealth advisor.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on the market and other conditions. These documents may contain certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Centura Wealth Advisory is a registered investment advisor. Advisory services are only offered to clients or prospective clients where Centura Wealth Advisory and its representatives are properly licensed or exempt from licensure. 12255 El Camino Real, St. 125, San Diego, CA 92130.

Life insurance is an important consideration when it comes to securing your family’s financial future. In the event of your death, life insurance policies can provide financial protection to your loved ones, ensuring that they are taken care of in your absence. However, not all life insurance policies are created equal. For high net worth individuals, a private placement life insurance (PPLI) policy can offer unique advantages over traditional life insurance policies.

In this article, we’ll explore the differences between PPLI and traditional life insurance, and explain why PPLI may be the better choice for high net worth individuals & families.

Traditional Life Insurance

Traditional life insurance policies operate in a relatively simple manner. Policyholders pay a premium in exchange for a death benefit that is paid out to their beneficiaries when the insured dies. After premiums are paid, insurance charges are deducted and the net premium is invested in some sort of mechanism, dictated by the policy type. In the case of traditional variable universal life (VUL), this net premium is allocated to the carrier’s “segregated” account that is separate from the general account (thus not subject to the carrier’s creditors).

Limited Investment Pool

One of the main drawbacks of traditional VUL policies is that they limit investment choice to a pre-selected pool of options. Similar to the investment selection of a 401k menu, there are typically anywhere between 75-150 funds to choose from. Also, these funds do not include alternative style investments, thus limiting the potential growth of the cash value. As a result, traditional life insurance policies may not be an ideal option for qualified purchasers and/or accredited investors who are seeking to grow their wealth tax-efficiently and with more significant returns.

Accessibility

It’s essential to note that traditional life insurance policies are generally more accessible than PPLI policies, as they do not require nearly as significant investment upfront. However, traditional life insurance policies do not offer the same level of flexibility and customization over investment selection as PPLI policies.

PPLI (Private Placement Life Insurance)

Private placement life insurance (PPLI) policies operate in a similar manner to traditional life insurance policies. However, PPLI policies are specifically designed for serving as a tax efficient wrapper for tax inefficient assets.. Also, with a PPLI policy, the policyholder can invest in a separately managed account (SMA), which can be customized relative to the fixed menu of “off the shelf” offerings on the carrier’s platform. These SMAs can hold a range of investment types, including hedge funds, private equity, private credit and real estate to name a few.

Tax Efficiency

One of the most significant benefits of cash value life insurance policies is tax efficiency. PPLI policies allow policyholders to defer taxes on their investment gains and income while the policy is active. Additionally, PPLI policies can provide tax favored access to policy distributions, either by withdrawing up to cost basis tax free or utilizing tax free policy loans. The death benefit is also received tax free by the policy holder’s heirs.

Asset Protection and Estate Planning Benefits

PPLI policies can also offer asset protection and estate planning benefits. PPLI policies are typically structured to provide a level of asset protection, shielding investments from creditors and lawsuits. Additionally, PPLI policies can be designed to reduce estate taxes, providing a tax-efficient way to transfer wealth to the next generation.

PPLI vs. Traditional Life Insurance

When comparing PPLI and traditional life insurance policies, the key differences lie the investment flexibility, costs and liquidity. Since life insurance policies grow tax deferred, they trade off investment tax drag for insurance costs. Assuming the policies are designed properly, these insurance charges for the death protection are minimized and this can be a very favorable trade-off. PPLI amplifies this trade-off versus traditional coverage in two ways:

PPLI tends to have much lower upfront fees relative to traditional coverage

PPLI allows the underlying investments to be comprised of assets with higher return potential but that would normally come with higher tax drag. PPLI eliminates the tax drag while keeping the higher return potential

PPLI vs. Traditional Life Insurance: Which Is Right for You?

For high net worth individuals who seek to grow their wealth and manage their investments in a tax efficient manner with greater flexibility, PPLI policies may be the better option. However, PPLI policies require a significant investment upfront and may not be accessible to everyone.

If the goal is to minimize premiums paid for maximum death benefit coverage traditional life insurance policies can serve as a very effective tool for estate liquidity and generational wealth leverage for your loved ones. However, if you’re a high net worth individual looking to grow your wealth tax-efficiently, protect your assets, and provide ancillary estate planning benefits, a PPLI policy may be the better choice for you. By working with a knowledgeable wealth advisor, you can explore your options and make an informed decision that meets your unique financial goals and needs.

If you’re interested in learning more about PPLI and how it can help you achieve your financial goals, contact Centura Wealth Advisory today. Our experienced advisors can help you create a customized wealth management strategy that meets your needs and provides the protection and growth you deserve.

Connect With Centura

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients with fully transparent reporting and tools to make informed decisions around their wealth plan.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1188909800.jpg14142119Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2023-07-01 18:51:002025-06-29 22:28:48PPLI vs. Traditional Life Insurance: What’s the Difference?

San Diego, CA – Centura is proud to announce that Derek Myron, the company’s Managing Director, was featured in the recent wealth management roundtable organized by the San Diego Business Journal (SDBJ).

The roundtable discussion brought together eight of the region’s leading financial planners and wealth managers to share their expertise and advice on retirement planning and estate planning management.

Derek Myron’s Experience and Commitment to Helping Others:

With over 25 years of experience, Derek Myron has been serving high net-worth individuals and families since 1998, assisting them in the creation and implementation of carefully crafted plans to achieve both their financial and life goals. His dedication to helping others reach their highest potential, both professionally and personally, has been his guiding principle throughout his career.

Strong Foundation and Qualifications:

Growing up in a two-parent-teacher household that emphasized academic excellence and community service, Derek developed a strong foundation of values centered around education and helping others. He earned his undergraduate degree in Business Administration with a Finance concentration from the University of Washington and has held the Certified Financial Planner (CFP(R)) designation since 2001.

Passionate about Liberated Wealth® Plans:

Passionate about making a positive impact on his clients’ lives, Derek finds great joy in developing and implementing Liberated Wealth® plans for Centura Wealth Advsiory’s clientele. By facilitating an impactful change to their financial well-being, he helps them achieve their life goals with a focus on long-term prosperity.

The Great Retirement: Insights From Wealth Management Expert, Derek Myron

The latest issue of the San Diego Business Journal magazine’s Wealth Management section explores the challenges faced by Baby Boomers, the generation born between 1946 and 1964, who currently represent 28% of the U.S. population. With retirement rates rapidly accelerating, approximately 75 million Baby Boomers are expected to retire by 2030, marking a significant shift in the demographic landscape.

Top Concerns for Retirement Planning

As Baby Boomers approach or enter retirement, ensuring financial stability throughout their golden years becomes a paramount concern. Factors such as longer life expectancy, rising healthcare costs, and market volatility contribute to the complexity of retirement decisions. Navigating the financial path during retirement presents challenges that require careful consideration and expertise.

The Largest Intergenerational Wealth Transfer in History

In addition to retirement planning, Baby Boomers face the task of transferring wealth to their children, marking the largest intergenerational transfer of wealth in history. However, despite the magnitude of this responsibility, a majority of U.S. households lack sufficient plans in place to effectively manage this transition. Many individuals overlook the opportunity to seek guidance from wealth managers and financial planners who possess the expertise to structure comprehensive plans that facilitate the growth and management of wealth.

Let’s review Derek’s insights.

What potential challenges can arise during the transfer of a family business, and what are the associated complexities? When passing on a business, what are the primary goals to consider: fairness or equality?

Derek Myron explains the complexities associated with passing on a family business: “A family business can be extremely complicated to pass on and continue running after the death of the primary owner. This often arises due to family dynamics, disproportionate involvement in the business, and various other factors… Should it be passed on to those involved, benefiting them more than others? Or should it be divided equally… The right solution depends on the facts, circumstances, and preferences of the business and family. Proper business succession planning is crucial…”

What are common issues/problems heirs may encounter that wealth managers can help with?

Derek Myron sheds light on the issues heirs may face and how wealth managers can assist: “A good estate plan allows heirs to inherit wealth with help and support in how to manage it… Certain assets can pose challenges for heirs… Having a competent, experienced, and qualified financial advisor will help assess whether your current estate plan aligns with your goals and make necessary modifications as needed. They can also assist in setting up business succession plans, facilitating the sale of directly managed real estate assets, and transitioning into syndicated deals where management is delegated… without proper planning, wealth can become burdensome.”

What actions can be taken to Mitigate Tax Exposure in a Trust/Estate Plan?

Derek Myron provides insight on actions that can be taken to mitigate tax exposure in a trust/estate plan. He explains: “At present, gift tax and estate tax exemptions are around $13 million per individual and around $26 million per married couple… the exemptions will sunset on Jan. 1, 2026, back down to the level pre TCJA; adjusted for inflation… anyone with assets expected to exceed these estate tax exemption levels in 2026… should consider the design and construction of their current wealth transfer plans.”

Centura’s Ranking in San Diego Business Journal’s List of Wealth Management Firms

Centura Wealth Advisory has secured the notable position of #22 on the San Diego Business Journal’s list of wealth management firms. SDBJ’s list was ranked by assets managed locally for fiscal year 2022.

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients with fully transparent reporting and tools to make informed decisions around their wealth plan.

Read on to learn more about our 5-Step Liberated Wealth Process and how Centura can help you liberate your wealth.

Disclosures

Centura Wealth Advisory does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither attorneys nor accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

SDBJ’s Wealth Management list was ranked by assets managed locally for fiscal year 2022. The ranking should not be viewed as representative of any one client’s experience and should not be taken as an indication of performance by Centura and any of its clients. SDBJ requested Centura to participate in the special report. Centura paid a fee to participate in the special report.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1432326796.jpg14242106Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2023-06-16 18:41:002025-04-08 16:22:16Centura’s Managing Director, Derek Myron, Featured in San Diego Business Journal’s Wealth Management Roundtable

A PPLI policy can be a highly effective solution for both privately held business owners and high net worth individuals/families seeking tax efficient cash accumulation.

PPLI is an elegant type of variable life insurance contract that leverages the tax advantages of traditional coverage and provides access to a wider array of investment options. If structured properly, funds may be allocated across a highly customized pool of investments. Surplus premiums (premiums paid in excess of death benefit costs) are added to the policy cash value, growing tax deferred. PPLI can serve as an excellent strategy for mitigating ongoing income taxes, acting as a tax efficient wrapper for assets that:

Generate high levels of tax inefficient income, such as private credit or high-turnover hedge funds.

Are expected to significantly increase in value within the foreseeable future, and will ultimately be prepared for disposition.

Typical PPLI Candidate:

Net worth of $10 million or greater

Access to significant liquidity

Ability to fund $2-$5 million, cumulative within the first five years

Appetite for alternative style investments

Desire for sophisticated income tax & wealth transfer planning

Common Investments Inside PPLI Include:

High Turnover Hedge Funds

Private Credit

Direct Lending

Real Estate

Private Equity

Traditional Mutual Funds

Investment Customization Vehicles Include:

Off-the-Shelf Platform Funds (predetermined fixed menu of VITs & IDFs already available)

Institutional Pricing (typically < 100 bps per annum)

Trades investment tax drag for costs of insurance

No Surrender Charges

Favorable Policy Lending Terms

PPLI Discovery Process

The financial advisor and client collaborate to determine the client’s investment objectives, risk tolerance, as well as income tax & estate planning needs.

A risk/return analysis is conducted. The financial advisor works with the client to create a customized policy that meets their specific investment goals and tax planning needs. It includes review of cost to set-up and administer.

PPLI Policy in Action

Initial Set UpGrantors draft an irrevocable trust that will own a life insurance policy.

Contribution of FundsFunds are contributed to the trust, which are used by the trustee to purchase a PPLI policy.

InvestmentLiquid funds are allocated to various investment options within a separate account managed by an independent financial advisor.

Tax Favored Access to Policy ValueOver time, any investments acquired in the account grow tax-free. The policyholder can access funds tax-free by taking loans against the policy’s cash value. Upon policyholder’s death, the death benefit is paid out tax free to beneficiaries named in the policy.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1457585755.jpg13792173Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2023-06-15 18:49:002025-04-08 16:43:27Private Placement Life Insurance (PPLI)

Private Placement Life Insurance (PPLI) is a financial tool that offers unique benefits for high net worth individuals. PPLI is a form of life insurance designed for accredited investors and qualified purchasers, providing a broad range of investment options with significant tax advantages.

In this article, we will explore the benefits of PPLI and compare it with traditional life insurance coverage.

What is PPLI?

In a nutshell, PPLI serves as a tax efficient wrapper for tax inefficient assets. It is essentially a tailored variable universal life insurance policy that is offered exclusively to accredited investors and qualified purchasers, allowing for a wider array of investment options that can include alternative style investments (i.e., such as private equity, private credit, hedge funds, etc..). These policies are treated as private offerings that when structured properly, can be highly customized to suit the policy holder’s needs & investment philosophy. PPLI is often designed as a highly tax efficient investment vehicle that provides tax-deferred growth on the policyholder’s underlying investments as well as tax favored distributions from the policy.

How Does PPLI Work?

The Mechanics of PPLI:

PPLI operates similarly to cash value universal life insurance contracts. It provides a death benefit to beneficiaries when the insured passes away. The policyholder pays an insurance premium, which, after deducting insurance fees, is allocated to an investment mechanism that generates a cash value component. The growth of this cash value depends on the net performance of the underlying investments and the deduction of ongoing insurance charges. If the investment performance exceeds the policy charges in a given year, the cash value increases. As long as the cash value remains above zero, the policy remains active.

Maximizing Premiums within IRS Limits:

In PPLI, policyholders often pay the maximum allowable premium relative to the death benefit set by the IRS. This approach minimizes the costs associated with insurance protection (death benefit). With proper asset management, the tax-deferred investment performance within the policy tends to outperform the costs of insurance over time. When comparing similar investment strategies outside of PPLI, policyholders make a trade-off. They trade the tax drag on investments outside the policy for the insurance fees within the policy. When structured correctly with suitable investments, this trade-off favors the “tax efficient” PPLI vehicle, with insurance charges minimized compared to outside investment tax drag.

Segregated Account and Investment Options:

Since PPLI falls under the category of variable universal life insurance, the net premium is allocated to the carrier’s segregated account, separate from the general account and protected from creditors. The segregated account consists of various pre-determined investment options provided by the carrier, including a range of alternatives. These options are fixed or locked-in, similar to investment offerings in a 401K menu. However, the inner workings of the segregated account can be highly customized by utilizing separately managed accounts (SMAs), creating customized insurance dedicated funds (IDFs), or a combination of both.

By understanding the mechanics of PPLI and utilizing the flexibility offered within the segregated account, individuals can optimize their tax efficiency while protecting their assets and beneficiaries.

PPLI vs. Traditional Life Insurance: What’s the Difference?

Traditional Life Insurance

Permanent life insurance (regardless of PPLI or traditional) provides a death benefit to beneficiaries upon the policyholder’s death. It also offers the following four tax advantages (assuming Non MEC status):.

Tax deferred growth of underlying investments (i.e., cash value)

Ability to withdraw funds tax free, up to the cost basis in the policy

Ability to loan from the policy tax free, via direct carrier loan or pledge the policy for collateral (VUL & PPLI policies will have more stringent collateral requirements relative to fixed insurance products such as Whole Life)

Death proceeds are received income tax free to the beneficiaries

Traditional life insurance has several limitations, such as limited investment options, higher relative fees, and inflexibility. With traditional VUL, policyholders are restricted to investing in a limited number of funds chosen by the insurance company. As a result, they miss out on the potential for higher returns that alternative investments can offer. Traditional life insurance also tends to have higher upfront fees and expenses that can eat into the policy’s returns and delay a positive return on investment. Finally, traditional life insurance policies are less flexible and often include surrender charges.

PPLI Investment Flexibility and Tax Efficiency

PPLI, on the other hand, offers a range of investment options with tax-deferred growth. Policyholders can allocate their investments to various asset classes, including private equity and hedge funds. This offers PPLI a significant tax advantage over traditional life insurance as policyholders can invest in a range of assets that offer higher growth potential, without taking on the added tax drag often associated with some of those investment classes. This makes PPLI an attractive option for those looking to minimize their tax liability.

How PPLI Supports Tax-Efficient Financial Planning

Asset Protection and Estate Planning Benefits

Asset protection and estate planning benefits are significant advantages of PPLI policies. One of the primary benefits of PPLI is its ability to provide maximum asset protection. By shielding assets from potential lawsuits and creditors, PPLI policies can help protect the wealth of high net worth individuals who are at greater risk of being sued. This protection is possible when the policy is owned by an irrevocable trust, assuming the policy holder is not a named beneficiary (unless drafted in a self-settled spendthrift state)

Estate Planning Benefits

PPLI can also be an effective tool for estate planning. Policyholders can transfer their wealth to future generations while minimizing estate taxes by using PPLI. The policy is held in an irrevocable trust outside the taxable estate, and when the insured(s) passes away, the death proceeds are paid out to their beneficiaries free of income and wealth transfer tax. This influx of liquidity can then be used for estate taxes. Additionally, PPLI policies can be structured to allow for gifting to beneficiaries, which can further reduce the policyholder’s taxable estate. This can be particularly beneficial for individuals with large estates who want to ensure their assets pass on to their heirs in a tax-efficient manner.

Tax Benefits

As previously mentioned, the tax benefits of PPLI make it an attractive option for high net worth individuals looking to invest in a tax-efficient manner. One of the key benefits of PPLI is tax-deferred growth. Policyholders can invest in a range of assets, and any gains on these investments are deferred from taxes until the policy is surrendered (not taxed at all if planned appropriately).

Good and Bad Investments for PPLI

While PPLI offers a range of investment options, it is important to not only choose investments that are suitable for the policyholder’s investment objectives and risk tolerance, but also balance in investments that tend to generate unfavorable taxable income while also providing the potential for attractive returns. These include private credit, high turnover hedge funds, direct lending, private equity, etc. However, there are also various risks associated with certain investments. For instance, investing in hedge funds may lead to high mgt. fees and volatility. Private equity investments may also be risky due to the lack of liquidity and potential for significant losses. It is important to conduct due diligence and carefully evaluate the risks associated with each investment before making a decision.

Connect With Centura

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients with fully transparent reporting and tools to make informed decisions around their wealth plan.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1475002191.jpg14142121Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2023-06-09 18:52:002025-06-29 22:30:59The Role of PPLI in Tax-Efficient Financial Planning

Investing in the stock market can be an exciting and rewarding experience, but it can also be unpredictable and risky. One way to mitigate risk is to have a diversified portfolio, which means investing in a variety of different assets to spread out risk.

In today’s volatile market conditions, diversification is more important than ever to protect your investments.

Diversification: A Key Strategy for Mitigating Risk in Your Portfolio

Diversification is a crucial strategy for mitigating risk in an investment portfolio. By spreading investments across different asset classes, investors can reduce the overall risk and increase the potential for long-term returns. This section explores the significance of diversification and its benefits.

Understanding Asset Classes

To effectively diversify a portfolio, it is essential to understand different asset classes. Asset classes represent different types of investments, each with its own risk and return characteristics. This section provides an overview of some common asset classes and their roles in diversification.

Stocks

Stocks represent ownership shares in publicly traded companies. They offer the potential for high returns but also come with a higher level of risk. Stocks are influenced by various factors, such as company performance, industry trends, and overall market conditions.

Bonds

Bonds are debt instruments issued by governments, municipalities, or corporations to raise capital. They are considered relatively safer investments compared to stocks and typically provide regular interest payments. Bonds are influenced by interest rates, credit ratings, and the financial stability of the issuer.

Real Estate

Real estate investments include residential, commercial, and industrial properties. They offer potential income through rental payments and the possibility of appreciation in property value. Real estate investments can diversify a portfolio by providing a different source of returns and a hedge against inflation.

Commodities

Commodities include physical goods such as precious metals, oil, natural gas, agricultural products, and more. Investing in commodities can provide diversification as their prices tend to have low correlation with traditional financial assets. They can serve as a hedge against inflation and provide opportunities for portfolio diversification.

The Benefits of Diversification

Diversification offers several advantages to investors, enabling them to manage risk and potentially enhance portfolio performance. This section explores the benefits that diversification provides.

Risk Reduction

Diversification helps reduce the overall risk of a portfolio by spreading investments across different asset classes. When one asset class experiences a decline, others may perform well or remain stable, helping to offset potential losses. By diversifying, investors can minimize the impact of any single investment’s poor performance on their overall portfolio.

Enhanced Stability

A diversified portfolio is typically more stable than one concentrated in a single asset class. Different assets tend to have varied responses to market conditions. While some investments may be affected negatively, others may be less influenced or even benefit from changing economic circumstances. This stability provides a cushion against extreme market fluctuations.

Capital Preservation

During market downturns or financial crises, a diversified portfolio can help protect investors’ capital. By including assets that tend to have a low correlation to the market, investors can reduce volatility of their portfolio. For example, in the 2008 financial crisis, investors with diversified portfolios were better positioned to weather the storm compared to those heavily concentrated in a single asset class.

Potential for Increased Returns

Diversification offers the potential for increased returns by exposing investors to different sources of growth. While some asset classes may underperform in certain market conditions, others may thrive. By diversifying across various asset classes, investors can tap into opportunities presented by different market cycles and potentially achieve better risk-adjusted returns.

The Importance of Rebalancing Your Portfolio in a Volatile Market

While diversification is an essential strategy for mitigating risk, it’s not a set-it-and-forget-it strategy. Investors need to regularly rebalance their portfolios to maintain their desired asset allocation. This means periodically selling some assets that have performed well and buying assets that have underperformed. Rebalancing helps to ensure that your portfolio remains diversified and aligned with your risk tolerance and investment goals.

In a volatile market, rebalancing can be especially important. For example, if the stock market experiences a significant decline, your portfolio may become more heavily weighted toward bonds, which may not be aligned with your risk tolerance. Rebalancing can help you maintain your desired asset allocation and potentially avoid significant losses.

How Centura’s Customized Investment Plans Help Clients Manage Risk and Achieve Their Financial Goals

Centura is a financial advisory firm that offers customized investment plans to help clients manage risk and achieve their financial goals. Centura’s team of experts works with each client to develop a personalized asset allocation strategy based on their unique financial situation, risk tolerance, and investment objectives.

One of the key benefits of Centura’s customized investment plans is ongoing monitoring and adjustment. As market conditions change, Centura’s team constantly monitors each client’s portfolio and adjusts their asset allocation to ensure it remains aligned with their objectives. This helps clients stay on track to meet their financial goals while also minimizing risk.

Centura’s investment plans have helped many clients achieve their financial objectives. For example, one client came to Centura with a desire to retire early and travel the world. Centura worked with the client to develop a plan that would help them to reach their goal within 10 years. Through a combination of diversified investments and ongoing monitoring and adjustment, the client was able to retire on schedule and embark on their dream adventure.

Strategies for Protecting Your Wealth During Market Downturns

Market downturns are an inevitable part of investing, but there are strategies that investors can use to protect their wealth during these periods. This section discusses some effective strategies for safeguarding investments during market downturns.

Hedging

Hedging is a strategy that involves investing in assets that move in the opposite direction of the market. By holding positions that counteract the losses in the rest of the portfolio, investors can offset some of the downturn’s impact. Common hedging instruments include options, futures contracts, and inverse exchange-traded funds (ETFs). However, it’s important to note that hedging strategies also come with their own risks and costs, and they may not provide complete protection against losses.

Stop-Loss Orders

Stop-loss orders are instructions to sell a security when it reaches a predetermined price. By setting stop-loss orders, investors can limit their potential losses by automatically selling the asset if its price falls below a certain threshold. Stop-loss orders help protect against further declines in the stock price and can be a valuable risk management tool during market downturns. However, it’s essential to set appropriate stop-loss levels, taking into account volatility and individual risk tolerance, to avoid triggering unnecessary sales.

Defensive Investing

Defensive investing involves seeking out companies or sectors that are less vulnerable to economic downturns. These companies typically have stable earnings, strong cash flows, and reliable dividends, even during challenging market conditions. Defensive sectors often include utilities, healthcare, consumer staples, and essential services. By allocating a portion of the portfolio to defensive investments, investors can potentially cushion the impact of market volatility and protect against significant losses.

Effective Implementation and Professional Guidance

Implementing these strategies effectively requires careful consideration and understanding of individual investment goals and risk tolerance. Working with a financial advisor can help ensure that these strategies align with your specific circumstances and objectives. A professional can provide valuable insights, monitor market conditions, and make adjustments to the portfolio’s risk management strategies when needed.

Maintaining a Long-Term Perspective

During market downturns, it’s crucial to stay calm and maintain a long-term perspective. It’s natural to feel uneasy during periods of market volatility, but panic selling can lead to significant losses. History has shown that markets tend to recover over time, and selling during a downturn can lock in losses and prevent investors from benefiting if they don’t reinvest before subsequent market rebounds. By focusing on a long-term investment strategy, maintaining a diversified portfolio, and managing risk effectively, investors can better weather market volatility and position themselves for long-term success.

In conclusion, protecting wealth during market downturns requires thoughtful strategies and a disciplined approach. Hedging, using stop-loss orders, defensive investing, and seeking professional guidance are some effective strategies to mitigate losses and safeguard investments. Additionally, maintaining a long-term perspective and avoiding panic selling are vital for preserving wealth and achieving financial goals.

Final Notes

Diversification is a key strategy for mitigating risk in your portfolio. Creating a diversified portfolio by investing in a variety of different assets, you can spread out risk and potentially benefit from different market cycles. Rebalancing your portfolio is also important to maintain your desired asset allocation and potentially avoid significant losses during market downturns.

Centura’s customized investment plans can help you manage risk and achieve your financial goals by offering ongoing monitoring and adjustment. While there are other strategies for protecting your wealth during market downturns, it’s important to implement them effectively and stay calm during market volatility. By working with a financial advisor and staying disciplined, you can potentially achieve long-term success in your investments.

Connect With Centura

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients with fully transparent reporting and tools to make informed decisions around their wealth plan.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2024/08/iStock-1365412652.jpg12992309Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2023-05-25 18:56:002025-06-29 22:23:41Diversification: A Key Strategy for Mitigating Risk in Your Portfolio

Financial planning is crucial for individuals and families with high net worth. These individuals often have complex financial situations that require specialized expertise to manage effectively. Without proper planning, high net worth individuals may struggle to achieve their long-term financial goals. However, financial advisors face unique challenges when planning for these clients. This is where holistic planning comes in.

Holistic Planning: A Comprehensive Approach

Holistic planning is a comprehensive approach to financial planning that involves a combination of different components, including cash flow planning, goal-based planning, portfolio management, income tax planning, and wealth transfer planning.

Unlike an isolated approach to financial planning (for example, an approach in which there are a larger number of providers working in silos to provide expertise), holistic planning takes into account the big picture, considering how different aspects of financial planning impact each other and bringing that expertise under one roof.

This ensures that any recommendation made on one piece of the financial plan will likely affect other areas as well. Holistic planning is particularly beneficial for high net worth individuals and families, as it helps to manage the complexity of their financial situation effectively.

Benefits of Holistic Planning

Holistic financial planning offers several benefits to high net worth individuals and families. Let’s take a look.

Customized Approach to Financial Planning

One of the most significant advantages is the customized approach to financial planning that it provides. This approach is tailored to the unique needs of each client, taking into account all aspects of their financial situation. By doing so, advisors can create a plan that maximizes their client’s wealth and minimizes their tax liability. This results in a more efficient use of resources and a higher probability of achieving long-term financial goals.

Tailored Tax and Wealth Transfer Planning

In addition to customized planning, holistic financial planning ensures that all aspects of a client’s financial situation are considered. This includes income tax planning and wealth transfer planning, which are often outsourced by advisors to other professionals. By incorporating these elements into the planning process, advisors can create a comprehensive financial plan that considers the interplay between different aspects of the client’s financial situation. This approach can help clients to achieve a better understanding of how their financial decisions impact their overall financial health.

Focus on Long-term Goals and Legacy Planning

Holistic financial planning also places a strong emphasis on long-term goals and legacy planning. This means that advisors work with clients to ensure that their financial plan aligns with their long-term objectives, such as retirement or legacy planning. By doing so, clients can have peace of mind knowing that their financial future is secure and that their assets will be managed in a way that aligns with their values and long-term goals. This approach can also help to minimize the emotional and financial impact of life events such as divorce, death, or disability.

Risk Management

Finally, holistic financial planning can help clients to manage risk and navigate uncertainty. By taking a comprehensive approach to financial planning, advisors can help clients to identify potential risks and develop strategies to mitigate them. This can include everything from investment risk to estate planning risk to market risk. By having a plan in place that considers these risks, clients can feel more confident about their financial future and be better equipped to handle unexpected events.

For ultra high net worth individuals and families, the approach to financial planning is quite different from traditional financial planning.

Holistic planning is becoming increasingly important for ultra-high net worth individuals and families, as traditional financial planning approaches often fall short in addressing the complexity and high stakes involved in managing their wealth. Rather than focusing on individual pieces of the puzzle, holistic planning takes into account the big picture.

According to Sean Clark, MBA Director of Financial Planning at Centura Wealth Advisory, this approach involves pairing all the different parts of financial planning with income tax planning, wealth transfer planning, and balance sheet optimization. By understanding how all the parts work together and move, holistic planning ensures that any recommendation made on one piece of the financial plan will likely affect other areas as well. This comprehensive approach to financial planning helps identify small adjustments, such as debt or where an asset is held or titled, that can make a big difference in maximizing wealth and minimizing tax liability.

The Centura Approach

At Centura Wealth Advisory, we understand the unique needs of ultra high net worth individuals and families when it comes to financial planning. Our team of experts is well-versed in all areas of financial planning, including income tax planning and wealth transfer planning, and we work closely with our clients to develop a customized plan that addresses all aspects of their financial situation. Our comprehensive and integrated approach to financial planning ensures that every recommendation made on one piece of the financial plan takes into account its impact on other areas as well.

By adopting this approach, we help our clients achieve their long-term financial goals. Therefore, at Centura Wealth Advisory, we strongly believe that holistic planning is essential for high net worth individuals and families to secure their financial future.

Connect With Centura

At Centura Wealth Advisory, we go beyond a traditional multi-family office wealth management firm to offer advanced tax and estate planning solutions which traditional wealth managers often lack in expertise, knowledge, or resources to offer their clients.

We invest heavily into technology and systems to provide our clients with fully transparent reporting and tools to make informed decisions around their wealth plan.

Centura Wealth does not make any representations as to the accuracy, timeliness, suitability, or completeness of any information prepared by any unaffiliated third party, whether linked to or incorporated herein. All such information is provided solely for convenience purposes and all users thereof should be guided accordingly.

We are neither your attorneys nor your accountants and no portion of this material should be interpreted by you as legal, accounting, or tax advice. We recommend that you seek the advice of a qualified attorney and accountant.

For additional information about Centura, please request our disclosure brochure as set forth on Form ADV using the contact information set forth herein, or refer to the Investment Adviser Public Disclosure website (www.adviserinfo.sec.gov). Please read the disclosure statement carefully before you engage our firm for advisory services.

https://centurawealth.com/wp-content/uploads/2023/05/iStock-1363015018.jpg12242448Andre Lawrencehttps://centurawealth.com/wp-content/uploads/2024/07/Centura-Logo-White.pngAndre Lawrence2023-05-18 18:58:002025-06-29 22:26:10Holistic Planning for High Net Worth Individuals and Families

At Centura Wealth Advisory, we believe in creating exponential value for our clients. But what does that mean, exactly? Let’s take a look.

What Do We Mean By Exponential Value?

Exponential value, as we define it, is the concept of taking two things and creating synergies that result in something greater than the sum of its parts. In other words, 1+1=4. We believe that tax planning is one of the best ways to create exponential value for our clients.

Let’s Take a Hypothetical Example

Imagine a business owner who is selling their business and has a significant transaction coming up. If we can save them half of the tax bill they would otherwise pay on that transaction, the resulting wealth could be life-changing. Depending on the size of the transaction, this could amount to tens of millions of dollars. This newfound wealth can have significant impacts going down the road, whether that be for personal consumption, wealth transfer, legacy planning, charitable intent, philanthropy, or other purposes.

The Compounding Effect of Wealth Over Time

The compounding effect of wealth over time is what creates the true exponential value. By having more assets on your balance sheet, you have the ability to invest more money for the long-term, which coupled with compounding, creates newfound wealth. Of course, this must be done by investing in quality assets paired with a prudent approach to portfolio management, over time. For example, we have had business owners who have sold their businesses for tens of millions of dollars in their 30s. By objectively investing the wealth for a long period of time, in quality assets with strong risk adjusted returns, these business owners can generate life-changing results for their families, communities, and generations to come.

Baseline Scenario

To illustrate the point, we always do a baseline scenario, which involves paying taxes on the business sale and investing the money. We compare this to a scenario where the client employs tax planning strategies on the front end, saves more money, and then invests the money alongside the proceeds of the business sale. The results are often night and day.

How Exponential Growth Creates Value

Let’s Talk Compound Interest

Albert Einstein once famously said, “Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.” Einstein was fascinated with the concept of compounding interest and the effects it can have over time. At Centura Wealth Advisory, we couldn’t agree more.

The idea behind compounding interest is simple but powerful. By reinvesting your earnings, you can earn interest not only on your original investment but also on the interest earned. Over time, this can lead to substantial growth in your wealth. In fact, the longer you allow your money to compound, the more significant the impact can be.

We believe that anyone who is fascinated by the concept of exponential value should run the math on the time value of money and see how a bigger pot of money invested over time at high returns can really add substantial wealth. This is where tax planning comes into play.

Customized Tax Planning Strategies

At Centura Wealth Advisory, we provide customized tax planning services to our clients that are designed to minimize their tax liabilities while maximizing their financial outcomes. We work closely with our clients’ legal and accounting teams to ensure that all risks are addressed and key aspects of the tax planning process are fully integrated into their overall financial plan.

Our tax planning strategies involve a range of options all of which mitigate, eliminate and/or defer income tax. In addition, these income tax reduction strategies aim at maximizing exemptions, exclusions, deductions, and/or credits. Furthermore, we utilize tax efficient investments, trusts, and a range of asset protection strategies to help our clients safeguard their wealth.

We are committed to providing our clients with the highest level of service and support. We believe that creating exponential value for our clients is not only good for their financial outcomes but is also good for our business. We pride ourselves on building long-term relationships with our clients that are built on trust, transparency, and mutual respect.

Our Holistic Approach

At Centura Wealth Advisory, we take a holistic approach to wealth management. We understand that creating exponential value for our clients requires more than just tax planning. We work closely with our clients to understand their unique financial goals and develop customized strategies that align with their objectives. By doing so, we can help our clients create exponential value that goes beyond just financial returns.

What Does a Holistic Financial Plan Include?

A holistic approach looks at an individual’s lifestyle, goals, values, and priorities to create a financial plan that works for them. Financial planners can coordinate these needs and the lifestyle of their clients in order to create a strategy.

Insurance needs (home, auto, life, long-term care, liability, etc.)

Tax planning

Tax preparation

Final Notes